The tough year continued in October for many asset classes, including precious metals. In our universe, however, uranium and other energy transition metals have been a welcome exception to the market carnage; for example, our spot uranium oxide proprietary composite7 is up 24.12% YTD. By contrast, gold is off 10.70% YTD through October 31, 2022, and silver bullion2 has lost 17.78% YTD. Gold mining equities3 are down 21.54% YTD. The broader equities markets have also been trounced, with the S&P 500 Index7 off 18.76% YTD and the U.S. Treasury Index down 14.30%.

Month of October 2022

| Indicator | 10/31/2022 | 9/30/2022 | Change | Mo % Chg | YTD % Chg | Analysis |

| Gold Bullion1 | $1,633.56 | $1,660.61 | ($27.05) | (1.63)% | (10.70)% | Record seven straight down months |

| Silver Bullion2 | $19.16 | $19.03 | $0.14 | 0.72% | (17.78)% | Continues to diverge promisingly from gold |

| Gold Senior Equities (SOLGMCFT Index)3 | 96.79 | 97.17 | (0.38) | (0.39)% | (21.54)% | Promising divergence relative to gold |

| Gold Equities (GDX)4 | $24.16 | $24.12 | $0.04 | 0.17% | (24.57)% | (Same as above) |

| Bloomberg Comdty (BCOM Index)5 | 113.35 | 111.49 | 1.86 | 1.67% | 14.30% | Stabilizing at July levels |

| DXY US Dollar Index6 | 111.53 | 112.12 | (0.59) | (0.53)% | 16.57% | Early topping signs? |

| S&P 500 Index7 | 3,871.98 | 3,585.62 | 286.36 | 7.99% | (18.76)% | Fed pivot FOMO squeeze |

| U.S. Treasury Index | $2,142.42 | $2,172.70 | ($30.28) | (1.39)% | (14.30)% | Another down month, 17.8% drawdown |

| U.S. Treasury 10 YR Yield* | 4.05% | 3.83% | 0.22% | 22 BPS | 254 BPS | Early topping signs? |

| U.S. Treasury 10 YR Real Yield* | 1.53% | 1.67% | (0.14)% | -14 BPS | 263 BPS | Early topping signs? |

| Silver ETFs** (Total Known Holdings ETSITOTL Index Bloomberg) | 764.76 | 763.98 | 0.78 | 0.10% | (13.69)% | Selling abating |

| Gold ETFs** (Total Known Holdings ETFGTOTL Index Bloomberg) | 95.10 | 97.04 | (1.93) | (1.99)% | (2.80)% | Six consecutive down months |

Source: Bloomberg and Sprott Asset Management LP. Data as of October 31, 2022. *Mo % Chg and YTD % Chg for this Index are calculated as the difference between the month end's yield and the previous period end's yield, instead of the percentage change. BPS stands for basis points. **ETF holdings are measured by Bloomberg Indices; ETFGTOTL measures the total known holdings of gold exchange traded funds (ETFs); ETSITOTL measures the total known holdings of silver ETFs.

October Review

Spot gold fell $27.05 (1.63%) to close at $1,633.56 for October. Gold has now dropped a record seven straight months. Over the past few months, gold prices have been held back by the strengthening U.S. dollar ("USD") and rising interest rates, despite strong gold demand. Longer-term investors have taken advantage of lower prices to build positions. The World Gold Council reports that in Q3 2022 gold demand recovered to pre-COVID levels, rising 28% year-over-year and 18% year-to-date compared to 2021. Gold mining equities performed better than physical gold in October, with the undervalued gold mining sector offering an attractive risk/return profile after several months of declines. The gold mining sector has begun to report third-quarter financial results, which are mixed but indicate that cost pressures appear to be easing, with several operators noting stronger production expected for the second half of 2022. Even with the lower gold price, margins remain profitable and balance sheets are in good shape.

All Eyes on the Fed

Signs that Federal Reserve ("Fed") interest rate hikes could slow amid rising global financial stability have sparked trade reversals across some asset classes. Since March 2022, there has been an unrelenting rise in Fed rate hike expectations as the Fed desperately sought to bring rampant inflation under control with its most aggressive rate hikes in decades. The UK fiasco, though eye-catching, was not the only sign of these unsustainable rate hikes causing damage to the financial-economic system, which may eventually boomerang back to the U.S.

Gold demand was strong in Q3 2022 as long-term investors took advantage of lower prices to build positions.Throughout the month, signs of a slowing in the pace of Fed rate hikes gathered momentum. Central banks had already signaled that the high U.S. dollar ("USD") level was causing financial stability issues. Currency interventions in the UK, Japan and China this past month and signals from Fed channels that officials were exploring how to communicate slower rate hikes sparked a reversal trade. Adding to the evidence of slowing rate hikes were the lower-than-expected interest rate hikes by the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC) and less hawkish language from the ECB. Another important catalyst was the U.S. Treasury openly exploring bond purchases to improve U.S. Treasury liquidity, which has fallen to worrisome levels last seen in March 2020.

Gold Bullion Continues to Hold Below $1,700

After an initial short-covering rally from the UK shock, gold fell back to the recent low end of its trading range as shorting resumed. But with positioning overcrowded and cross-asset correlations elevated, even a tiny perceptible move to slowing interest rate hikes can quickly morph into a pause (or a precursor to a pivot). Both were catalysts for a broad rally in a crowded market with abysmal trading liquidity depth. As highlighted previously, gold positioning has ground down to the low end of its 10-year range, trading in the short positions accounting for most price swings. Often, when established trade patterns are about to change, short position holdings show increased volatility as shorts have increased convexity to potential squeezes. Gold continues to hold below the $1,700 level (Figure 1) but shows signs of the downtrend's deceleration as measured by the 200-day Z-score.8

Figure 1. Gold Bullion with 200-Day Z-Score (2018-2022)

Source: Bloomberg. Data as of 10/31/2022. Included for illustrative purposes only. Past performance is no guarantee of future results.

The UK Situation: A Cautionary Tale

The current extreme regime change is unfolding with high volatility and challenging asset returns. The last market regime change event was the 2008 global financial crisis ("GFC") when dovish central banks ushered in markets built and priced on low macro volatility, "slow-flation," stable correlations, forward guidance and the use of leverage. Central banks (via trillions of dollars in quantitative easing [QE], zero interest rate policy [ZIRP] and negative interest rate policy [NIRP]) pushed investors out on the risk curve and down the quality ladder in a quest for yield. Since the GFC, modern market structures have been built on this regime set of conditions now unraveling at a breakneck pace due to the fastest interest rate hikes in decades.

Markets contain many hidden risks. The UK pension investment in LDIs (Liability-Driven Investing)9 is an example. LDIs use derivatives to gain leverage to significant exposures (out on the risk curve, down the quality ladder, with leverage). When UK rate volatility blew out, margin calls were triggered. A liquidity event ensued, forcing the Bank of England to launch "temporary QE," suspend QT and exact a fiscal policy U-turn. The real risk is another UK pension plan-type disaster that is not averted at the last minute, leading to cascading VaR events (forced selling; value at risk, or VaR, is a way to quantify the risk of potential losses for a firm or an investment.). As central banks hike at the fastest pace in decades, more landmines will likely pop up. These are under-the-radar features of a leveraged financial system when liquidity is rapidly removed. In moments of fragility, they can detonate, setting off chain reactions crippling economies almost overnight.

Deficits matter again; the events in the UK signify that the free (QE) lunch era is near its end. After the GFC, developed countries could enact a fiscal stimulus, cut taxes and replace lost income without concern about inflation or rising interest rates. Those years of financial repression allowed policymakers to avoid the economic consequences of market forces. The UK event is not idiosyncratic; it is a symptom of overleveraged markets requiring constant liquidity. However, due to persistently high inflation rates, QE is no longer tenable without consequences. The bill has seemingly come due; policymakers and governments are on notice, even in the U.S.

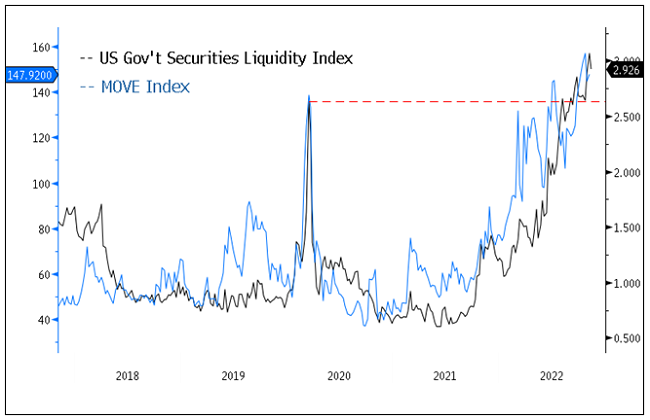

U.S. Treasury Liquidity: One Shock Away?

Though the near-term rally in risk assets may signal a more bullish tone, U.S. Treasury liquidity (see Figure 2) now matches or exceeds March 2020 levels, when the last shock event caused markets to seize up. The U.S. Treasury market is the world's deepest liquid market, and if it were to seize up, the spillover effects globally would likely be severe and immediate. If a shock were to happen, there would likely be forced sales to cover margin calls leading to lower prices and further margin calls. Eventually, liquid assets may all be sold, leaving illiquid assets that cannot be liquidated for capital requirements. In extreme macro volatility and uncertainty, illiquid assets would approach a zero value and a full-blown credit and credit liquidity crisis may ensue.

The MOVE Index10 (bond volatility measure) has also surpassed its March 2020 levels (Figure 2). The creator of the MOVE Index notes that at a 150 reading, the Fed has lost control of bond volatility. At 150, the daily implied price swing is 9.5 basis points per day, an untenable level of volatility for the risk-free asset used in virtually every financial asset pricing model. Conversely, a 50 reading indicates that the Fed is containing risk and is a signal to take on risk with a Fed backstop. There will likely be a massive risk event if the Fed loses control of the long end in a leveraged world still trapped in long-duration assets. Similar to the UK, if U.S. Treasuries lose liquidity functioning, we can expect some form of "temporary QE" as market functioning will likely trump the inflation fight. The U.S. Treasury Department is also exploring buying bonds to improve functioning, as it recognizes that the U.S. debt market underpins the entire global financial system.

Figure 2. U.S. Government Securities Liquidity Index and MOVE Index Both Surpass COVID Levels (2018-2022)

Source: Bloomberg. Data as of 10/31/2022. Included for illustrative purposes only. Past performance is no guarantee of future results.

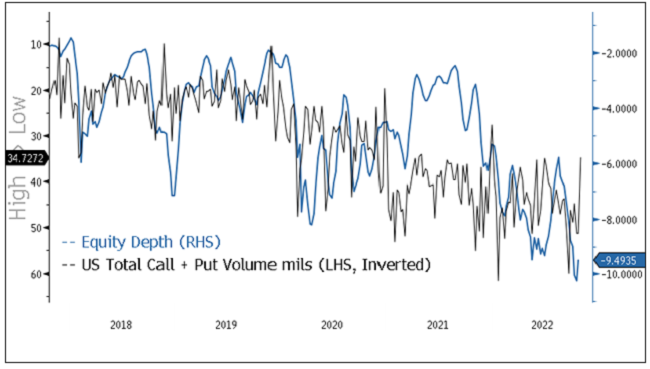

Falling Equity Liquidity and Options Activity

The recent wild intraday swings are signs of the market malfunctioning due to illiquidity. Lately, about 50% of all options traded now are 24 hours or less to expiry, and this is institutional activity, not retail, individual investor activity. In short, institutions have become day traders. Compounding this extreme options trading activity, market depth is now worse than March 2020 levels and dealers are short gamma. Short gamma forces dealers to sell into the down leg and to buy the up leg (to maintain their delta hedge).11 This weaponization of gamma results in chasing end-of-day flows resulting in extreme price moves that will likely generate noise but provide little information. Each day becomes its own ecosystem of flow chasing. Figure 3 highlights the deterioration in equity market depth and the increase in options volume, which has more than doubled since 2019.

Mechanically, if equities fall sharply, puts are monetized and calls are bought, creating a massive positive swing in deltas (buying flow).12 These flows then spill over into systematic funds, resulting in more buying. As equities rally, this process reverses (calls sold, puts bought, negative delta), creating a near impossible market. As fascinating as market microstructures have become, the level of market fragility and risk under the surface of manic flows is unsettling. If a liquidity event were to occur driven by U.S. Treasuries seizing up, imagine how these 24-hour options would trade.

Figure 3. Equity Market Depth and U.S. Total Call+Put Volumes (2018-2022)

Source: Bloomberg. Data as of 10/31/2022. Included for illustrative purposes only. Past performance is no guarantee of future results.

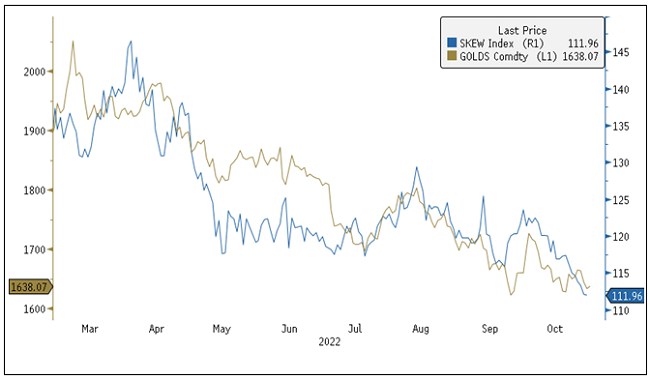

Recession/Financial Stability Fears Replace Rate/Inflation Fears

Last month saw a pause in the rise in the USD and yields as central banks' tone and messaging softened. Along with financial stress rising and concerns of overtightening, various recession probability indicators are now signaling recession. When the market shifts its focus from the rates/inflation shock to the recession/financial stability fears, we expect this will likely be more favorable for gold bullion. Equity volatility has lagged other volatility measures (rates, currencies, credit, etc.) mainly due to the relatively hedged markets resulting in low net equity exposures. The CBOE SKEW Index (a measure of perceived tail risk derived from options pricing)13 is a good "visual" for this lack of reach for safe haven assets. The well-hedged positions deter funds from paying up for option protection. In Figure 4, we overlay a chart of the SKEW Index with gold bullion to highlight the recent lack of a safe haven (or tail risk) bid for gold. Without this protection bid, gold has closely (inversely) tracked the rise in bond yields and the USD.

The story of the markets through most of the year has been the rate and inflation shocks. Only recently has the market begun to price in the medium- and long-term consequences (recession and related financial instability) of the extraordinary rate hikes by the central banks. Since mid-October, there has been an emerging "Fed pivot FOMO" as signs of peak tightening will likely lead to peak yields and a peak USD, a bullish market catalyst. With low net exposure, funds need to buy expensive calls (right-tail crash-up hedges) or reduce hedge positions to increase exposure. A reduction of hedges will likely increase funds' exposure to left-tail events. In an upside-down world, a short-term squeeze into risk assets, even as we transition into the recession/financial instability risk phase, is a likely required step for gold to regain its safe haven footing. If peak yields and a peak USD are realized in the short term, peak gold short positions are also likely.

Figure 4. CBOE SKEW Index and Gold Bullion (2022)

Source: Bloomberg. Data as of 10/31/2022. Included for illustrative purposes only. Past performance is no guarantee of future results.

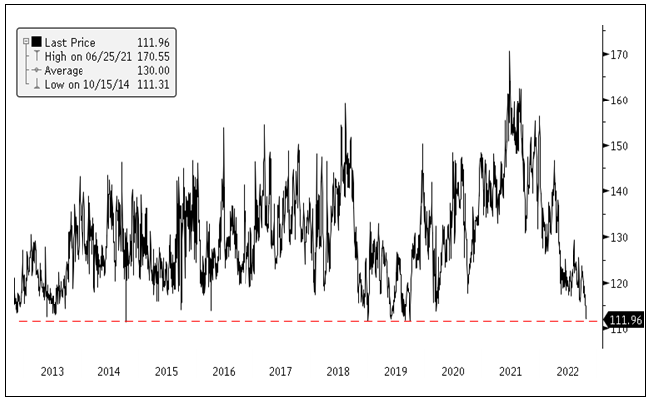

The 10-year percentile reading of the SKEW Index has now reached the 0.2%-tile. There will likely be a reach for protection when financial instability increases. Risk and volatility patterns around financial system stability are far different from other risks, as credit and credit liquidity typically comes into play. They have a long and dramatic history of producing massive market drawdowns.

Figure 5. CBOE SKEW Index at <1%-Tile, Last 10 Years (2013-2022)

Source: Bloomberg. Data as of 10/31/2022. Included for illustrative purposes only. Past performance is no guarantee of future results.

The Risk Window is Opening

The most hawkish central bank tightening in decades has shown that leveraged markets and governments depend on dovish liquidity conditions, and withdrawal is excruciating. Every major tightening cycle exposes hidden risks (landmines or left-tail risks) that typically show up during times of stress, such as now. When QE fades, liquidity quickly falls away and markets lose their ability to transfer risk. As financial stress builds, QT (quantitative tightening) becomes impossible to execute without repercussions. With financial system stress cracks showing up, central banks are now trying to balance aggressively fighting the highest inflation levels in 40 years while maintaining financial stability in over-leveraged governments and markets. A significant risk remains, such as a liquidity event and, ultimately, a test and failure of a central bank put somewhere.