Strengths

On July 18, 2025, the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act was signed into law. This landmark legislation established the first comprehensive federal framework for payment stablecoins, removing them from SEC/CFTC jurisdiction and classifying them as banking products, providing the regulatory green light institutional investors had long awaited.

As of December 2025, the Markets in Crypto-Assets (MiCA) regulation completed its first year of full application. Over 100 licensed entities now use "passporting" to operate seamlessly across all 27 EU member states, making Europe the most structurally stable market for crypto-asset service providers (CASPs).

By late 2025, Spot Bitcoin and Ethereum ETFs from BlackRock and Fidelity became core institutional portfolio assets, securing $31 billion in annual net inflows. This was accelerated by an August 2025 Executive Order opening the $9 trillion US 401(k) market to crypto ETFs, transitioning the sector from retail speculation to long-term institutional savings.

Weaknesses

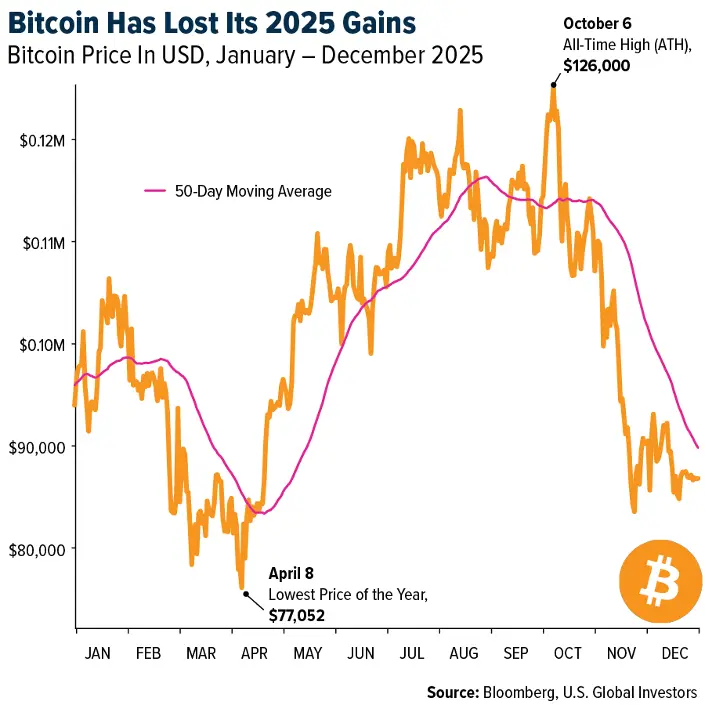

Despite growing institutional adoption, Bitcoin ended 2025 with a year-to-date (YTD) return of roughly -6%, wiping out all annual gains by December. After hitting an all-time high of $126,000 in October, it plunged about 30% to the $87,000 range. This extreme volatility, driven by leverage liquidations and shifting macro sentiment, continues to hinder Bitcoin’s evolution from a speculative asset to a stable medium of exchange.

A large portion of the market's liquidity is concentrated in just two entities: Tether and Circle. With Tether’s reserves heavily tied to U.S. debt, the entire crypto ecosystem remains vulnerable to shocks in the Treasury market or shifts in U.S. fiscal policy.

While Layer 2 solutions have improved, the user experience for non-custodial wallets and cross-chain bridges remains a barrier. CoinTelegraph reports that “gas wars” and bridge hacks, though less frequent than in 2024, continue to pose significant challenges for mainstream retail adoption.

Opportunities

In a strategic pivot to diversify away from pure fiat, Tether became the largest private buyer of gold in Q3 2025, acquiring 26 metric tons. Their total holdings now reach 116 tons (valued at $14 billion), placing them among the top 30 gold holders worldwide. This strengthens the appeal of "Tether Gold" (XAUt) as a hedge against dollar inflation.

Following the federal lead, several U.S. states in 2025, including Texas and Pennsylvania, moved to establish Strategic Bitcoin Reserves. Texas became the first to fund its reserve with a $5 million "placeholder" purchase, marking a new front for sovereign-level demand.

The GENIUS Act has enabled the mass tokenization of private credit, real estate, and commodities. Major banks are now using the framework to move trillions in traditional assets onto public and private blockchains, creating a significant new revenue stream for the sector.

Threats

The implementation of the DAC8 Directive in late 2025 marks the end of crypto anonymity in Europe. It mandates automatic tax reporting for all crypto transactions, significantly raising compliance costs for platforms and pushing some capital to offshore jurisdictions.

While the GENIUS Act resolved the stablecoin issue, other areas such as Decentralized Finance (DeFi) and privacy-focused coins like Monero face increased scrutiny. The IRS and international task forces have introduced stricter Know Your Customer (KYC) requirements for DeFi protocols, which could hinder decentralized innovation.

There is a growing risk of capital flight, as institutional funds previously allocated to crypto are redirected toward the energy and hardware demands of AI infrastructure, potentially reducing liquidity in digital assets.