Whether in the U.S., Europe, or Japan: bond yields are rising.

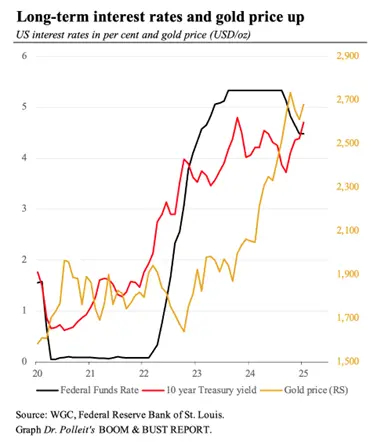

For instance, the U.S. Fed has reduced its key interest rate by 1 percentage point from September 2024 until today. But long-term yields have not declined, as is usually the case if the central bank cuts interest rates, but gone up.

The yield on the 10-year US Treasury bond has risen by almost a full percentage point from 3.8 to 4.7 per cent—the highest level since October 2023. And the yield on 30-year US government bonds has nearly reached 5 per cent—a record high since the spring 2007.

Why have yields gone up?

It could be that yields are rising because investors expect higher economic growth. That would be a rather positive scenario, and no cause for major concern. Or do investors perhaps fear a deterioration in the credit quality of borrowers and/or higher future inflation? In that case serious trouble would be ahead.

Because economies worldwide are highly indebted. The Institute of International Finance (IIF) estimates that global debt had reached 323 trillion U.S. dollar in the third quarter of 2023, amounting to 326 per cent of global economic output. A very high ratio by any standard—though it is about 30 percentage points below its record level in 2020/2021.

The sky-high debt ratio is a cause of serious concern, especially so as it has been increased in a period of extremely low interest rates, a result of central bank policy, and the already existing debt has been refinanced at very low borrowing costs.

As a result, the rise in interest rates is now putting increasing pressure on borrowers. It affects households, companies, and especially states (whose debt, by the way, is ultimately borne not by the government but by net taxpayers).

But it’s not only the borrowers who are under pressure when interest rates remain elevated or rise further. The entire economy takes a hit.

As interest rates rise, many entrepreneurs realize that their investments, made during times of artificially low interest rates, are no longer profitable in an environment of higher yields, causing corporate bankruptcies, job losses, and an economic slowdown, further deteriorating the economic situation and reducing the debt sustainability of the economy.

The key question is: Why are yields rising?

It is likely that the reasons differ across various currency areas. For example, in the U.S., higher yields probably reflect the expectation that economic expansion will likely accelerate under the new presidency of Donald J. Trump. And a rise in U.S. interest rates exerts a pull effect on yields in other currency areas around the world, especially in Europe.

However, it cannot be dismissed out of hand that investors have become increasingly concerned about credit quality, particularly of the quality of government debt—because investors may expect politicians to continue with their reckless deficit spending policy. Where could this lead?

Well, September 2022 comes to mind, when UK government bond prices collapsed: The government had promised tax cuts without accompanying spending cuts, which would have led to rising deficits. As a result, yields on UK government bonds spiked, threatening to collapse the entire UK financial system. It didn’t take long, and the Bank of England intervened in the market by buying bonds, pushing yields back to politically acceptable levels, and markets relaxed.

This episode clearly shows how quickly a dramatic sell-off in government bond markets can occur, which—if it doesn't stop—could make the tower of debt coming crashing down, even crashing the entire fiat money system.

Because the unpleasant truth is this: In today fiat money system, government debt is actually a ponzi game. Governments borrow without intending to ever repaying down their debt. Instead, the idea is to replace maturing debt with new debt, and on top of it, to borrow even more.

Such a Ponzi scheme works as long as investors believe that not only today but also in the future, there will be buyers for government bonds. And so investors buy government bonds today because they expect that there will be future buyers for newly issued bonds, which the government will use to pay off maturing debt.

But if investors begin to doubt that there will be buyers in the future willing to finance the growing debt burden, the Ponzi scheme is nearing its end, taking a bad turn. This is what was about to happen when there was the gilt sell off in September 2022—had the Bank of England not intervened.

The practise of central banks bailing out the fiat money system is, however, highly problematic. It does not only encourage reckless behaviour on the part of the investor community—in terms of borrowing too much, and lending too much at too low an interest rate, aggravating debt accumulation.

It also makes people, in time of crisis, considering the expansion of the money supply by the central bank as the policy of the least evil—meaning that the economy slides into a policy of high inflation or, in the worst-case scenario, hyperinflation.

Investors should know that central banks can, if they want, perfectly control market interest rates perfectly—by being willing to buy bonds in the capital market. Under such a policy, however, central banks lose control over the money supply and therefore inflation.

What can we expect in the near future?

One of the most important issues is what the Trump administration will do about the precarious state of US public finances. The announcement to rein in the deep state, reduce government spending, and stimulate economic growth by lowering energy prices could help alleviate the situation—and I find it quite likely that at least some progress will be made on that front, so that the rise in U.S. bond yields will stop soon, and that yields will decline again over the course of the year.

The situation in the euro area looks more problematic—especially Italy and France will likely not be able to shoulder their debts without financial subsidies from the European Central Bank, and Germany’s economy contracts, dragging production and employment in the euro area down with it.

Furthermore, there are few signs for a significant political change in continental Europe. Economic decline will likely have to worsen before any significant changes in the current policy course occurs.

Against this backdrop investors will most likely demand higher yields for holding Euro government bonds—and this will prompt the European Central Bank to increase the money supply again, causing a new wave of inflation. This is perhaps also a major reason why the euro has been depreciating against the US dollar.

In some sense, the euro area could follow Japan’s example: Since around 2020, Japanese capital market yields have been rising, translating into higher interest rate payments on government debt, undermining confidence in the yen, causing its external value to fall against the US dollar.

What should the investor do?

Well, take very seriously what is happening in credit markets and to interest rates. If you personally conclude that the rise in rates can no longer be stopped and reversed, if there will be a bond bust, then run for cover, expect a crash scenario.

However, as mentioned earlier, such a scenario is not, at least not yet, inevitable.

No matter how bond and loan markets develop, it is advisable for investors to keep part of their portfolio in gold. Because in an environment where fiat money system disequilibria are growing, the price of gold will likely become increasingly independent from movements in interest rates.

Also note that gold is the ultimate currency of mankind, and it has successfully weathered many storms in history. Gold, in this sense, is insurance against the vagaries of fiat money, an insurance that will gain in value. To cut a long story short: It makes a lot of sense to hold gold—it will help reduce portfolio risk while also increasing portfolio returns.

Of course, the elevated uncertainty in credit markets does not offer support for stock market prices, at least not in the short term. However, there are good reasons for long-term investors to remain positioned in the stock market—preferably in companies with inflation-resistant business models.

If you would like to learn more about what the investor should do in challenging times, please check out Dr. Polleit’s BOOM & BUST REPORT—for investors who really want to know. All information can be found on my website at www.boombustreport.com.