2023.04.16

Gold prices are on the brink of setting another record as a confluence of market forces has prompted investors to pile into the precious metal over recent months.

Historically, gold has been viewed as a hedge against inflation, and given the high-price environment now, a rally would make perfect sense. But is that really it? Are the price movements of gold and consumer goods really in sync?

For over a year, the Federal Reserve has tried to smother sky-high inflation through monetary tightening. That, to some degree, has worked. The latest data shows US CPI was only 0.1% higher in March, which was better than anticipated and much healthier compared to the 5% a year ago.

From this, we can see that US inflation is showing signs of cooling down, and yet, gold is still gaining a lot of traction. This would defy the common perception of gold being an inflation hedge. In fact, the relationship between inflation and the yellow-colored metal hasn't been as straightforward as we may think.

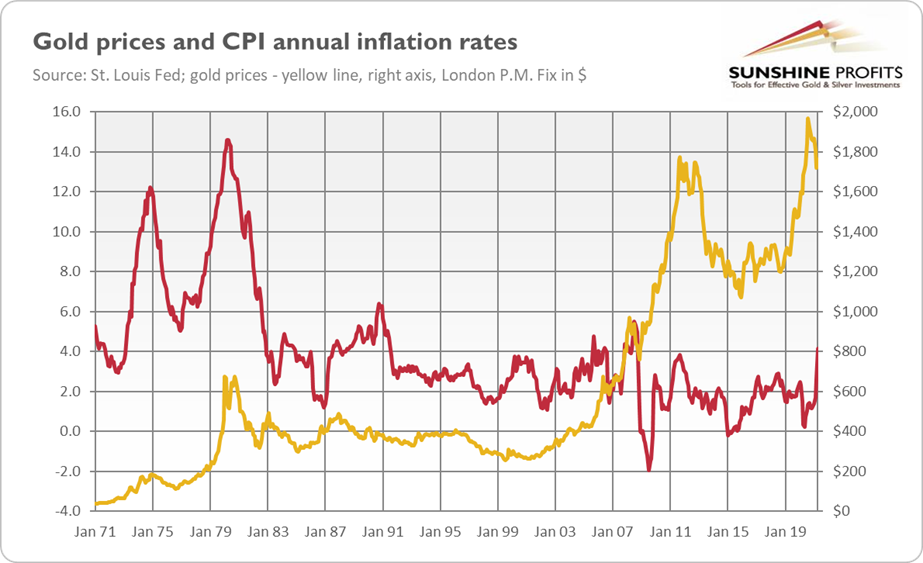

Gold vs. Inflation

Contrary to popular belief, it may be a stretch to call gold the "perfect inflation hedge."

Analysis of historic data suggests that the correlation coefficient between CPI and the price of gold is actually very close to zero over the long run. It is only during certain periods (i.e. the 1970s stagflation) when the two values had a positive correlation, but overall, there is no discerning pattern to establish a long-term link (see below).

Source: Sunshine Profits

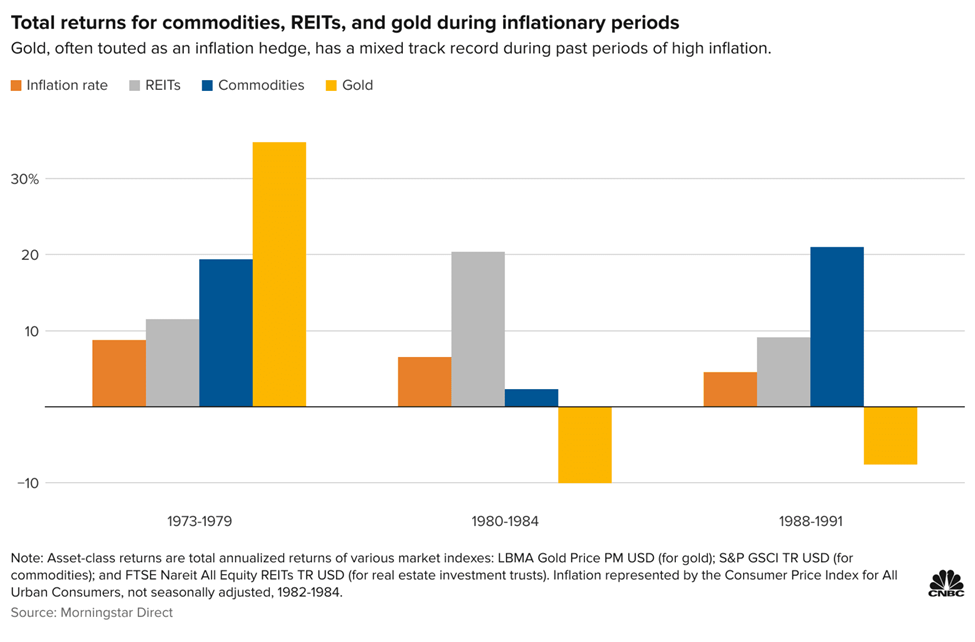

According to Amy Arnott, a portfolio strategist at Morningstar, gold's correlation to inflation has been relatively low — 0.16 — over the past half century. "Gold is really not a perfect hedge," said Arnott, who analyzed the returns of various asset classes during periods of above-average inflation.

"If you look at the very long term, gold should hold its value against inflation. But in any shorter period, it may or may not be a good hedge," Arnott concluded.

Source: Morningstar

Therefore, gold's role as an effective hedge against inflation is more of an oversimplification manifested into common knowledge over the years.

So if it's really not price levels, then what else can gold's value be tied to? One economic indicator that may better explain gold's behavior during inflationary periods — and also tied to inflation itself — is real interest rates.

Gold vs Real Interest Rates

As we know, interest rates have been consistently going up since the first quarter of 2022. By the end of March 2023, the US Federal Reserve had already announced its ninth straight rate hike, taking the base rate to the highest it's been since 2007.

The Fed's monetary tightening entails making interest rates as high as possible by raising the discount rate (what it charges to banks) and the federal funds rate (what commercial banks charge each other).

Macroeconomic theory states that a higher rate would discourage consumer spending and borrowing, which in turn slows down economic activity and helps keep inflation in check.

Under this scenario, fixed-income investments become very attractive to the general public instead, as higher interest rates mean higher returns for their money. By the same token, gold loses a lot of appeal since it pays no interest or dividend.

So, the consensus amongst market analysts and investors for years is that gold is negatively correlated with real interest rates (interest rates adjusted for inflation). According to Swiss investment bank UBS, a rise in the real rate, all else equal, "raises the cost of holding gold, and investors have tended to offload their positions."

A study published in the Financial Analyst Journalfound that the historical correlation between real interest rates and the price of gold is -0.82, which pretty much describes an inverse relationship.

To fully digest the interplay between gold and real rates, we have to first refer to a century-old economic observation called the Gibson's Paradox, which posits that a positive correlation exists between price levels and interest rates. The reason it was called a "paradox" was because the relationship could not be explained by existing economic theories.

The Gibson's Paradox remains unsolved to this day, mostly because the market conditions forming the basis of this observation occurred during the Gold Standard era. Under a gold standard, the general price level is the reciprocal of the real price of gold. Because gold is a durable asset, its relative price is systematically affected by fluctuations in the real productivity of capital, which also determine real interest rates.

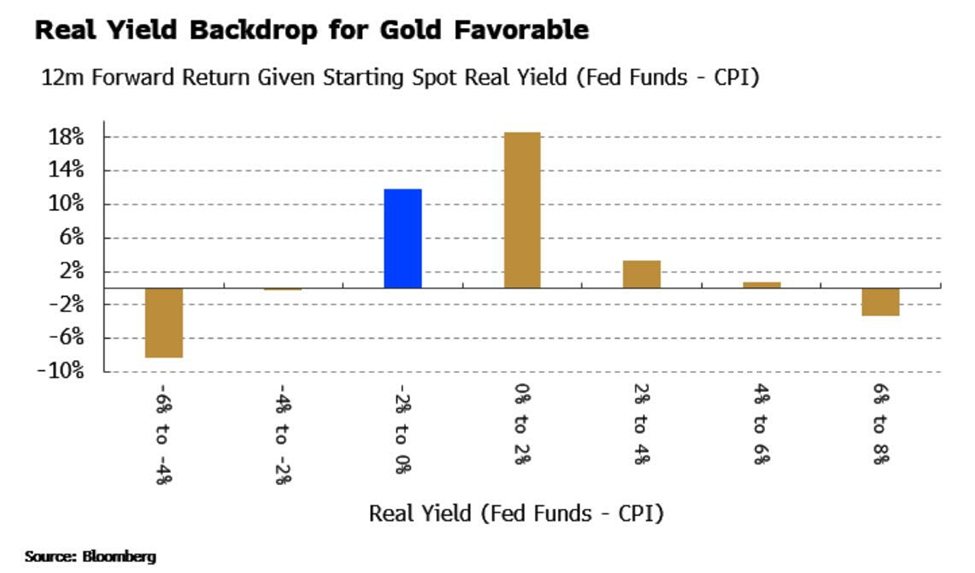

Henceforth, the Gibson's Rule was established for gold investors, which, according to Bloomberg Markets strategist Simon White, states that for every percentage point the real fed funds rate was below 2%, gold should rally 8% through the year.

Source: Bloomberg

On this basis, the outlook for gold should be positive. Take the US for example, at a real interest rate of -1% now, gold should be up by as much as 24%; so far in 2023, it has recorded a gain of 10%.

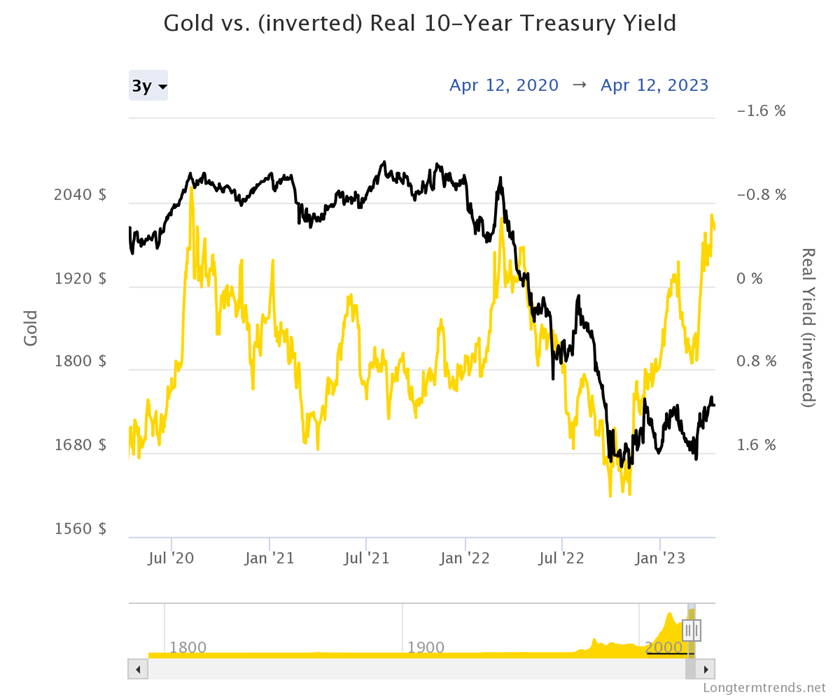

Short-Term Deviations

And yet, the Gibson's Rule does not fully explain why gold's value has remained strong under this high-rate environment. In fact, funds backed by gold have swung back into net inflows for the first time in 10 months, despite the allure of higher-yield investments on the market.

Once again, this feels rather counterintuitive and defies the general investment rationale and historic evidence (see chart below).

Source: Longtermtrends

According to those at UBS, while previous analysis has shown that the level of real rate is important, even more so is the trend and pace of the adjustment. The bank believes that investors have recently attached a greater emphasis to hedging geopolitical risks (i.e. Russia-Ukraine), inflation concerns and broader market uncertainties, instead of focusing just on the yields on assets.

Ben Popatlal, multi-asset strategist at Schroders, acknowledged that it's possible for the price of gold to go up together with real yields, contradicting the conclusion from the firm's September 2022 study which described gold as being in the middle of a "tug of war" between interest rates and inflation.

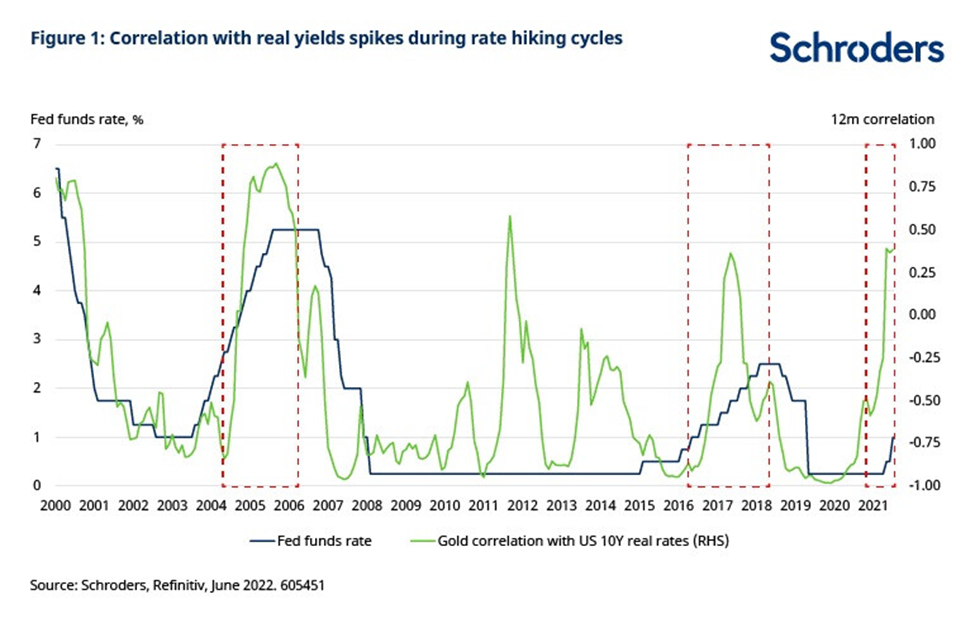

"Looking at this recent period as well as historical data in the chart below, we can see that during rate hiking cycles the correlation between gold and real yields tends to rise from negative to positive," he said.

Source: Schroders

Explaining this unusual positive relationship, the Schroders strategist pointed to a previous analysis on the effect of rate hikes on risk assets such as equities, which found that:

In general, risk assets, when driven by plentiful liquidity as opposed to by strong growth, are likely to have a negative relationship with real yields. And when/if the liquidity is withdrawn one day, such as when central banks start hiking rates and real yields rise again, gold would not be a particularly good hedge against an equity market sell-off.

"Well, now that withdrawal of liquidity has begun, and equities have accordingly made losses this year. Given our broad-based tug-of-war assertion, we might have expected gold to sell off more than it has done this year so far. But our analysis explains why gold's performance has been relatively uninteresting, neither benefiting from flows of money seeking an inflation hedge, nor losing out from the impact of rising rates," he noted.

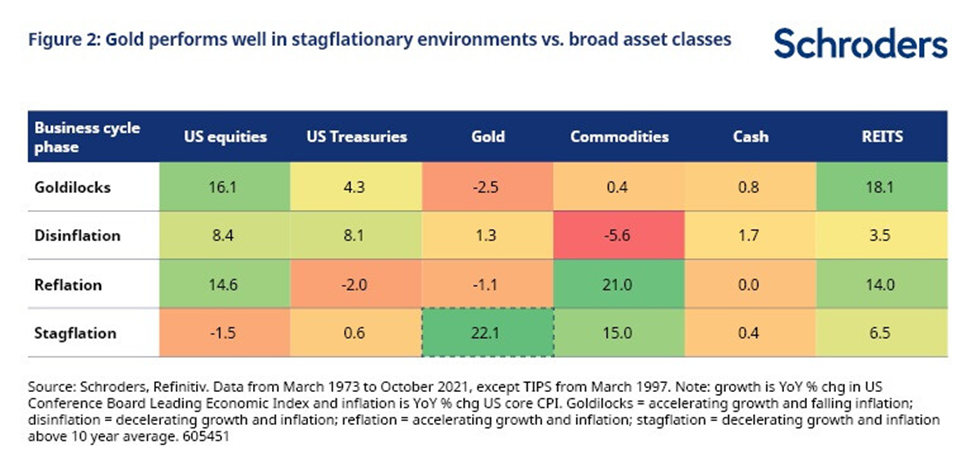

Looking ahead, Popatlal says markets are increasingly focusing on the prospect of stagnant growth and higher inflation – also known as stagflation. In such an environment, risk assets tend to underperform, and so gold should be relatively appealing to investors. "Most asset classes make losses, so investors seek the best of a bad bunch," he explained.

Source: Schroders

As seen in the chart above, gold does indeed stand up quite well in this context. While there haven't been many stagflationary periods from historical data, there have been plenty of economic slowdowns during which gold had positive correlation with real yields.

"It is encouraging that gold is again unencumbered by central banks' actions. With rate hiking cycles often leading to recession, gold starts to perform by anticipating the upcoming rate cuts and looser financial conditions the recessionary environment necessitates," Popatlal concluded.

Conclusion

As much as we like to ascribe certain rules to gold's ups and downs, the fact of the matter is that there are a lot of dynamics at play to make generalizations; everything comes down to context.

Nevertheless, what gold's performance this year is telling us is that the precious metal stands to benefit both ways in the middle of the "tug of war" between inflation and real rates. On one hand, it would serve as a hedge against rising price levels; on the other, rising rates would take the economy closer to a recession, supporting gold's appeal as safe haven.