Strengths

- Regulated on-chain infrastructure is moving from pilot programs to real adoption by large financial institutions. Dubai Insurance, the fourth-largest insurer in the UAE, became the first insurer globally to offer a crypto wallet for paying premiums and receiving claims, partnering with Zodia Custody, backed by Standard Chartered. The launch aligns with the UAE’s post-2024 regulatory framework, signaling that crypto rails are now credible for core insurance cash flows.

- Ethereum leaders are reactivating 70,500 ETH (~$220 million) untouched since the 2016 DAO hack to fund network security. About $13.5 million will be distributed as security grants, while the remaining ETH will be staked to generate roughly $8 million per year. This demonstrates Ethereum’s financial scale and governance maturity, strengthening trust among developers, institutions, and long-term users.

- Talos, an institutional-grade crypto trading and portfolio management provider, raised $45 million in additional funding, bringing total funding to $150 million and valuing the firm at roughly $1.5 billion. With strategic investors including Robinhood, Sony Innovation Fund, Fidelity, and BNY, Talos has doubled revenue and clients for two consecutive years and integrates with BlackRock’s Aladdin, reinforcing its role as core infrastructure for institutional digital asset markets.

Weaknesses

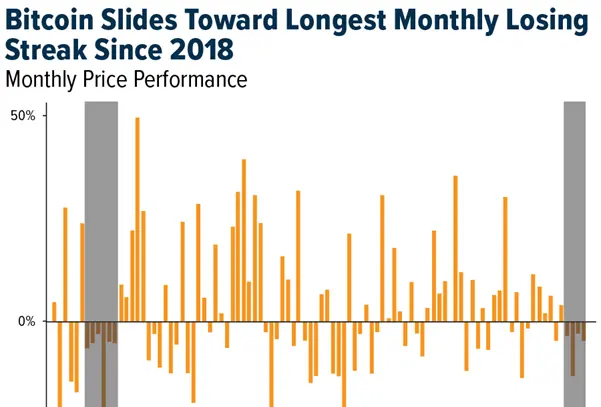

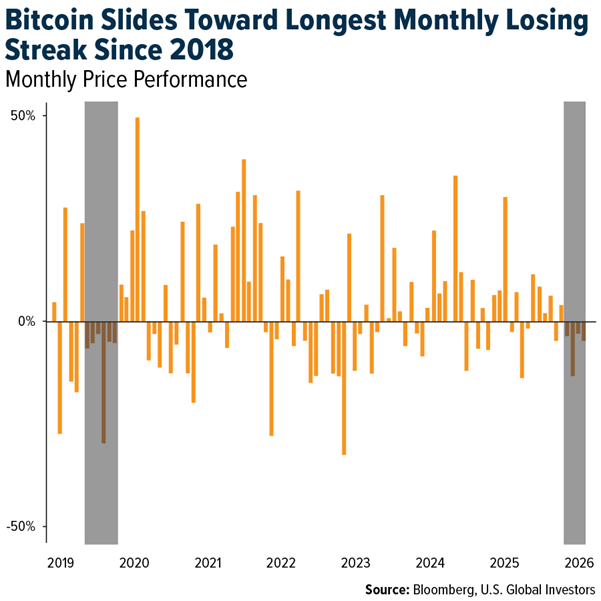

- Bitcoin is showing macro vulnerability, heading for its longest monthly losing streak since 2018, down nearly 6% in January and trading about 30% below recent highs. As investors rotate to traditional safe havens, gold and silver hit record levels, while the total crypto market cap fell over $200 billion, highlighting bitcoin’s high-beta risk behavior in risk-off environments.

- Bitcoin is losing its “digital gold” role, failing to rise when the dollar weakens. While gold and silver saw $1.4 billion in inflows, Bitcoin funds had ~$300 million in outflows, and BTC is down ~30% from its peak. The BTC–gold correlation has turned negative (-0.18), with crypto traders rotating into commodity derivatives, underscoring Bitcoin’s declining appeal as a hedge or safe-haven.

- DeFi’s structure leaves it exposed to future regulatory and tax expansion. While currently outside the EU’s DAC8 framework, the OECD’s CARF rollout shows cross-border crypto tax enforcement will expand globally in 2027. Without identifiable intermediaries, DeFi protocols face rising compliance burdens, regulatory inclusion risk, and increased uncertainty for users.

Opportunities

- Bybit, one of the world’s largest crypto exchanges by trading volume with over 81 million users, is expanding into IBAN-linked fiat accounts to offer bank-like services. This move creates an opportunity to capture deposits, payments, and treasury flows beyond crypto trading. With support for 18 fiat currencies across 200+ jurisdictions, Bybit can position itself as a crypto-native neobank, strengthening user retention and paving the way for U.S. expansion and a potential IPO.

- U.S. regulators are signaling a structural opening for crypto adoption in retirement portfolios, with the SEC stating that the “time is right” for 401(k) plans to include digital assets under proper guardrails. An executive order signed in August 2025 enables access to the roughly $10 trillion U.S. retirement market, while forthcoming SEC–CFTC coordination could establish national standards that accelerate institutional flows and onshore crypto innovation.

- For the first time, a U.S. Senate committee advanced a crypto market structure bill, with the Agriculture Committee voting 12–11 to move it to the next phase. While hurdles remain, the milestone increases the likelihood of clearer SEC–CFTC oversight, potentially unlocking new institutional products, onshore investment, and broader capital participation in U.S. digital asset markets.

Threats

- Russia plans to cap retail crypto purchases at 300,000 rubles (~$4,000) per investor, ban privacy coins like Monero and Zcash, and prohibit crypto for domestic payments, with penalties similar to illegal banking offenses. Only a short list of approved assets, likely including BTC and ETH, would be widely tradable, with all others restricted to “qualified” investors who pass mandatory risk tests. These rules could shrink the retail base, reduce trading volumes, and fragment liquidity, while setting a precedent for other governments.

- UK authorities warn that widespread stablecoin use could drain bank deposits, potentially moving tens of billions of pounds from traditional accounts. Proposed rules require systemic stablecoins to hold at least 40% of reserves at the Bank of England, raising capital and compliance costs and potentially slowing issuance, limiting payment innovation, and reducing credit availability.

- The shutdown of NFT platforms like Rodeo highlights ongoing consolidation risk, as weak user growth and low trading volumes threaten platform survival. Rodeo will cease operations by March 10, following exits like Nifty Gateway, forcing creators and collectors to migrate assets and increasing uncertainty for users while underscoring the fragility of NFT infrastructure.