As an investor, it pays to be cautious, to think through various scenarios carefully, to constantly review your own assessments critically — but at the same time not to be a weather vane blowing in the wind, not to let yourself be distracted by media spectacle, and not to be swept into wrong decisions by the ups and downs of the financial markets. This applies especially — perhaps even particularly — to precious metals investors, those who buy gold and silver for wealth preservation and capital appreciation.

As an investor, you certainly know that the only constant in life is change. For instance, companies come and go. They are founded, rise, sometimes fall again, some reinvent themselves, others disappear completely.

Gold is different. It does not change its physical properties over time; it is, so to speak, what it is, and it will remain, what it is.

Moreover, once gold has entered humanity’s possession, it does not disappear again: it is used, but not consumed. Its available quantity gradually increases over time through new mining output.

And the total amount of gold grows only relatively slowly — on average by just under 2% per year since the beginning of the 20th century — by the way, far less than credit and money supplies are expanded in the developed economies.

What usually shows major changes with respect to gold is not so much the supply of gold, but rather the esteem and appreciation that people have for the yellow metal — in other words, gold demand.

The yellow metal is in demand for industrial purposes, jewellery, and investment. All these demand components contribute to total gold demand; and they diversify and stabilise it. For example:

If investment demand for gold rises sharply and the gold price rises accordingly, industrial demand for gold falls: gold is used more sparingly and/or replaced by substitute materials wherever possible, reducing the upward pressure on the price of gold.

Conversely: if the gold price falls because monetary demand for the yellow metal weakens, industrial demand rises at the same time because gold is now cheaper to use in production—and this supports the gold price.

In this sense, there is a certain automatic, built-in stabilisation of gold demand. However, individual demand components can, and do, change sustainably, beyond the short term.

Since the beginning of the 21st century at the latest, it can be assumed that monetary gold demand has (once again) gained significantly in importance in gold price formation:

The growing problems in the international credit and fiat money system are, on balance, driving total demand for the yellow metal higher, translating into a rising gold price. Gold is increasingly in demand as a store of value, especially also as portfolio insurance.

The concerns of investors driving this development are well-founded and manifold: many fear the collapse of the global debt pyramid; or that central banks will monetise debt ever more strongly, thereby driving inflation higher; or that savers and investors face defaults that could destroy their capital.

In such an environment, gold is in demand: after all, the purchasing power of the yellow metal cannot be debased by the central banks’ electronic printing presses; it carries no default risk; and it can be withdrawn from the banking and financial sector — and, last but not least, the marketability of gold does not, proverbially, depend on electricity.

At present, there is (unfortunately) no sign that the rulers and the ruled in the Western world want to halt and reverse the pernicious trend fed by the credit and fiat money system. On the contrary, they are sticking to excessive debt, instructing central banks to lower interest rates, keep them artificially suppressed, and continue expanding credit and fiat money supplies ever further.

Yet the hope that the economies might somehow “grow out” of their problems in this way is rather slim. The probability that the world’s economic and financial system will be pushed wide-eyed into a big crisis — and that such a crisis will be met with even more debt, even lower interest rates, and even more money creation — is, by contrast, quite high.

The question therefore arises: what further consequences will all this have for the gold price? This question can perhaps be answered more easily if we decompose the gold price. In this sense, gold’s market price, that is the nominal gold price, equals real gold price plus a price inflation premium plus a credit default, or risk, premium.

The real gold price represents the relative price of gold vis-à-vis all other financial instruments (stocks, bonds, etc.) and other goods such as real estate;

the price inflation premium reflects the (expected) loss of purchasing power of fiat money;

the risk premium is the surcharge that market participants are willing to pay for gold to protect themselves against payment defaults.

Such a decomposition may help us better understand the dynamics of the gold price. For example, let us think about the following situations:

If goods price inflation moves within “generally accepted bounds” of, say, an average of 2–4% per year, the nominal gold price also rises in this order of magnitude (due to the price inflation premium) without the real gold price or the credit risk premium changing.

If inflation rises above the level accepted by the population, say to 4–8% per year, not only does gold’s price inflation premium rise accordingly, the real gold price also goes up — because holding gold now becomes more attractive relative to other asset positions (especially bank deposits and debt securities).

And if market participants fear defaults that the central bank will not be able, or willing, to avert by printing new money, both the real gold price and the default risk premium in the gold price rise.

Against this backdrop, it appears that since the beginning of the 21st century the price of the yellow metal (which stood at around 257 U.S. dollar per ounce at the time) has probably risen (to now 4,200 U.S. dollar per ounce) because both the real gold price and the price inflation premium have increased.

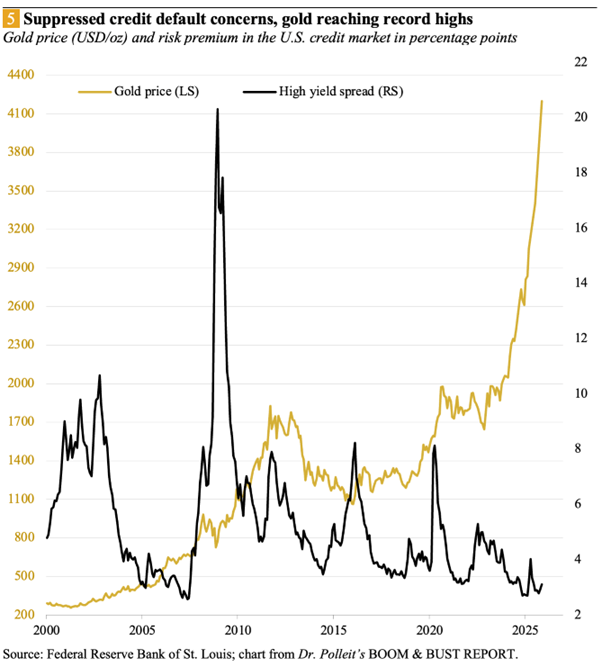

Credit default concerns in the markets have certainly also played an important role in the rise of the gold price. However — and this is important to understand — credit default fears have been receding since the great crisis of 2008/2009 was overcome, and the risk premium in the gold price has therefore probably been relatively subdued or even declining.

With the politically dictated lockdowns in 2020/2021, the real gold price and the price inflation premium then rose strongly, more than compensating for the still subdued (or even declining) risk premium.

Especially the explosive rise in the gold price in the last two years (during which it has almost doubled when measured in U.S. dollar) is attributable to a higher real gold price and an elevated price inflation premium.

The important, indeed decisive question, however, remains: Has the gold price rise already gone too far, is gold now too expensive? Or is it still too low, or is it just right?

There are good reasons to assume that the gold bull market of the 21st century has probably only just begun — that it is far from over. The major problems that are still to come have very likely not yet appeared at all, or only inadequately, on most market participants’ radar screens. Over the next twelve months, therefore, the chances are quite good that (cautiously estimated) the price of one troy ounce of gold will reach at least the 5,000 mark in U.S. dollar — that would be a return potential of roughly 20 per cent, starting from the current price of around 4,20 U.S. dollar per ounce.

From a risk and reward perspective, it makes sense for the long-term oriented investor to allocate a portion of his investment assets to gold— since the chances are good that the 21st-century gold bull market has essentially only just begun.

And if you want to know how to position yourself sensibly as an investor and what you should specifically do, I recommend you read Dr. Polleit’s BOOM & BUST REPORT. You’ll find all the information at www.boombustreport.com/english.