Gold price at record highs, credit spreads at record lows

Gold price (USD/oz) and US credit spread (High Yield Spread*) in percentage points

Source: WGC, Federal Reserve Bank of St. Louis; graph Dr. Polleit’s BOOM & BUST REPORT. - * Yields of US below investment grade bonds over US Treasury yields.

At the end of 2023, the gold price stood at $2,062.60 per ounce. Today, gold trades close to $2,750 per ounce, an increase of over 33 per cent. This was indeed a rather significant price increase that occurred more or less quietly, without major enthusiasm or a media-driven "mega-crisis," and presumably to the astonishment of many market participants. The truth is: It is not an easy task to come up with an explanation for the fulminant gold price rise by taking recourse to "visible data."

For example, central banks acquired 693.5 tons of gold in the first three quarters of this year, which, was less than the increase of 833.4 tons in the first three quarters of 2023. What is more, demand for gold ETFs has been disappointing. While gold ETF holdings increased somewhat in the last five months up to September (latest available figures), gold ETF inflows have remained modest. Also, in the first three quarters of this year, gold demand from India and China – which together accounts for around half of the world’s gold demand – was disappointing, falling 1.2 per cent against the same period last year. In short, the available (historical) data does really not provide a convincing explanation for the most astonishing increase in price of the yellow metal.

Perhaps we should not be overly confident in the information value of the available data? On the one hand, not all gold supply and gold demand components might have been documented correctly. On the other hand, the reported data represent "market-clearing quantities" that have arisen at the respective (average) market price of gold. And as we know, a high market price for gold can correspond with a high(er) or a low(er) market-clearing quantity of gold. That said, a given level of traded quantities does not necessarily have a constant relation to the price of gold.

What is more, there are factors that are usually difficult to measure but have a great impact on the gold price. These factors can be called "imponderables"—non-quantifiable uncertainties, moods, and fluctuations in sentiment on financial markets—that can increase the demand for gold, translating into a higher valuation of gold, expressed in official currencies and relative to stocks and bonds. For instance, one might think of the following: The risk that the war in Ukraine escalates into World War III; that the conflict in the Middle East escalates further; or that, given the growing global debt, investor confidence in bonds and official currencies erodes—not only in the US, but also Europe and Japan as well—potentially triggering a new financial and economic crisis. Of course, all these factors are difficult to quantify as far as their impact on the gold price is concerned, but they can be assumed to have quite some relevance.

Conversely, one can assume that interest rates have been a particularly significant factor for the increase in the gold price so far this year. Generally speaking, the level of interest rates significantly influences the economic attractiveness of holding gold: A high interest rate increases the opportunity cost of holding gold, because gold holders forgo interest income that they could alternatively earn by holding interest-bearing securities. The reverse holds true when interest rates decline: Holding gold becomes more attractive, increasing the demand and thus the price of gold. That said, one would expect that falling interest rates (or just the prospect of future falling interest rates) would increase investor demand for gold and, consequently, push its market price up. This is what has been happening since the beginning of the year: In credit markets, the expectation emerged that the interest rate hiking cycle had peaked and that rates would be cut sooner rather than later (which has indeed been the case: The Fed has slashed borrowing costs by 0.50 basis points in September ’24 – and the gold price rose). The particularly strong rise in the price of gold, however, may have occurred in anticipation of a return to extremely low interest rates (as we expect it—see Dr. Polleit’s BOOM & BUST REPORT, 3 October 2024).

It is one thing to try to understand what has caused the price of gold to rise. The other—and likely much more important issue for investors—is the answer to the question: What’s next for the gold price?

It is reasonable to assume that, as suggested earlier, the current gold price already reflects (at least partially) the anticipation of further declines in interest rates. However, market participants do not seem to expect that short-term US interest rates, in real terms, meaning after inflation is accounted for, will be pushed back down to, or below, zero per cent by the US central bank. However, Dr. Polleit’s BOOM & BUST REPORT thinks that this is very likely to happen. Monetary policy will most likely continue where it left off in early 2022, before key interest rates were raised: creating negative real interest rates, devaluing the purchasing power of money and savings invested in debt securities. This will not only occur in the US but in all major currency areas worldwide. If this expectation proves correct, the gold price will most likely continue to rise over the coming years.

There is another very important factor at work that deserves our attention: As seen in the graph on page 1, the gold price has reached record highs, while credit spreads in the US capital markets have been approaching all-time lows. How should this be interpreted? Clearly, financial market participants expect that the US central bank will fend off large-scale credit defaults. If the economy and/or financial markets falter, investors believe the Fed will come to the rescue. Seen this way, the gold price seems to have already reacted to the thread of future (high) inflation: Investors are betting on gold because its value cannot be debased by inflation caused by central banks, and it won’t take a hit in a credit event. And this idea is actually the key reason why the gold bull market is far from over; People will increasingly rely on gold – in the US, Canada, Europe and of course Asia, actually the world over.

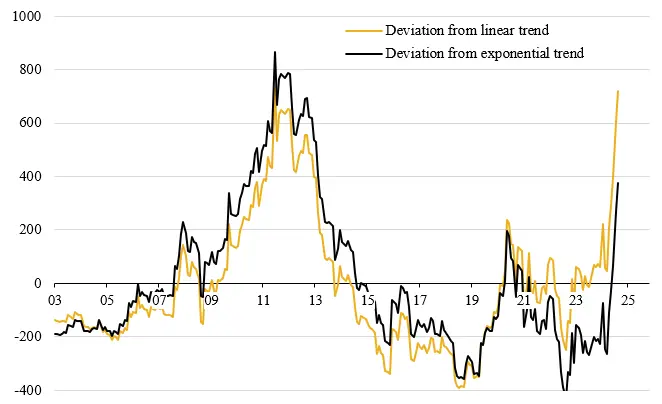

Gold has become more expensive … hasn’t it?

Deviations from trends in US-Dollar per ounce

Source: WGC; calculation and graph Dr. Polleit’s BOOM & BUST REPORT.

Nevertheless, there are reasons for the investor to exercise caution: Could the dramatic rise in the gold price over the past ten months mean that gold is now significantly overvalued? Indeed, one can see from figure 2 that the gold price trades now significantly above long-term trend lines. If we use a linear trend, the gold price is currently about 720 USD/oz above its trend value; with an exponential trend, the deviation is about $375 USD/oz. In this view, the gold price should actually trade between $2,000 and $2,400 per ounce instead of $2,750 per ounce. From this perspective, the current gold price seems to have a correction potential of 14 to 26 per cent.

But are the underlying trends we used reliable? Perhaps gold has assumed a new underlying megatrend—so that the simple extrapolation of what has happened in the gold price over the past 20 years is no longer a reliable indicator for the future market price of gold? The answer to these questions is, in our opinion, yes! Gold is (gain) getting peoples’ preferred “safe haven asset”.

So what should the investor do with these insights? Dr. Polleit’s BOOM & BUST REPORT recommendation is as follows: Those who wish to invest long-term, meaning with a time horizon of 5 years or more, should keep building up and expand their physical gold positions—and should not be deterred by the alleged price deviations from their trend value as outlined above. And in view of the current market momentum, those who trade gold with a short(er) horizon (that is, say, of 3 to 9 months) have also good reasons to take long gold positions for the time being. However, they should be aware that there is a non-negligible potential for significantly lower gold prices, at least temporarily. ■