(Kitco News) - Gold’s sharp correction this year may be unsettling for investors, but one market strategist argues the precious metal remains firmly within a historic bull market that is tracking one of its most historic rallies almost “tick for tick.”

In an interview with Kitco News, Jeff Clark, publisher of The Gold Advisor, said gold’s current decline closely resembles the correction seen during the legendary 1970s bull market, which ultimately culminated in one of the strongest advances in the metal’s history.

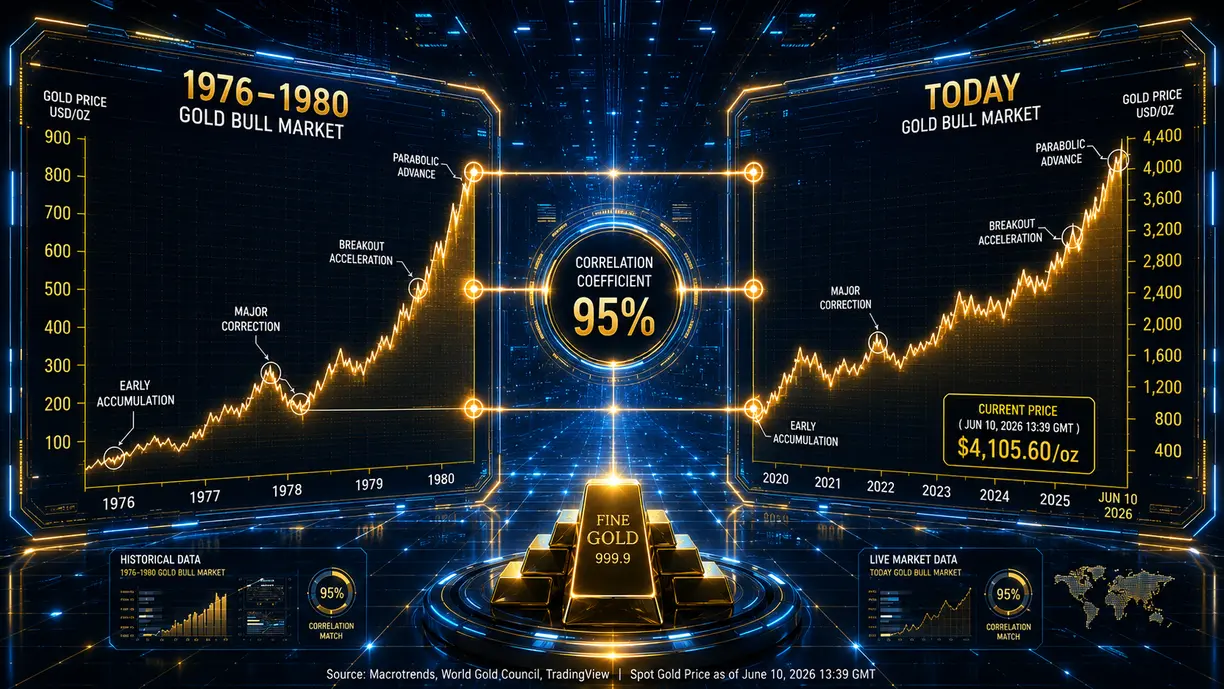

“I charted the correlation between our current gold bull market and the one from 1976 to the peak in 1980,” Clark said. “Believe it or not, the correlation coefficient between those two bull markets is 95%.”

Clark said the comparison suggests the current correction may be a normal and healthy part of a much larger advance.

“At this particular period in the 1970s bull market, gold crashed,” he said. “It crashed, and then it immediately rebounded. And guess what’s happening now? Gold is crashing. We’re matching it. It’s almost tick for tick.”

Clark noted that if the correlation continues to hold, gold would have to nearly triple from current levels to match the full magnitude of the 1970s rally.

Clark’s bullish long-term outlook comes as the precious metal faces challenging headwinds. After a historic rally to a record high of $5,600 an ounce in January, gold prices have turned negative on the year. The months-long selloff picked up momentum Friday after prices dropped below critical long-term support at its 200-day moving average.

Gold prices have now dropped nearly 8% in less than a week. Spot gold last traded at $4,125.50, down more than 3% on the day, and prices are down 4.5% year-to-date.

The veteran precious metals analyst noted that while gold prices are down more than 21% from January’s peak, the decline remains smaller than the 30% correction during the 2008 financial crisis and the 28% drop during the 2020 pandemic shock.

However, for Clark, the current weakness does not signal the end of the secular uptrend. He explained that history is still on the side of the bulls.

“If the bull market were to end right now, it would be the shortest bull market in modern history,” he said. “All other bull markets, all other bull runs in gold have been longer than what we have had right now. It’d be the shortest on record.”

Clark said that, based on historical averages, the current cycle should have at least two more years to run. As a result, he views the correction as a buying opportunity and said he has been aggressively adding to positions.

“I am personally aggressively buying right now. In fact, I just recently made a large investment,” he said.

Gold has struggled in recent months as the ongoing war in Iran has significantly disrupted the global energy market, sending oil prices sharply higher. Higher energy prices are stoking inflation fears, and markets are now looking for the Federal Reserve to raise interest rates rather than cut them.

Core inflation, which strips out volatile food and energy prices, rose 0.2% last month, compared to the 0.4% increase in April. Core inflation was slightly cooler than expected, as economists were looking for a 0.3% increase. Annual core inflation rose 2.9%, up from 2.8% reported in April.

Despite the persistent risks in the gold market, Clark said that investors are focusing too heavily on inflation risks while overlooking the damage higher interest rates could inflict on an already fragile economy.

He said that if inflation accelerates significantly, the Fed's response will eventually be to support economic growth rather than continue tightening policy.

“If inflation really gets as bad as many mainstream analysts believe, what is the Fed’s number one tool to combat a bad economy? It’s manipulating interest rates,” he said. “If the economy gets as bad as many mainstream analysts predict, it’s more likely the Fed will lower rates than raise rates, in my opinion.”

Clark also questioned how aggressively the Fed can tighten monetary policy given the federal government’s growing interest expenses.

“Can the Fed really afford to raise rates all that much?” he asked. “With the interest levels where they are, they’re making things more difficult on themselves financially by raising rates.”

Although markets have focused heavily on inflation and interest rate expectations, Clark said he sees those issues as short-term headwinds. He remains focused on longer-term structural drivers that continue to support gold, including rising debt burdens, persistent deficits, potential monetary easing and unforeseen geopolitical or financial shocks.

Among those drivers, sovereign debt remains one of his biggest concerns.

“I’m forced to remain long gold because of the financial system and because every single currency is fiat in the world today, the first time in history,” Clark said. “Because of these factors, I am forced to remain long gold. I have to continue to own my gold.”

Clark said mounting government debt levels around the world leave investors with little choice but to maintain exposure to hard assets. While the timing of gold’s next rally remains uncertain, he said the fundamental case for the metal remains intact.