Strengths

- The best-performing precious metal for the week was platinum, though it was still down 5.86%. With platinum near 20-year highs, the lack of greenfield investment is creating a structurally supply-constrained market, which may explain its relative resilience. Analysts noted that platinum bar availability remains tight, unlike gold or silver.

- Swiss gold refiners imported 51 tons of gold from the United States in February, nearly double the previous month, while total exports fell 17% to 106 tons. Exports to the U.S. were less than half a ton, though still higher than in January, according to Swiss trade data.

- On a price-to-net asset value (P/NAV) basis, gold producers are trading at 1.5x, a 3% discount to the historical average. On 2026E EV/EBITDA, the group is trading at 6.4x, a 10% discount. Using spot commodity prices, valuations appear more discounted, with P/NAV and 2026E EV/EBITDA at 44% and 15% discounts, respectively, according to Bank of America.

Weaknesses

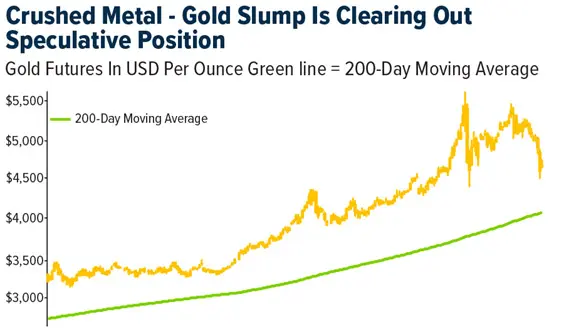

- The worst-performing precious metal for the week was silver, down 16.30 %, with both gold and palladium lower by 10%. This week’s drop in gold marks its worst weekly decline in four decades, driven by a nearly 10 basis point rise in U.S. Treasury yields across the curve. Yields rose 17 basis points for 1-, 2-, and 3-year notes, making them more attractive and pressuring commodity prices.

- Investors are pricing the broader mining sector lower due to expected margin compression from higher energy and consumable costs. Gold prices are now below pre-war levels, raising questions about its safe-haven status. A stronger U.S. dollar and fading rate cut expectations amid rising inflation pressures from higher energy prices are also contributing, according to JPMorgan Chase.

- In 2022, a similar trend followed Russian invasion of Ukraine, when surging energy prices drove inflation higher. During that period, gold declined for seven consecutive months from April to October.

Opportunities

- Despite this week’s pullback, silver demand remains strong, with China importing over 790 tons in early 2026, driven partly by solar production. Tight inventories and solid structural demand continue to support the outlook beyond short-term volatility.

- Ray Dalio believes the Iran conflict centers on control of the Strait of Hormuz; if Iran retains influence, it signals a loss for the United States. He warns that failing to keep the strait open could expose U.S. weakness—militarily and financially—potentially driving creditors away and boosting gold. Dalio also highlights U.S. debt, the dollar, and gold as key assets to watch.

- According to Canaccord Genuity, gold mining companies can support investors through aggressive share buybacks. A neutral stance is recommended, as strong free cash flow and clean balance sheets should enable companies to repurchase shares on further weakness.

Threats

- According to Canaccord Genuity, the GDX/GLD ratio has broken below its 100-day moving average, signaling weaker sentiment toward gold miners. While GDX at 94 remains above its 100-day average of 90, a decisive break below could push gold equities into bear-market territory.

- Ghana’s new gold royalty, which can reach 12% when prices exceed $4,500 per ounce, is reducing mining margins and may shift investment to other regions. At the same time, a 20% rise in Ghana’s stock index—driven by banks and oil stocks—suggests foreign capital is rotating away from mining as royalties peak.

- Gold miners are facing pressure from lower gold prices and rising diesel costs, which account for 15–20% of cash expenses. Producers set 2026 cost assumptions around $70 per barrel oil, but prices have moved higher. Open-pit mines are most exposed due to heavy diesel use, particularly in Africa and Latin America, where weaker currencies increase fuel costs. Reports also suggest Australia holds only about one month of diesel reserves, raising additional margin risk if shortages emerge.