Following a 3-session 21% decline in the gold price at the end of last month, accompanied by a staggering 6-session 47% silver nosedive into the first week of February, the mining complex barely flinched after rising over 175% in 2025.

Since both silver and gold’s parabolic peaks near the end of January, the miners lost just 20% during a brief 3-week correction and are now testing recent multi-year highs into month-end.

Although the mining sector is already up another 25% since the beginning of 2026, this bull still has a long way to run after the latest consolidation process runs its course.

Ongoing currency debasement, U.S. threats of war against Iran, a tariff showdown between the Supreme Court and the White House, along with recent stagflationary U.S. economic data during fears of a Sovereign Debt Crisis has investors rotating stock market gains into the under-owned precious metals mining complex.

Gold Futures began an attempt to break out to the upside of a bullish 3-week symmetrical triangle consolidation after stagflationary U.S. economic data was released last Friday.

The U.S. economy ended 2025 on weak footing with Q4 GDP increasing at just a 1.4% annualized rate, as economic activity was significantly weaker than expected.

At the same time, PCE inflation remains stubbornly elevated at a full 1% above the Fed's fantasy 2% target with a weakening jobs market to signal stagflation, which is a healthy environment for both gold and silver.

The Supreme Court's takedown of President Donald Trump's tariffs last Friday infused new risks and uncertainties into trade policy, U.S. debt, and the dollar as the country may be on the hook for $175 billion worth of refunds.

The Commander-in Chief's furious rush to impose replacement levies has already drawn immediate criticism from Europe, who has demanded the U.S. stick to the terms of an EU-U.S. trade deal reached last year, along with fresh confusion about trade policy.

Safe-haven gold buying is also being featured after President Trump briefly laid out his case for a possible attack on Iran in his State of the Union speech to Congress on Tuesday, while the U.S. is causing pure tariff chaos around the world.

As the uncertainty over duties and war continues into month-end, the mining sector is leading the metals higher and breaking out against the stock market.

In terms of gold, the S&P 500 has lost nearly 50%, while in silver terms the best single gauge of large-cap U.S. equities is down over 50% since the beginning of 2024.

This is proof that owning gold and silver has been a far better bet than owning general equities. Yet, Wall Street has done a good job keeping generalist investors out of "risky" gold stocks until only recently.

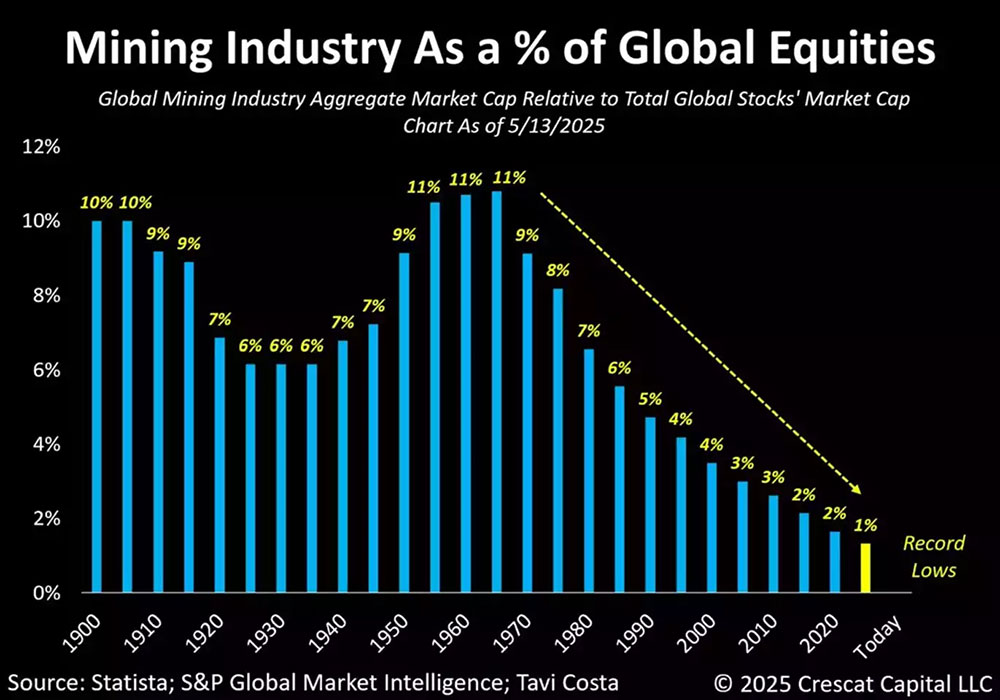

The mining industry as a percentage of global equities, Crescat points out in this chart, is at an all-time low of just 1%. If mining shares just returned to the percentage of the total investment market in 1970, when the sector peaked at 11%, they would have to go up 1000%.

{kind=link}

Incredibly, this under-investment of the masses remains even as Q4 and full year 2025 financials being released by the miners this month is proving to be one of the best earnings seasons this industry has ever seen. Free cash flow is running at 3-5x what precious metals miners generated just two years ago.

Furthermore, balance sheets are the cleanest they have been in decades. Miners have paid down debt, built up large cash reserves, and instead of chasing risky acquisitions (an outdated strategy that burned investors in 2011), most producers are returning some of that cash to shareholders through dividends and buybacks while funding growth organically.

With AISC for most of these companies in the $1400-$1800 range and gold trading above $5200/oz, every ounce produced delivers a whopping $3200+ in margin.

This kind of profitability not only improves balance sheets but it is forcing Wall Street to value a sector they have shunned for over a decade much higher.

Due to most generalist investors having yet to discover this tiny sector, precious metals stocks continue to trade at valuations that assume gold is still below $3000/oz. But the gap between what these companies are actually earning and what the market is pricing in will not last forever.

Meanwhile, silver miner valuations have companies trading as if the silver price is still below $50/oz, a price the metal took 45-years to breach.

Following the silver price zooming to $121/oz last month, the ratio of silver mining stocks to silver itself (SIL/Silver) bounced sharply from a major spike low during the late January silver crash, favoring silver stocks over the metal going forward.

For silver miners specifically, the historical pattern of 3-5x leverage to metal prices is set to play out as generalists have recently begun to return to the mining space.

As analyst upgrades keep rolling in following record-breaking 2025 earnings, weakness is being bought quickly during the recent miner pullback.

Several major miners also increased dividends this month, while the Street's darling Nvidia plunged 5.3% Thursday, despite reporting a jump in profit and record income a day earlier.

The AI sector has been a huge strength for the U.S. stock market for the past couple of years. But coming into the new year, investors have begun to realize the recent downdraft is more of a problem than an opportunity.

The MAGS ETF offers equal weight exposure to the “Magnificent Seven” (MAG-7) stocks – i.e., Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla.

MAGS has gone nowhere since September 2025, as the sector appears to be forming a 6-month rounded top, while the NASDAQ has been negatively diverging from the Dow Industrials.

MAG-7 companies are now spending over $400B per year on AI infrastructure. The spending is so massive that companies like Meta and Google are issuing debt to finance it.

This has left less cash on the books for buybacks. Without the $250 billion annual bid for stock buybacks underneath their shares, the MAG-7 has lost its single biggest support mechanism and smart money already knows it.

A big part of the reason general equities have outperformed the precious metals mining sector for over a decade is due to the success of the technology sector.

Take that away, and there is potential for a bigger rotation into the relatively tiny precious metals mining sector. Nvidia’s 5.3% drop yesterday erased $260 billion in market cap in a single trading session, while the combined market cap of the entire precious metals mining sector is just around $1 trillion.

Understandably, investors look to be giving up on trying to value software and technology companies amid the risk of AI disruption and have begun to turn toward the undervalued and under-owned gold, silver, and copper mining space.

Moreover, Bitcoin's deep correction is likely far from over, given the history of previous cycles. Following its 2017 and 2021 rallies, the largest crypto bellwether corrected between 70% and 75% from the all-time high.

If the pattern repeats itself, Bitcoin could slip to the $31,000 level, erasing all gains since October 2023. This is likely to occur if institutions are under pressure to shed their BTC holdings, Bitcoin Treasury companies sell Bitcoin, and capital rotates from Bitcoin into gold, the prevailing safe haven.

Two key levels to watch are the $60,000 support and the $70,000 resistance. A clean break above $70,000 could hint at a recovery in Bitcoin in the coming weeks.

Conversely, a firm breakdown below $60,000 could trigger further liquidations and extend Bitcoin’s current bleed and see more rotation into the gold complex.

The extraordinary rise in both precious metals is the marketplace screaming that the global sovereign debt spiral has reached terminal velocity intermixed with increasing geopolitical turmoil, while generalist investment institutions and retail investors have only recently started to return to the gold mining complex after leaving en masse in 2012.

Their recent return to this tiny sector is evidenced by several important benchmark precious metals sector ratio trades beginning to break out above significant 12-year resistance levels.

Specifically, the GDX/Gold ratio, GDX/SPX ratio, Gold/SPX ratio are breaking out to the upside from a strong multi-year accumulative base, following the Silver/SPX ratio having already done so in January.

Meanwhile, the higher-risk TSX-Venture Exchange ($CDNX) is breaking out to 12-year high's with strong volume. A monthly close above major resistance at 1050 later today would be a significant technical breakout, with the target being over 150% higher at the 2011 high of 2465 when the gold price was $1800/oz.

With the marketplace only just beginning to wake up to the miners absurd disconnect from metals prices, mining stocks still have a lot of catching up to do.

After JMJ painstakingly accumulated and recommended positions in high quality gold, silver, and copper related juniors heading into 2025, the recent price action is why being right and sitting tight is the best course of action following a confirmed significant breakout in this tiny sector.

Trimming large positions along the way, while holding core positions until the bull market matures, continues to be recommended.

The JMJ newsletter is a one-stop shop for precious metals stock speculators, maintaining a high net-worth real money portfolio, which was up 265% in 2025.

The service is completely transparent, and assists in teaching its members how to carefully construct and maintain a successful junior resource stock portfolio.

Subscribers are provided a carefully thought-out rationale for buying individual stocks, as well as an equally calculated exit strategy. Although the 500 subscriber limit has recently been reached, click here to be placed on the Waiting List.