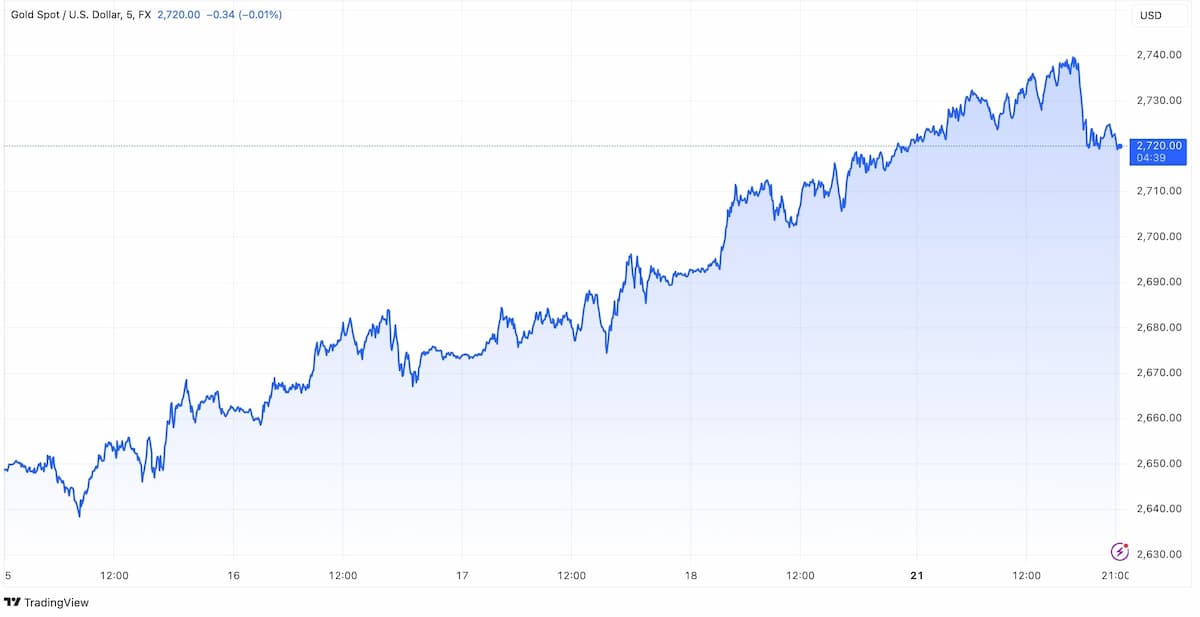

This week has started extraordinarily well for gold prices. The spot price has soared to an impressive $2,720, up more than 32% this year, despite diminishing geopolitical risk.

So, why is this happening, what can we expect next, and is it time to take profits?

Starting with the latter: unfortunately, there is no one-size-fits-all answer. Investment decisions should vary based on individual objectives and risk tolerance, not dizzying market movements.

For example, short-term investors may want to lock in profits or at least part of them, especially if we are talking about risky gold-linked instruments such as derivatives.

For long-term investors, holding on could still be a good strategy. With the Fed's rate cuts and current geopolitical tensions, an upside potential could be above $3,000.

At the same time, prices for other metals, including silver, may continue to rise. When it comes to copper, however, economic stimulus in China needs to yield the desired results. Unfortunately, that seems unlikely.

At the same time, prices of other metals, including silver, may follow. When it comes to copper, however, the economic stimulus in China needs to yield the desired results. Unfortunately, that seems unlikely.

Despite recently announced measures, analysts predict they won’t be enough, and additional government intervention is necessary. But Beijing seems in no rush to take that step.

In general, keep in mind that no market grows without corrections. Therefore, even if there is a fall — of up to 10% — there is no reason to panic and sell at a loss. Of course, this requires nerves of steel.

As for the second question, participants expected significant growth in precious metal prices at the LBMA annual conference: gold could reach $2,941, silver $45, and platinum $1,148 per ounce.

Thus, the outlook seems quite optimistic. However, it is crucial to note that achieving these targets depends on events unfolding as planned, especially regarding Federal Reserve policy.

For example, if the rate-cutting cycle is revised downward in light of extremely optimistic economic data and higher prices, interest in gold could decline, and therefore, prices could fall.

The reason lies in the FOMC's dovish policy, which tends to weaken the dollar, diminishing the value of DXY. This makes gold cheaper as it is priced in US currency. Conversely, a hawkish policy strengthens the dollar.

Finally, there is the geopolitical aspect. If tensions in the Middle East ease and a major conflict is avoided, demand for safe-haven assets such as gold could decrease.