Gold prices have taken a breather after an impressive run-up earlier this week, pulling back modestly to trade around $3,545 per ounce, down roughly 0.5% from yesterday’s peak of $3,578. The dip reflects short-term profit-taking, but the underlying momentum remains constructive. This week’s rally to new highs underscored the growing strength of the safe-haven trade, with investors responding to a blend of geopolitical uncertainties, shifting monetary policy expectations, and structural changes in global reserve allocations. Against this backdrop, the metal continues to hold its place as a central pillar of stability within the broader investment landscape.

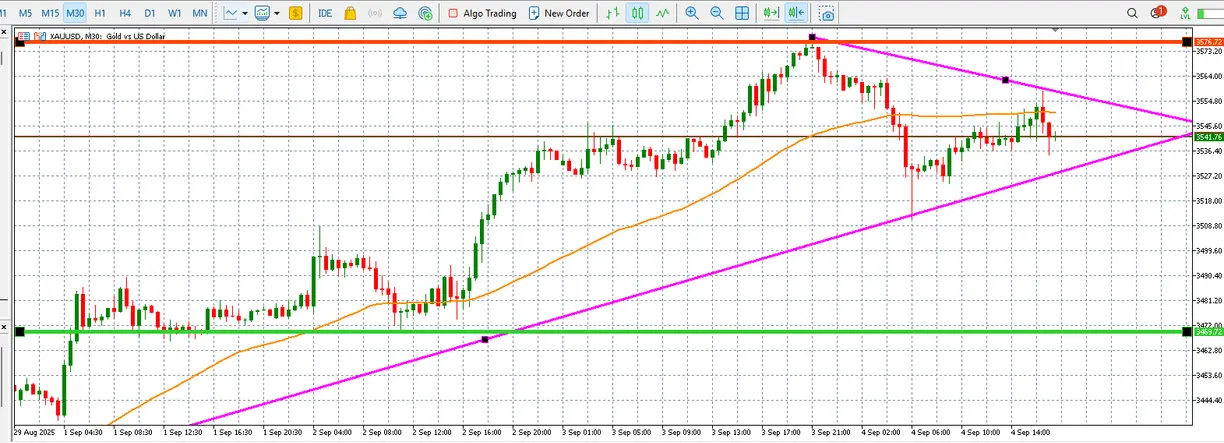

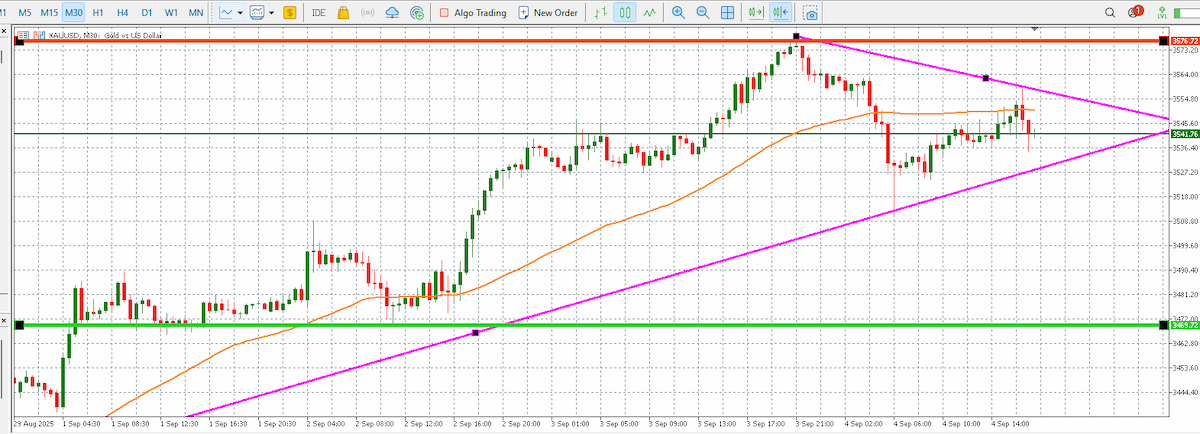

Gold trading chart: XTB

The economic data flow has played an important role in today’s moderation. The latest ADP private payrolls figure came in at just 54,000, undershooting the consensus forecast of 73,000. That disappointment highlights a softening labor market and feeds into speculation that the Federal Reserve may move sooner rather than later to ease policy. This dynamic typically supports gold, as lower rates reduce the opportunity cost of holding the metal while simultaneously signalling caution over the growth outlook. Yet, markets are also eyeing the more consequential Non-Farm Payrolls (NFP) report due shortly. Historically, gold has moved inversely to payroll surprises—a weak print tends to trigger buying, while stronger-than-expected job gains put pressure on the price. The interplay between these releases explains much of the volatility in recent sessions.

Beyond data, intraday sentiment has also been a driver. Around the 2:40 PM window, equities staged a modest uptick, suggesting a “risk-on” tone that weighed on gold temporarily. This dynamic is crucial for analysts to monitor: when equity indices advance, capital often rotates away from safe-haven assets, creating headwinds for gold. Conversely, risk-off episodes where stocks weaken tend to accelerate flows into gold. As such, the short-term pullback we are seeing today fits neatly into this risk-on narrative. It does not negate the underlying bullish structure but instead reflects the constant tug-of-war between short-term positioning and long-term fundamentals.

Those long-term fundamentals remain perhaps the most compelling driver of gold’s trajectory. A quiet but profound shift is taking place in global reserve management. Central banks are steadily reducing their reliance on U.S. Treasuries, redirecting allocations into gold at a scale not witnessed in decades. With holdings now surpassing 36,000 tons and annual purchases running above 1,000 tons, the demand base has grown significantly stronger. This trend is not just a function of diversification—it reflects waning confidence in Treasuries as the ultimate safe-haven asset. The implications are significant: if even 1% of the vast pool of capital traditionally directed toward Treasuries were to move into gold, prices could easily accelerate toward $5,000 per ounce. The psychology of such a shift—particularly if made public—could itself become a self-reinforcing driver of higher valuations.

For investors and analysts, several focal points stand out. First, the NFP report will be decisive in shaping near-term price action. A downside surprise would validate the ADP signal and reinforce gold’s upward trajectory. Second, market risk appetite should be closely tracked; correlations between equity indices and gold are particularly strong during periods of heightened volatility. Third, monitoring the pace of central bank gold accumulation and reserve allocation away from Treasuries remains critical, as this represents a structural rebalancing with long-lasting effects on price.

From a portfolio perspective, gold remains undervalued when viewed through the lens of reserve diversification and real interest rate trends. The market has yet to fully account for the scale of reserve reallocation underway, nor has it priced in the potential for deeper rate cuts should labor market softness persist. As such, we continue to view gold as not only a tactical hedge but also a strategic asset, positioned to benefit from both cyclical pressures and structural capital flows. The pullback witnessed today appears less like a reversal and more like a pause in a broader bullish story