It was likely that S&P 500 wasn‘t to sustain premarket gains following the opening bell, allowing for locking in open gains in our intraday channel. Bond auctions during the day didn‘t end up too badly, yet it was the yen‘s continued decline spurring BoJ Adachi‘s remarks about being open to hike earlier rather than having to wait to hike more when the Japan inflation horse would have left the stables already via depreciating currency.

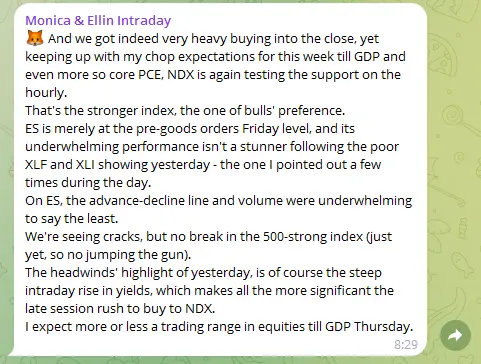

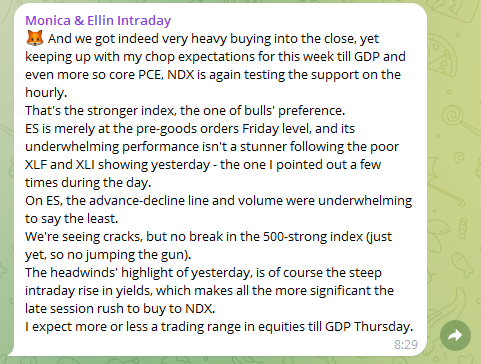

This verbal intervention was enough the change the market dynamic, especially in the Asian and European sessions today – the US closing bell action was great, seeing heavy buying focused on Nasdaq. But, the market breadth has a bit deteriorated as the below summary from our channel says – forget not how sharply 10y yield rose on a daily basis (to 4.56%) with 2y touching 5%. The odds of no Fed funds rate change in Sep went up to 54% almost, which is a very meaningful increase on a daily basis.

Hence, Russell 2000 has been and is to feel most pressure (of course, that‘s why I hadn‘t been talking bullishly IWM or even ES lately beyond an opportune dip) – Nasdaq still outperforms S&P 500, which is a good sign, and it‘s not a matter of NVDA only, but as well of ARM and MU with DELL to name a few – see also stock picks from Sunday‘s extensive analysis that had done great

(…) the right sectors are leading (tech, tben all eyes on financials recovering from two Dimon cold water pronouncements (yeah, Friday too), and consumer discretionaries as such (it‘s not about AMZN just – see LULU, ANF, AEO, ELF, RL and even TGT having trouble declining).

The sectoral mix was right in that financial and industrials rose as well while defensives didn‘t crater – and once again, the lower volume or inside bar Friday isn‘t an issue - I‘m counting on tech, and of course NVDA and beyond to lead.

The fly in the ointment were XLF and XLI yesterday, and S&P 500 hasn‘t yet found solid footing. Yields must decisively turn lower for that.

Keep enjoying the lively Twitter feed via keeping my tab open at all times (notifications on aren't enough) – combine with subscribing to my Youtube channel, and of course Telegram that always delivers my extra calls (head off to Twitter to talk to me there), but getting the key daily analytics right into your mailbox is the bedrock.

So, make sure you‘re signed up for the free newsletter and make use of both Twitter and Telegram - benefit and find out why I'm the most blocked market analyst and trader on Twitter.

Let‘s move right into the charts (all courtesy of www.stockcharts.com) – today‘s full scale article contains 3 more of them, with commentaries.

Tired of seeing those red boxes instead of way more valuable information? Try the premium services based on what and how you trade.

Crude Oil

Oil surprised nicely Friday, and continued doing so Tuesday. Oil stocks also bucked the trend of declining equities (worsening breadth), which in itself is marking risk-off. Day or two of consolidation of latest sharp gains is likely before the market picks a direction – it all depends upon whether BoJ effect on yields wears off within two days, whether the yen carry trade seems some more unwinding or not. USDJPY is thus far clear about that.

Thank you for having read today‘s free analysis, which is a small part of my site‘s daily premium Monica's Trading Signals covering all the markets you're used to (stocks, bonds, gold, silver, miners, oil, copper, cryptos), and of the daily premium Monica's Stock Signals presenting stocks and bonds only. Both publications feature real-time trade calls and intraday updates. Forget not the lively intraday Telegram channels for indices, stocks, gold and oil - here is how you can join any advantageous combination of these.

Go beyond the free Monica‘s Insider Club serving instant publishing notifications and other content useful for making your own trade moves.

Turn notifications on, and have my Twitter profile (tweets only) opened in a fresh tab so as not to miss a thing – such as extra intraday opportunities. Thanks for all your support that makes this great ride possible!

Thank you,