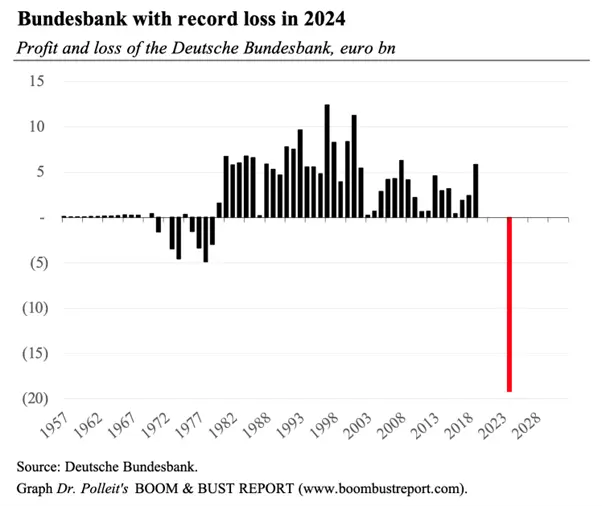

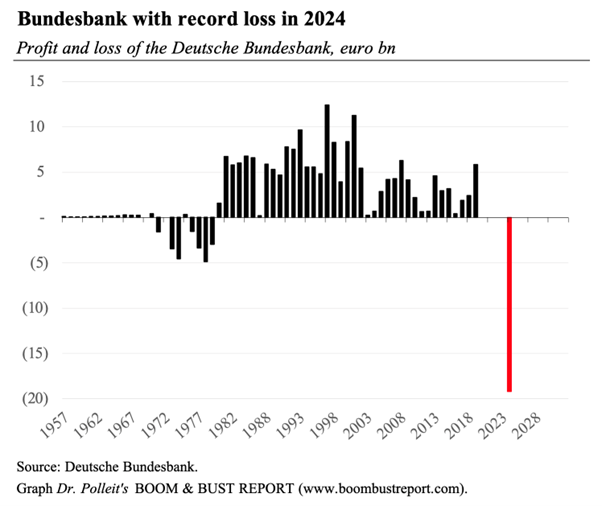

On February 25, 2025, the Deutsche Bundesbank presented its annual report for 2024, revealing a loss of 19.2 billion euros. Is that a lot? Yes, it is. In fact, it is a huge loss, equivalent to 7.2% of the Bundesbank's equity capital and almost half a percentage point of Germany's GDP. It is the first loss since the 1970s (when the Bretton Woods system collapsed, and the Bundesbank had to write off the market value of its US dollar reserves).

You ask: Why is the Bundesbank making losses now? Well, there are two answers to that.

The first answer: The Bundesbank has bought bonds in the past at completely inflated prices. You surely remember: central banks had driven interest rates to extremely low levels just a few years ago, and as a result, bond prices soared to stratospheric levels, and central banks, including the Bundesbank, bought the bonds at these inflated prices.

However, central banks have since raised interest rates again, and as a result, bond prices have collapsed, causing book losses for the Bundesbank.

At the end of 2023, the Bundesbank had securities holdings of 1 trillion euros, but by the end of 2024, this number had dropped to 910.9 billion euros—because some bonds were redeemed over the course of the year.

What's important, however, is that the bonds on the Bundesbank's balance sheet are not recorded at market values, but at acquisition costs—the Bundesbank does not adhere to the accounting principles of the corporate world, which promote transparency and honesty.

As a result, the bank’s accounting losses remain concealed from prying eyes. (Just to give you an idea: a 10-year bond with a nominal value of 100 euros and a 1% coupon has a market value of 100 euros. If the interest rate rises to, say, 2.5%, the market value of the bond drops by 14%, to 86 euros.)

Even if one doesn’t know the details: we can sense that the unreported losses on the Bundesbank's balance sheet are probably huge.

The second answer: In 2024, the Bundesbank made a loss of 13.1 billion euros from net interest income, compared to a 13.9 billion euro loss in 2023. How come? Well, the Bundesbank is earning less interest on its bond portfolio than it pays out to the German banks. Yes, you’ve heard correctly: the Bundesbank pays interest to the banks. The deposits that the banks hold with the Bundesbank are even generously rewarded. At the beginning of the year, banks were getting 4%, but following the European Central Bank interest rate cuts, it is now only 2.75%. Some private investors might only marvel at that.

You ask: Who got the money that the Bundesbank lost? Well, here's the answer: Those who sold bonds to the Bundesbank at inflated prices received the money. So primarily banks, hedge funds, and other institutional investors. Also, the banks received money from the Bundesbank by holding interest bearing deposits (which carry no default risk) at the Bundesbank.

Who suffers from the loss on the Bundesbank's balance sheet? Well, simply put, it harms all those who, literally speaking, didn’t receive any money from the Bundesbank. Those who were given new money from the Bundesbank are the beneficiaries, while those who didn’t are the disadvantaged.

From an economic perspective, however, one should not mourn the fact that the Bundesbank won't be paying a profit to the state due to its loss (as it has not done since 2020 due to a lack of profits). Because a central bank profit does not make the economy richer. A central bank profit is essentially money creation out of nothing.

Sure, politicians are happy when they receive new money from the central bank because it allows them to fund their policies, bribe voters, and especially pay themselves.

But the central bank profit (i.e., an increase in the money supply for the state) does not make the economy wealthier. (If it were, we could make all the people in the world rich simply by giving them newly created money. But we know that this isn’t true.)

The central bank profit enriches (like any money supply increase) only a few at the expense of many others, reducing the purchasing power of money.

There is a silver lining, if you can call it that, that should still be mentioned in this context: The Bundesbank famously holds around 3,350 tons of gold (making it the second-largest gold holder in the world after the US Treasury). The gold reserve is recorded on the asset side of the Bundesbank’s balance sheet at market values, which at the end of 2024 amounted to 270 billion euros. Since the market price of gold has risen, the Bundesbank made a valuation gain of 69.2 billion euros in 2024. This gain was transferred into the so-called revaluation reserve, which counts towards equity, thus increasing the bank’s capital base. Without this gold gain, the Bundesbank's balance sheet loss would have been much higher!

What can we learn from all of this? Well, the key lesson is: Don’t get distracted from the bigger picture. The Bundesbank is a central bank that, in conjunction with other European central banks, creates the fiat euro currency out of thin air. And the fiat euro (like any fiat money) is economically and ethically deeply flawed.

The Bundesbank’s loss in 2024 should remind us that this time it’s not the state benefiting from the Bundesbank’s money creation, but rather— as I already said—the banks and the financial industry, to the detriment of everyone else.

Above all, however, the Bundesbank’s loss should remind us that fiat money is literally ruining an economy. This is well-known both in theory and in practice. And if the Bundesbank’s loss in 2024 makes you think that something is wrong with our money, with the euro, then you can be sure that your feeling is not misleading. And so I close with the words of the U.S. economist Irving Fisher, who wrote that irredeemable paper money (that is, fiat money like the euro) has always proven to be a curse for the economies that use it.

If you want to know what this means for your money, your savings, then read Dr. Polleit’s BOOM & BUST REPORT. You should not miss our analysis and recommendations. All information at www.boombustreport.com.