Strengths

- Tokenization is moving from pilot projects to institutional-grade market infrastructure. Superstate’s $82.5 million capital raise, $1.2 billion already tokenized, and SEC-registered issuance model show blockchain can now support fundraising, share issuance, and settlement within existing regulations. This cuts settlement times from days to near-instant, lowers intermediary costs, and enables 24/7 capital markets—strengthening crypto’s long-term integration into global finance.

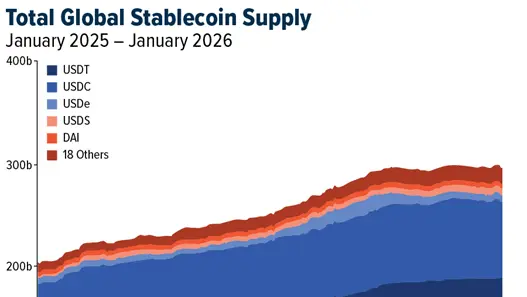

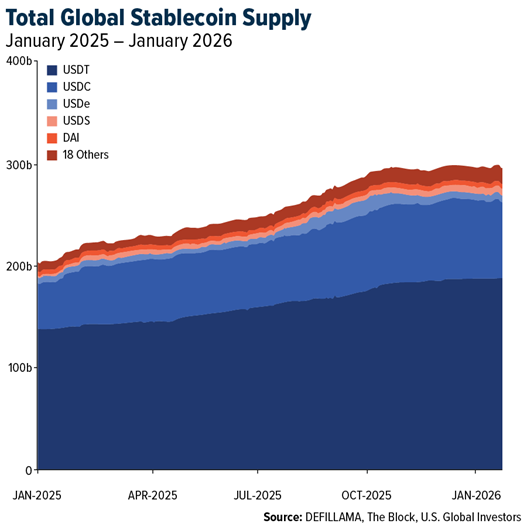

- Stablecoins have scaled beyond experimentation. Global supply exceeds $270 billion, more than double levels from two years ago, while USDC has grown approximately 80% year-over-year (YoY) for two consecutive years, according to Circle. Visa already processes around $4.5 billion in annualized stablecoin settlement, and both Visa and Mastercard are integrating stablecoins into payment rails. Circle’s CEO projects roughly 40% compound annual growth as banks move from pilots to live deployments, cementing stablecoins as a foundational layer of modern finance.

- Superstate is a regulated tokenization firm enabling SEC-registered assets, including Treasuries and equities, to be issued and settled directly on public blockchains. Its $82.5 million Series B, led by Bain Capital Crypto, brings total funding above $100 million and assets under management to $1.2 billion. The platform supports direct equity issuance and real-time settlement on Ethereum and Solana, cutting settlement from days to minutes and demonstrating scalability beyond tokenized Treasuries.

Weaknesses

- Bitcoin has fallen roughly 55% against gold since its December 2024 peak, while gold is up about 12% year-to-date (YTD) and trading near record highs. The BTC/gold ratio (18.46) is roughly 17% below its 200-week moving average, a level historically linked to prolonged underperformance. Similar breakdowns in past cycles lasted over a year, challenging Bitcoin’s role as a reliable store of value in risk-off environments.

- XRP has dropped about 19% from early-January highs, with investor sentiment in “extreme fear,” according to Santiment. Many small investors are stepping aside, and on-chain data mirrors early 2022, when prices fell for months. New buyers now hold XRP at higher prices than older holders, increasing the risk of further selling if prices don’t stabilize.

- Ethereum’s Fusaka upgrade was designed to boost data capacity and lower transaction costs by allowing more data (“blobs”) per block, mainly to support layer-2 networks. This temporarily increased transactions and active addresses but lowered fees, reducing ETH fee burn and weakening Ethereum’s revenue base. JPMorgan notes that past upgrades produced short-term activity spikes but failed to sustain growth, as value continues migrating to layer-2s like Base and Arbitrum.

Opportunities

- Sharon AI’s $500 million non-recourse on-chain loan, backed by tokenized GPU hardware, shows how blockchain can replace slow, restrictive bank financing with transparent, asset-backed credit. With $1.2 billion already deployed by USD.AI, this approach lowers capital barriers, improves collateral monitoring, and opens private credit markets to institutional investors seeking yield from AI compute.

- PwC notes that 2026 marks the shift from draft rules to live regulatory regimes across key hubs (EU MiCA, U.S., U.K. FSMA, UAE, Switzerland), accelerating institutional adoption. Stablecoins now exceed $270 billion in circulation, and regulated frameworks enabling banking access, tokenization, and cross-border products. Firms building compliant infrastructure early can capture outsized institutional flows despite higher compliance costs.

- Bermuda is emerging as a test case for on-chain public finance. Building on its 2018 Digital Asset Business Act, the country pilots stablecoin payments and tokenization with Coinbase and Circle, using USDC, which has over $30 billion in circulation globally. The initiative demonstrates live government and financial use cases, offering a scalable blueprint for modernizing payments, cutting settlement costs, and attracting digital-asset capital.

Threats

- Operational and custody risks at the sovereign level are becoming a systemic threat to crypto enforcement. South Korean prosecutors lost a “significant” amount of seized bitcoin, likely due to a mid-2025 phishing attack, exposing weak key management. Past seizure attempts of up to 24,613 BTC (~$127 million in 2024) highlight the scale of assets at risk, which could undermine trust and complicate regulation.

- Macroeconomic uncertainty is driving short-term institutional risk aversion in crypto markets. U.S. spot bitcoin ETFs saw $708.7 million in net outflows in a single day, while ether ETFs lost $286.9 million, as investors reduced exposure amid geopolitical tensions, interest rate uncertainty, and bond market volatility. Although spot crypto ETFs still hold over $116 billion, repeated macro-driven outflows could increase price swings and weigh on market confidence.

- Even with Federal Housing Finance Agency guidance, crypto adoption in U.S. mortgages remains limited. Homeownership is ~65%, and first-time buyers’ average age rose from ~39 in 2010 to ~59 in 2025. Lenders apply 30–50% haircuts to volatile assets like bitcoin, keeping most crypto-backed loans in jumbo or private-label markets. With BTC drawdowns historically exceeding 50%, timing and settlement risks keep crypto mortgages niche without clearer rules.