Strengths

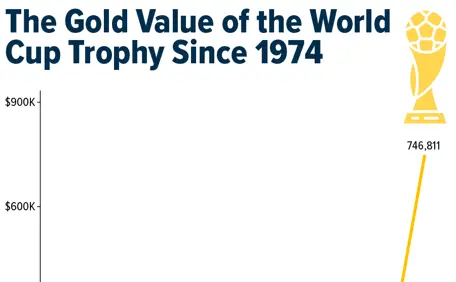

- The best performing precious metal for the week was palladium, up 2.41%. The World Cup kicks off this week, where one hard-working, intense team with a proven process will ultimately hoist the trophy. We see that journey as remarkably similar to the process miners undertake to recover gold from the ground, both require patience, discipline, and a refined approach repeated again and again before the payoff. Fittingly for such an electric event, we looked at how the price of the gold in the trophy has performed over time, a reminder to stay the course with hard work and a proven process.

- Asian-based ETFs have continued to accumulate gold even as U.S. and European holdings have rolled over, with the metal now down about 25% from its January closing high and finding some support around the $4,000 level. Chow Tai Fook shares surged as much as 13% after FY26 net income rose 52% to HK$9.0 billion and FY27 guidance beat expectations, driven by a recovery in weight-based gold jewelry demand as prices pulled back, with April and May same-store sales up 19.7% in mainland China and 40.6% in Hong Kong and Macau.

- Scotia analyzed several valuation metrics, including free cash flow yield, EV to EBITDA, price to cash flow, and price to net asset value, to assess where gold equities are trading today versus historical valuations going back to the 1970s. In short, gold equities are trading at very attractive valuations across these four metrics at spot gold prices compared with historical levels.

Weaknesses

- The worst performing precious metal for the week was platinum, down 4.45%. Platinum faced notable weakness as ETFs cut 46,948 troy ounces from their holdings in the latest session, a 1.6% daily drop that brings year-to-date selling to 15%, the steepest decline among the precious metals. The selling pressure reflects heightened volatility tied to war-related developments, with investors paring back exposure as shifting geopolitical headlines drove sharp swings across the complex.

- Resolute Mining recently reported that security concerns throughout April and May impacted the delivery of key equipment, which in turn affected mining of higher-grade zones in the A21 pit. The company also flagged that underground grades have been lower than expected due to intermittent blasting as a result of temporary explosives supply issues, and that maintenance downtime originally planned for May has been deferred into June 2026 and extended. As a result, Resolute Mining expects a negative impact on Q2 production and is now targeting the lower end of FY guidance, according to Canaccord.

- The ECB noted that following the outbreak of war in the Middle East, some central banks sold gold and U.S. Treasuries to support their economies and currencies. The Turkish central bank sold or loaned out about 130 tons of gold, one of the largest reserve drawdowns in recent years, to defend its currency, mitigate rising energy import costs, and manage economic fallout. In 2026, besides Türkiye, other known sellers include Russia, reportedly to fund its ongoing war against Ukraine.

Opportunities

- According to RBC, junior gold EV per ounce valuations have increased materially from mid-2025 levels, clearing the prior cyclical highs set in 2020. Across the 90 plus companies RBC tracks, valuations are now estimated at $80 per ounce, up from $30 per ounce as of mid-2025. When measured as a percentage of the gold price, valuations have also increased but remain near cyclical lows, indicating the sector has not fully kept pace with gold’s rise over time.

- Northern Star Resources, according to Bloomberg, has received multiple takeover offers over the past year. Elliott Management, which holds a 4% stake, is suggesting that the company should be sold.

- The Gold Miners Bullish Percent Index has at one point collapsed to around 7.7, a washout reading seen only a handful of times in the past decade, including the March 2020 crash, the late 2022 bottom, and the 2023 low, each of which marked major buying opportunities before strong rallies in the sector. Historically, readings below 10 have signaled peak capitulation in gold miners, suggesting current extreme pessimism may once again be setting the stage for a significant rebound.

Threats

- Countries with potential royalty policy changes include Panama, Chile, Papua New Guinea, and Indonesia. Sliding scale royalties are also common in South America and Africa, although some countries do not currently use this structure and may adjust policies to align with regional peers, according to Scotiabank.

- Citigroup lowered its three-month price target for gold to $4,000 per ounce from $4,300, as the impasse over the Strait of Hormuz and elevated energy prices raise expectations that the Federal Reserve will hike interest rates this year. Analysts including Kenny Hu noted that softer physical demand may further weigh on prices.

- According to Bank of America, gold faces limitations as an official reserve asset compared with major fiat currencies. Its price is volatile, it is not remunerated, and when held in physical form it is costly to store. More importantly, supply is not fully elastic and does not adjust smoothly to shifts in international demand for liquidity.