Strengths

- The tokenization of Brazilian credit card receivables through BlackOpal’s GemStone platform highlights the growing maturity of real-world asset tokenization. By combining true-sale legal structures, central bank registry integration, and traditional payment rails, the initiative delivers institutional-grade, U.S. dollar–denominated yield (approximately 13%) while improving liquidity for merchants. This underscores crypto’s expanding role as financial infrastructure, particularly in emerging markets.

- Ether strengthened crypto’s institutional credibility by expanding beyond stablecoins into tokenized gold. With XAUT backed by more than 1,300 gold bars and a market capitalization of approximately $2.3 billion, the launch of Scudo (1/1,000-ounce units) improves the divisibility and on-chain settlement of gold. This reinforces crypto’s role as infrastructure for hard assets alongside Bitcoin, especially amid record central bank gold accumulation.

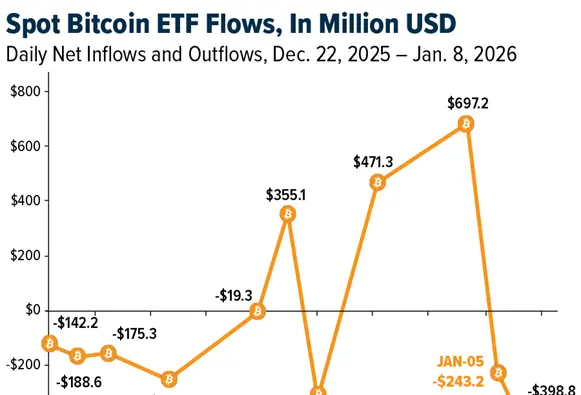

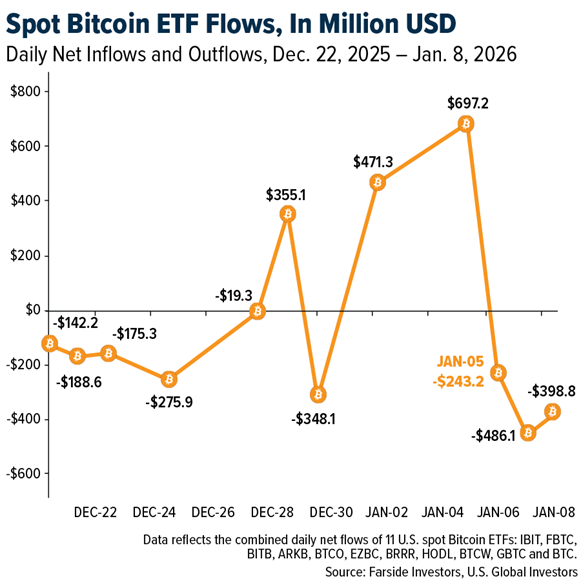

- U.S. spot Bitcoin ETFs reaffirmed their role as the primary institutional access point to crypto, attracting $697 million in inflows on the second trading day of 2026 and more than $1.1 billion in total inflows across the first two days of the year, according to Farside Investors. Despite significant outflows in late 2025, ETF assets remain above $110 billion, highlighting durable institutional participation and positioning ETFs as a structural, long-term allocation channel rather than short-term speculative capital.

Weaknesses

- Bitcoin’s failure to break above $95,000 and its repeated tests of the $89,200 support highlight weakening momentum amid ETF outflows and lighter trading volumes. At the same time, derivatives positioning shows rising leverage, with open interest nearing 700,000 BTC and persistently positive funding rates. This crowded long positioning increases downside risk, as even modest price declines could trigger forced liquidations and amplify volatility.

- The latest pullback highlighted crypto’s continued sensitivity to macro risk sentiment, with speculative segments leading losses. Memecoins and DeFi underperformed sharply, the CoinDesk Memecoin Index fell 8.6% in 24 hours, while DeFi and metaverse indexes dropped over 5%, as ETF outflows of $729 million reversed more than half of the prior week’s inflows. The episode underscores how quickly tourist capital exits during periods of uncertainty, reinforcing downside reflexivity across the market.

- The mass resignation of the Electric Coin Company team exposed governance and incentive misalignment within one of crypto’s most established privacy protocols. Internal disputes over nonprofit versus for profit structures triggered ecosystem fragmentation, a sharp ZEC sell off, and renewed questions around execution risk. The episode highlights how organizational instability, rather than technology, can undermine investor confidence and long-term adoption.

Opportunities

- Optimism’s proposal to allocate 50% of Superchain revenue to OP token buybacks marks a shift toward clearer value accrual models in crypto. By linking token economics directly to sequencer fee revenue from major ecosystems such as Base, Uniswap, and Sony-backed chains, the initiative reflects a broader industry move toward sustainable, revenue-backed token frameworks. If adopted, this model could strengthen long-term holder alignment and set a precedent for Layer 2 token design.

- The launch of regulated crypto ETFs that incorporate staking highlights a growing opportunity to position digital assets as yield-bearing instruments. Morgan Stanley’s proposed Ethereum ETF would allow investors to earn staking rewards currently estimated at 3% to 4% annually on Ether, in addition to price exposure. This comes as U.S. spot Ether ETFs have retained more than 80% of their peak inflows despite the 2025 crypto market drawdown, signaling sticky institutional demand. With global crypto ETF assets exceeding $125 billion in 2025, the integration of yield mechanisms could materially expand addressable capital and accelerate adoption of crypto within income-oriented and multi-asset portfolios.

- The launch of regulated stablecoin and RWA tokenization indexes by MarketVector, alongside NYSE-listed ETFs, underscores the growing institutionalization of crypto infrastructure. These products allow traditional investors to gain compliant exposure to stablecoin and tokenization technologies without holding digital assets directly, reinforcing crypto’s integration into mainstream financial markets.

Threats

- The potential delay of U.S. crypto market structure legislation until 2027 extends regulatory uncertainty for exchanges, issuers, and investors. Election-driven politics and conflict-of-interest debates increase the risk of legislative paralysis. The lack of near-term clarity may slow institutional investment and strategic decision-making in the U.S. crypto market.

- U.S. crypto regulation has reached a do-or-die moment as Senate negotiations stall over stablecoin yield rules and unresolved concerns around presidential conflicts of interest. Without strong bipartisan support, the market structure bill risks failing outright, potentially delaying regulatory clarity until after the 2026 midterms. Prolonged uncertainty would preserve the status quo, limiting institutional participation and reinforcing policy risk across digital assets.

- Despite high crypto adoption, Latin America continues to face regulatory uncertainty and fragile fiat infrastructure. Coinbase’s suspension of peso on- and off-ramps in Argentina, alongside Brazil’s move to tax crypto-based cross-border payments and stablecoin usage, underscores execution and policy risk even for global Tier 1 players. These constraints limit crypto’s ability to scale beyond trading into payments and financial inclusion, reinforcing dependence on regulatory clarity and banking cooperation across the region.