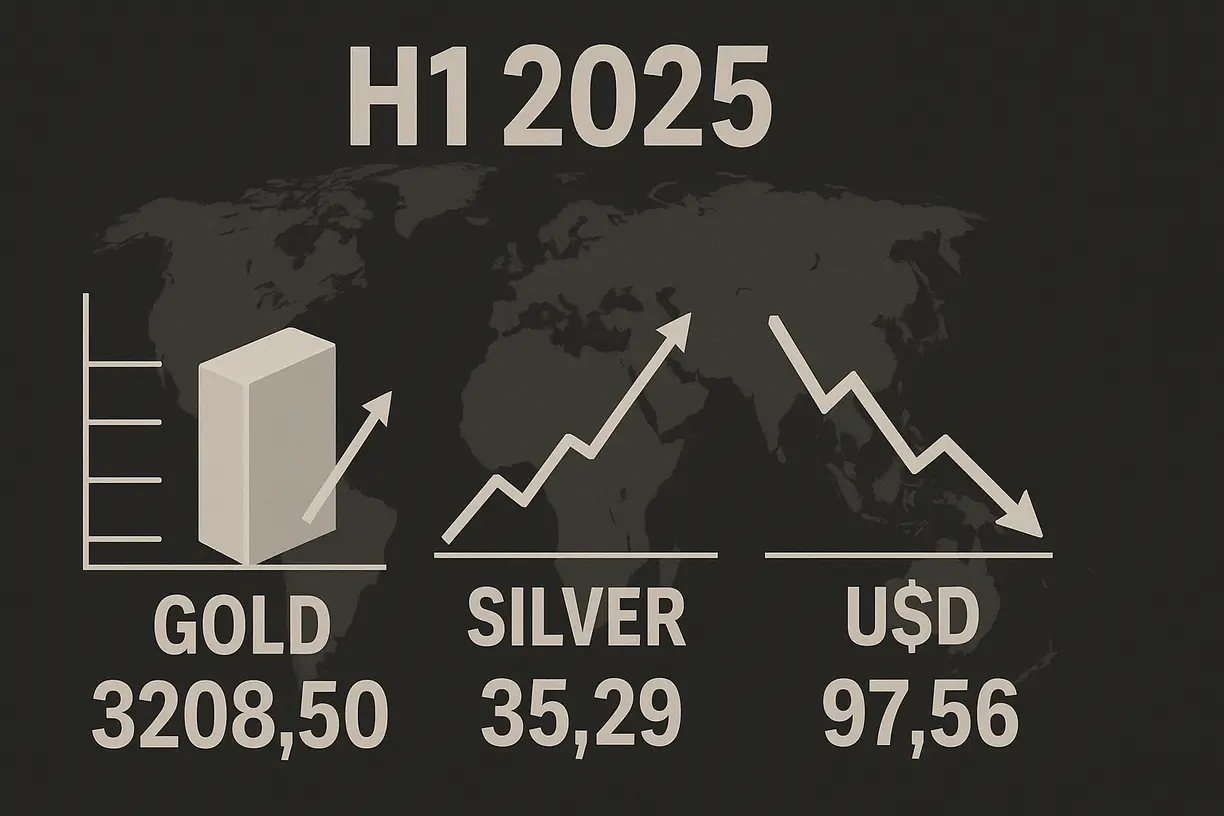

(Kitco Commentary) - As we head into the end of H1 2025, buying interest in gold is being limited by de-escalating tensions in the Middle East that have boosted risk appetite, while the silver price continues to catch up with gold following a test of the recent silver breakout at $35 on Tuesday.

With the war premium in the gold price fading, U.S. "big, beautiful bill" debt concerns taking the USDX below key support at 98 has both Gold and Silver Futures remaining in bullish consolidation of outsized gains above key support at $3200 and $35, respectively, heading into H2 2025.

Republicans in the U.S. Congress were scrambling to resolve nettlesome tax and health care provisions in their sweeping tax-cut and spending bill on Thursday, as President Donald Trump pressed law makers to pass it by a July 4 deadline.

The proposed U.S. spending bill is projected to add about $2.4 trillion to the national debt over the next 10 years, with the failure to address growing deficits only worsening the outlook for long-term debt management.

The debt burden is growing with no end in sight, and the cost of financing it is spiraling out of control. Interest payments alone topped $92 billion in May, surpassing nearly every other federal expense except Medicare and Social Security.

In May alone, the U.S. government collected $371 billion in revenue and spent $687 billion, leaving a $316 billion deficit in just one month.

It’s no wonder the battered U.S. dollar took another beating this week, as investors were also unnerved by fresh signs of an erosion in U.S. central bank independence, pushing the world's reserve currency down to its lowest levels in over three years.

Donald Trump on Wednesday called Federal Reserve Chair Jerome Powell "terrible" in his latest attack on the Fed chief and said he has three or four people in mind as contenders for the top job heading the U.S. central bank.

Dollar selling continued after the Wall Street Journal said the U.S. president - who has been urging the Fed to cut rates faster - was toying with the idea of selecting Powell's replacement in the next few months ahead of his formal departure in May next year.

The move this week in the world's reserve currency left the greenback down more than 10% for the year. If the USDX stays down below 98 by the end of Q2 on Monday, it will be the biggest fall in the first half of a year since the start of the era of free-floating currencies in the early 1970s.

Another reminder of the 1970s is stagflation fears returning to the marketplace this week as well, along with the possibility of further oil shocks. As war spreads in the Middle East, oil-exporting nations face mounting threats to their infrastructure and output.

Although the oil price cratered after President Trump announced a ceasefire between Israel and Iran to begin the week, there are still bullets being shot from both sides while the war against Hamas in Gaza is still grinding on.

On Sunday, Iranian lawmakers publicly supported closing the Strait of Hormuz, where nearly 25% of global oil and 20% of LNG passes through a narrow corridor.

A major oil price shock from a Hormuz closure would likely trigger a global recession and a 20%+ decline in equity markets, based on historical precedent.

Historically, in every single business cycle recession in which an oil price shock has been a factor, the U.S. equity market has experienced a major stock market decline of -15% or more.

Notably, the bear market of 1973-1974, which was triggered by the Arab Oil embargo, resulted in a very severe bear market decline of over 40% – one which took over a decade for U.S. stocks to recover from in real (inflation-adjusted) terms.

As war continues in the Middle East, energy costs are beginning to ripple across the broader economy as growth concerns persist – reigniting stagflation fears just as central banks were preparing to ease policy.

Last week, the Fed stuck to its forecast of two interest-rate cuts in 2025, despite seeing a burst of inflation coming in the next few months because of higher tariffs.

In an updated forecast, Fed officials now expect inflation as measured by the core PCE index to jump to 3.1% by the end of the year, up from a rate of 2.5% in April, to rise further away from the central bank's fantasy 2% mandated target.

In his day-one opening remarks on Tuesday before the U.S. House of Representatives Committee on Financial Services, Federal Reserve Chairman Jerome Powell reiterated the central bank’s stance that it is in no hurry to shift its current position.

After months of signaling rate cuts in the second half of the year, another surge in oil prices would threaten to derail the Federal Reserve's plans. There is no denying that the world's most powerful central bank is stuck between a rock and a hard place.

The Fed is terrified of crashing the bond market if it hikes too fast, and equally terrified of sparking a dollar collapse if it cuts too soon. Raising interest rates can have no impact on demand, as the government continues to borrow more and the central bank simply has no say.

Federal Reserve Bank of New York President John Williams expects slower growth and higher inflation this year due in large part to trade tariffs, in comments this week from an event held in Albany, New York that gave little in the way of guidance for what’s next for central bank interest rate policy.

“I expect uncertainty and tariffs to restrain spending and reduced immigration to slow labor force growth,” Williams said. Slowing growth in the economy and the labor force, along with higher inflation, equals stagflation.

The comment from Williams was made a few days before the Commerce Department's Bureau of Economic Analysis (BEA) said in its third estimate of GDP on Thursday that the U.S. economy contracted a bit faster than previously thought in the first quarter amid tepid consumer spending, underscoring the distortions caused by the Trump administration's aggressive tariffs on imported goods.

Central banks and investors alike are moving to gold as a hedge against both economic and political risk, while governments continue to borrow perpetually with no real intention of paying back their debts.

Therefore, we are experiencing a drastic shift away from public confidence worldwide, and that is causing capital to lose confidence in governments that are already deeply indebted.

Permanent deficits are a global reality, with fiat losing its value now more rapidly as a result. Government debt is no longer viewed as a safe-haven, and the only true safeguard is owning gold which has no counterparty risk.

Meanwhile, higher-risk silver stocks are showing relative strength as both gold and silver consolidate recent gains. Gold stocks sold down to fill monthly upside gaps in GDX and GDXJ this week, as silver ETFs moved closer to multi-year resistance.

As gold and silver miner ETFs consolidate recent gains with quarter-end book-squaring in mind, higher-risk quality juniors are setting up for continued gains following a recent major breakout in a closely followed Canadian junior index.

The weekly Canadian TSX-Venture chart (CDNX), where 50% of its holdings are small-cap junior resource stocks, broke out of a huge accumulative 3-year base in May.

Although the TSX-V has been making 52-week highs along with the miners, it remains over 75% below its all-time high reached in 2007 and 35% from its highs seen in 2021. And that is in nominal terms, not inflation-adjusted terms.

Following a spike low at 330 in early 2020, the TSX had tripled in just one year. A similar move back to the peak at 1113 in January 2021, would be a 75% rise from the recent breakout at 640.

At Junior Miner Junky (JMJ), my subscribers and I have accumulated shares in a basket of quality gold, silver, and copper related juniors, ahead of the recent major breakout in the mining sector.

The real-money JMJ Portfolio is up 80% thus far is 2025, outperforming both GDX and GDXJ. With the sector consolidating recent outsized gains, weakness is being bought quickly in the quality issues.

The JMJ weekly newsletter is a one-stop shop for precious metals stock speculators. Along with providing detailed macro commentary and technical analysis for subscribers following the real-money JMJ junior portfolio, the letter also teaches its members risk management via successful selling strategies.

If you require assistance in accumulating the best in breed precious metals related juniors, and would like to receive my research, newsletter, portfolio, watch list, and trade alerts, please click here for instant access.