Strengths

- The best performing precious metal for the week was gold, up 0.56%. Gold regained ground this week, breaking a two-week run of losses when the weaker than expected U.S. jobs growth was reported and prior numbers being revised down too. This sparked a rally in gold on Friday as expectations of a September rate cut became more probable. Adding fuel to the fire, U.S. factory activity contracted in July at the fastest rate in nine months and sliding to the lowest reading in more than five years, according to Bloomberg.

- According to Scotia, B2Gold announced that it has received approval from the state of Mali to begin underground mining at its Fekola Complex as of July 30, 2025. Throughout 2024 and 2025, the company had completed development work and installation of all required underground infrastructure in anticipation of receiving the required approvals, so stope ore production from the underground has already begun.

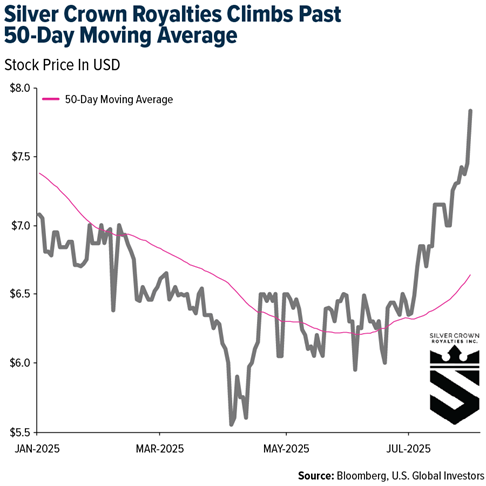

- The amendment to Silver Crown Royalties' silver royalty agreement with PPX Mining Corp. strengthens the company's position, as it increases the silver royalty to 11.1% and provides flexibility in the payment structure, positioning Silver Crown to capitalize on the initial phase of the Beneficiation Plant's operation. This strategic move, coupled with Silver Crown's stock breaking above its 50-day moving average, underscores the company's ability to enhance shareholder value even in a volatile market.

Weaknesses

- The worst-performing precious metal for the week was platinum, down 6.44%. Platinum, which had been trading at a premium on U.S. futures markets, sold off nearly 6% after Trump’s surprise decision to exempt refined copper from immediate tariffs, undermining trader expectations of similar protectionist moves for other critical metals. The sudden unwind erased the U.S.-London premium and triggered a wave of position exits, as American platinum companies and warehouse inventories came under pressure from a sharp sentiment reversal.

- Greatland Gold has reported a disappointing moderation for FY26 guidance, according to Canaccord, now forecasting production of 260,000–310,000 ounces and all-in sustaining cost guidance of A$2,400–2,800 per ounce. The moderation reflects additional risk weighting for lower grades in the run-of-mine stockpiles (inherited from Newmont) and unmined open-pit material.

- Putting it all together, and excluding over-the-counter transactions, gold demand increased by a solid 10.4% year-over-year in the past quarter, although this was slightly below the 15% year-over-year expansion in Q1 2025. This is one reason prices have remained resilient but have not pushed higher. Of course, the recent hawkish Federal Open Market Committee meeting also dampens a near-term bullish narrative, according to Bank of America.

Opportunities

- According to Canaccord, Torex Gold announced it will acquire Prime Mining in an all-share deal valued at C$449 million, adding the advanced-stage Los Reyes gold-silver project in Mexico and expanding its development pipeline. Torex appears to be consolidating junior exploration companies at attractive prices, while other miners remain relatively complacent.

- Canaccord expects M&A activity to continue, driven by consolidation among producers and royalty companies, as well as increased developer mergers to build out development pipelines. The group believes share buybacks make a lot of sense today because of: 1) sector undervaluation, 2) signaling confidence in future business value rather than waiting for generalist investors, 3) improved per-share metrics, 4) tax efficiency, and 5) the opportunity to capitalize on sector volatility.

- For Visla Silver, the high-grade Panuco project continues to show strong potential for resource growth, according to CIBC. Upcoming catalysts include ongoing progress at the fully permitted test mine, permitting updates in Mexico, the release of a feasibility study targeted for the second half of 2025, and the vision of first silver production by mid-2027. CIBC continues to view Panuco as one of the most promising primary silver development projects.

Threats

- According to JP Morgan, Ramelius Resources’ costs were 4% better than forecast in the quarter, but FY25 narrowly missed the low end of guidance. Pre-delivery of 7,000 ounces of hedging caused pricing to come in 4% below forecast. No FY26 guidance was given.

- U.S. platinum premiums fell after President Trump exempted refined copper from immediate tariffs, altering traders’ hedging strategies. The $30 per ounce premium between U.S. futures and London spot prices dropped to nearly zero, Bloomberg reports.

- Alamos maintained production guidance of 580–630k ounces but raised AISC guidance to $1,400–$1,450/ounce from $1,250–$1,300, citing higher share-based compensation, royalties, and slower starts at Magino and Young-Davidson. According to Scotia, Alamos has lagged peers recently and may struggle to outperform without a catalyst.