The banking crisis may no longer be acute, but there are enough risks to consider, such as recession, the collapse of the corporate real estate market, and the Federal Reserve's aggressive monetary policy. If not “cut and run”, perhaps now is the time to fully diversify.

But cash now might not be the best option. Judging by the $5.4 trillion in inflows to money market funds (MDFs), they look much more attractive for weathering the storm or even trying to capitalize on it should Treasury yields plummet.

The question is whether they will really fall, given that new government bonds worth $1 trillion will be issued in the next few months. On the other hand, if the Fed does take a pause, the dollar will not have the best prospects either.

What the heck is a money market fund?

In short, it is a mutual fund that invests in high-quality assets like US government securities and government-sponsored enterprises. It has low risk but offers a yield of around 4%. The minimum initial investment is typically between $500 to $5,000.

As mentioned earlier, money funds allow benefiting from changes in monetary policy. Investors who did not have enough money to buy Treasury bills or corporate securities could invest in the Morgan Stanley Institutional Liquid Government Securities Fund or the State Street US Government Money Market Fund.

Aren't MMFs a direct threat to banks?

In the long run, no. Although there has been a recent change of ownership, the financial industry will eventually stabilize and some funds may come back. However, it remains to be seen how long this process will take if there is a recession in the U.S. economy.

Banks face bigger challenges, such as tighter credit conditions that could negatively impact U.S. economic growth and put pressure on profit margins; new players entering the market, such as Apple, or the introduction of CBDC.

To mitigate risks, investors should consider diversifying their portfolios and ensuring that the banks where they keep their money are capable of withstanding significant changes and avoiding bankruptcy.

What about Europe?

European shares have benefited from a decline in energy prices, the lifting of restrictive measures in China, and the resolution of global supply chain issues, resulting in a decline in freight rates. Still, the outlook remains bleak amid slowing growth and reduced liquidity.

Analysts at Morgan Stanley, for example, expect a 10% correction during the summer months. The pretext for the decline could be problems in the real estate market and shadow banking sector in China, a decline in business activity in the U.S., as well as rising oil prices.

Not surprisingly, money market funds recorded net inflows of €11 billion in April. However, it should be remembered that about 90% of the assets of European money market funds are invested in financial debt, which is not considered any safer than bank deposits.

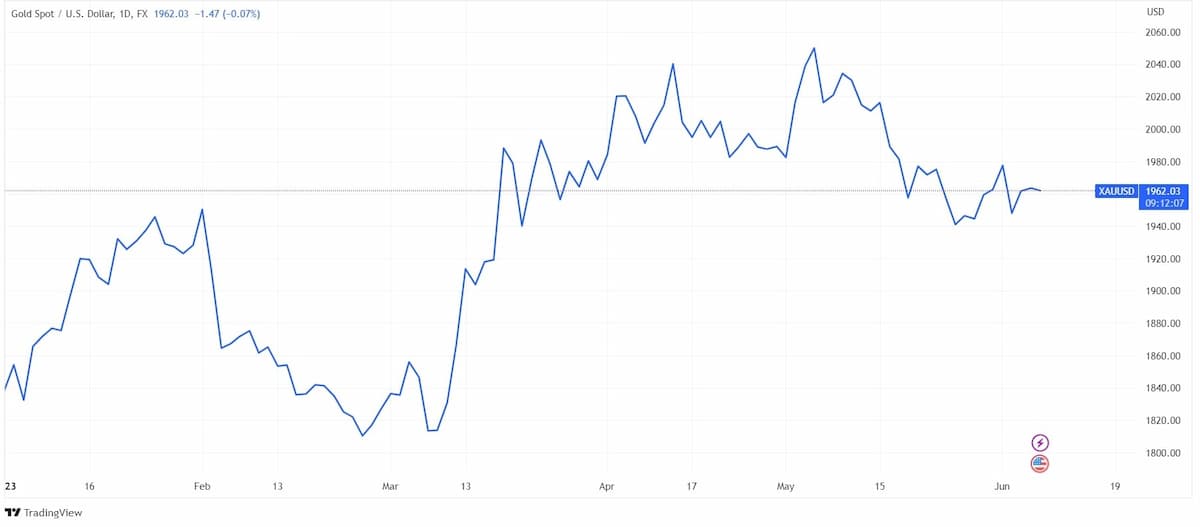

What about gold?

As with the economy, the outlook remains murky. Some expect a decline, others an increase. According to UBS analysts, for example, central banks' appetite for gold could drive its cost up to $2100 by the end of the year.

Historical data also support growth: when 70% of the U.S. government bond yield curve is inverted, gold outperformed the S&P500 in the following 24 months. The challenge now is to reach the traders' heads and shoulders minds and fingers.

However, traders are currently focused on factors such as an overheated labor market, hawkish comments from Fed members, and a strengthening dollar. Unless the rhetoric improves, XAUUSD could drop back to $1,950.

So, who is to be believed? Only your brain cells, or at least your intuition. But if you're considering a short-term investment, be cautious and prepared for potential spikes in volatility. A hint: pay particular attention to the incoming macroeconomic data.