Performance as of May 31, 2023

| Asset | 1 MO* | 3 MO* | YTD* | 1 YR | 3 YR | 5 YR |

U3O8 Uranium Spot Price 1 | 1.58% | 7.35% | 12.99% | 14.37% | 17.20% | 19.14% |

Uranium Mining Equities (Northshore Global Uranium Mining Index) 2 | -2.85% | -10.00% | -4.93% | -10.93% | 33.57% | 16.59% |

| Uranium Junior Mining Equities (Nasdaq Sprott Junior Uranium Miners Index TR) 3 | -4.62% | -17.25% | -16.31% | -25.87% | 35.52% | N/A |

Broad Commodities (BCOM Index) 4 | -6.08% | -7.72% | -13.16% | -25.41% | 15.50% | 1.55% |

U.S. Equities (S&P 500 TR Index) 5 | 0.43% | 5.75% | 9.65% | 2.92% | 12.90% | 11.01% |

Sources: Bloomberg and Sprott Asset Management LP. Data as of May 31, 2023.

*Performance for periods under one year not annualized.

Uranium Grinding Higher

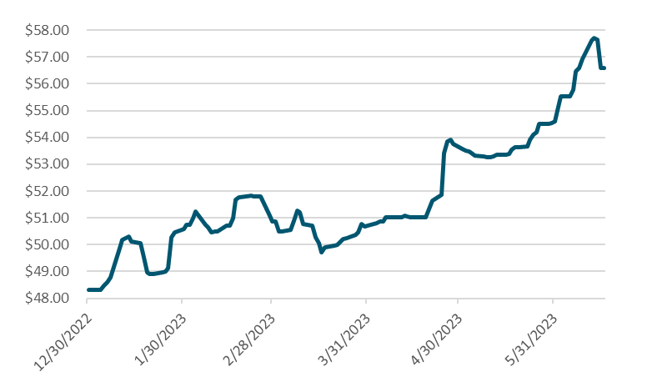

The U3O8 uranium spot price gained 1.58% in May, increasing from US$53.74 to $54.59 per pound as of May 31, 2023. Uranium has posted a healthy 12.99% year-to-date return as of May 31, and continued to show strength and diversification relative to other commodities, which declined 13.16% YTD (as measured by the BCOM Index). The price for uranium continues to be pushed higher, see Figure 1, by growing demand from utilities as they restock their inventories. UxC has noted over 2023 to date, 107 Mlbs of U3O8 has been awarded under term contracts, compared to 125 Mlbs for the whole of 2022.

Kazatomprom (KAP), the world's largest uranium producer, discussed in its annual general meeting notes a major transaction with CNNC, a Chinese utility, totaling more than 50% of the total book value of KAP's assets (i.e., 50% of ~$4.9 BB, implying ~50 Mlbs U3O8 or more at $50/lb).

While 2022 was the highest uranium contacting year in a decade, utilities are still not yet at the annual replacement rate. As a result, we expect the contracting cycle will accelerate as utilities are becoming increasingly concerned about the long-term security of supply.

Concerns about the security of supply were further enflamed by intensifying Western government actions to pivot away from Russia's nuclear fuel supply services.

Figure 1. Physical Uranium Year-to-date Rise (12/31/2022-06/16/2023)

Source: Data as of 06/16/2023. The U3O8 uranium spot price is measured by a proprietary composite of U3O8 spot prices. Included for illustrative purposes only. Past performance is no guarantee of future results.

Over the longer term, uranium has demonstrated even greater resilience within the commodity space. For the five years that ended May 31, 2023, the U3O8 spot price appreciated a cumulative 140.09%1 compared to 7.99% for the BCOM.

Uranium mining equities, in contrast to physical uranium, fell 2.85% in May and are off 4.93% year-to-date. Uranium equities experienced a roller coaster month, rattled by concerns about resource nationalization after Namibia said it would take equity stakes in mining companies.

Despite the short-term weakness, uranium mining equities have had notable long-term results, having gained a cumulative 115.48% for the five years ending May 31, 2023.2

Figure 2. Physical Uranium & Uranium Stocks Have Outperformed Other Asset Classes Over the Past Five Years (05/31/2018-05/31/2023)

Source: Bloomberg and Sprott Asset Management. Data as of 05/31/2023. Gold is measured by GOLDS Comdty Spot Price; S&P 500 TR is measured by the SPX; Uranium miners are measured by the Northshore Global Uranium Mining Index (URNMX index); BCOM is the Bloomberg Commodity Index; US Agg Bond Index is measured by the Bloomberg Barclays US Agg Total Return Value Unhedged USD (LBUSTRUU Index); the U.S. Dollar is measured by DXY Curncy and the U3O8 uranium spot price is measured by a proprietary composite of U3O8 spot prices from TradeTech LLC. Included for illustrative purposes only. Past performance is no guarantee of future results.

Only a Matter Before the Russian Nuclear Fuel Supply Chain is Cut Off

In last month's commentary, we noted that the West has been re-examining its energy supply chains and questioning Russia's role as one of the world's top energy exporters. Subsequently, in May, legislation in the U.S. has been advanced in this regard. The Senate Environment and Public Works Committee (Senate) passed the bipartisan Accelerating Deployment of Versatile, Advanced Nuclear for Clean Energy (ADVANCE) Act.6 Two important aspects of the ADVANCE Act are that it:

- Explicitly prohibits the possession or ownership of enriched uranium owned, controlled or organized by Russia or China unless the Nuclear Regulatory Commission (the Commission) specifically authorizes it.

- Directs the Commission to provide a report on the readiness and capacity to license additional conversion and enrichment capacity to reduce reliance on uranium from Russia.

These developments in the Senate followed additional legislation advanced by the House Energy & Commerce Committee on May 24 in consideration of the U.S. House of Representatives. Namely, the Prohibiting Russian Uranium Imports Act, which aims to ban low-enriched uranium produced in Russia, if doing so would not impede the operation of a nuclear reactor/company in the U.S. Specifically, by detailing limits for yearly imports (~1.3 Mlbs in 2023 to 1 Mlbs in 2027 and then 0 in 2028).7 This legislation must be passed by the House and Senate, and approved by President Biden to be implemented.

The U.S. is not alone in the goal of reducing reliance on Russian uranium services. The U.S., France, Japan, Canada, and the United Kingdom formed the Nuclear Fuel Alliance to specifically focus on dislodging Russian influence over the international nuclear energy market.8 Russia's Rosatom State Nuclear Energy Corporation accounts for more than $1 billion annually to the Russian economy, and impeding this revenue has been another goal of the Alliance.

Russia accounts for a small portion of U3O8 production at 5% of the world's total, but it controls about 27% of the global uranium conversion capacity and 39% of fuel enrichment.9 Given that Russia is clearly not a small player within the uranium fuel cycle and that the developing legislation noted here is aimed at prohibiting their supply, the impetuous for utilities to ensure their security of supply has been accelerated. Further self-sanctioning to mitigate supply disruptions, such as no new contracts being signed with Russian entities, may provide a tailwind for uranium and ultimately bolster uranium miners.

Namibia Nationalization Nullified

News out of Namibia, the third-largest uranium-producing country10 (see Figure 3), temporarily weighed on relevant uranium miners. At the end of May, the Minister of Miners and Energy for Namibia noted that the country is considering taking minority stakes in mining companies. Investor fears of nationalization weighed on stocks such as Paladin Energy Ltd., which owns the Langer Heinrich mine in Namibia. Then on June 1, the ministry noted that "The government has no intention of seizing any stake from existing mineral or petroleum license holders and remains committed to upholding the sanctity of contracts." As such, these uranium miners bounced back at the beginning of June. Namibia did not rule out the opportunity to take minority stakes when granting licenses in the future.

Figure 3. The World's Largest Uranium Producing Countries in 2022, WNA

Nuclear Energy is Crucial to the Energy Transition

Frustratingly, the performance of uranium miners in May did not reflect the sector's increasingly bullish fundamentals. Looking beyond the short-term performance, we believe the uranium bull market still has a long way to run. We believe conversion and enrichment services price increases have started to cascade to the uranium spot price. The long-awaited restart of the ConverDyn conversion facility in Illinois will play a key role in the West's transition away from Russian suppliers. Conversion has been the key bottleneck in the supply chain and this new capacity will finally enable the anticipated shift from underfeeding to overfeeding which will in turn create additional demand for U3O8.

Nuclear energy and uranium's critical role in energy security may likely be paramount going forward. Russia's invasion of Ukraine sparked a global energy crisis that forced many countries to reimagine their energy supply chains. In past years, Western countries' energy policies have predominantly favored renewable energy to reduce reliance on fossil fuels. However, renewables often suffer from intermittency and low capacity and require offsets with baseload energy sources, such as coal, natural gas or nuclear power plants. As the world continues to add renewable capacity to the grids, nuclear energy will have an important role to play, providing the highest capacity factor.

We believe the uranium bull market remains intact despite the uncertain macroeconomic environment. There has been an unprecedented number of announcements for nuclear power plant restarts, life extensions and new builds that are likely to create incremental demand for uranium. However, the current uranium price still remains below incentive levels to restart tier two production, let alone greenfield development.

Figure 4. Uranium Bull Market Continues (1968-2023)

Please click here to see an enlarged chart.

Note: A “bull market" refers to a condition of financial markets where prices are generally rising. A “bear market" refers to a condition of financial markets where prices are generally falling.

Source: TradeTech Data as of 05/31/2023. TradeTech is the leading independent provider of uranium prices and nuclear fuel market information. The uranium prices in this chart dating back to 1968 is sourced exclusively from TradeTech; visit https://www.uranium.info/.