Gold prices rose on Monday, driven by growing expectations of a U.S. interest rate cut that pressured the dollar, ahead of a Federal Reserve policy meeting this week. Spot XAU/USD climbed 0.4% to $4,188.51 per ounce as of December 8, 2025, rebounding from last week's muted performance that saw the metal close flat at around $4,175 amid holiday-thinned volumes and profit-taking.

This uptick isn't mere technical bounce—it's a recalibration fueled by last week's labor market fissures and inflation softness, which have solidified market conviction for Federal Reserve easing.

With DXY slipping below 103 (down 0.5% last week), gold's -0.87 correlation shines through, but traders must zoom in on the nuances: wage revisions hinting at sticky reflation, and QT taper liquidity that could unlock $60 billion. This week's calendar, headlined by the Fed, JOLTS, and CPI, could catapult XAU/USD to $4,300 or expose it to $4,000 tests.

Let's dissect last week's drivers and the forward-looking traps.

A Narrow Trade Driven by Dovish Signals and Profit-Taking

Last week's gold action was a tale of two realities: headline resilience masking deepening policy-easing imperatives. The metal traded in a narrow $4,150–$4,220 band, ending the period with a negligible 0.1% gain after an initial pop on Thursday's dovish FOMC minutes.

Those minutes, released December 4, revealed a 7-2 vote for November's 25 bps cut but flagged "upside risks to inflation" from potential tariffs, tempering the rally and capping gains near the 50-day EMA at $4,210.

Profit-taking ensued Friday as spot prices dipped to $4,199 before recovering on light positioning ahead of PCE revisions—ultimately showing core PCE easing to 2.8% YoY from 2.9%, a whisper of abating services inflation that boosted cut odds to 87% for December. Yet, beyond the top-line "easing intact," the minutes' subtext—four FOMC members dissenting on pace, citing labor hoarding—underscored a Fed divided on 2026's trajectory (median two cuts projected).

This internal friction, coupled with Challenger's 71,321 announced layoffs (up 15% MoM), amplified stagflation whispers: U.S. Q3 GDP held at 1.8%, but nowcast revisions implied a 0.2-point drag from inventory builds amid tariff fog.

Labor Market Fault Lines Intensify Safe-Haven Demand

Compounding this, ADP's surprise 32,000 private payroll drop on Wednesday (versus +150K expected) and the preliminary Michigan sentiment's expectations index slipping to 82 (below recession's 80 threshold) ignited safe-haven bids, lifting gold $25/oz intraday. These weren't isolated shocks; they highlighted labor's underbelly—JOLTS revisions due this week show vacancies at 8.2 million (up 200K from initial), signaling hoarding that keeps wage pressures at 4.1% (above Fed's 3.8% comfort).

Gold, as the anti-dollar play, benefited asymmetrically: each 10K vacancy surprise above consensus has added ~$20/oz via eroded real yields (-0.8% on TIPS).

Geopolitics simmered in the background, with Red Sea disruptions hiking shipping costs $80/container, but U.S.-China truce rumors capped the haven premium. ETF flows reflected the caution: $1.2 billion inflows for the week (net 28 tonnes added), but physical demand in India/China eased 34% as buyers awaited corrections.

A Pivotal Fed Week Shapes Risk and Reward

This week's economic calendar—dominated by the December 10–11 FOMC two-day meeting—serves as gold's ultimate litmus test, with non-headline signals poised to dictate $100/oz swings. Wednesday's core event: the Fed's rate decision (88% priced for 25 bps to 3.75–4.00%), but fixate on the dot plot and SEP revisions. September's median eyed two 2026 cuts; watch for a hawkish skew if three+ hawks (e.g., Bowman) dissent, potentially revising unemployment to 4.5% (from 4.2%) while holding GDP at 1.8%—a steeper yield curve scenario that could rebound DXY above 104 and pressure gold to $4,050.

Market Triggers to Watch and Tactical Levels

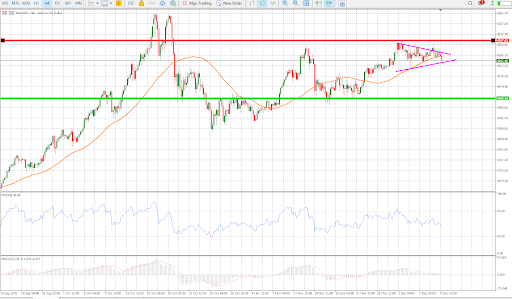

Technically, last week's RSI reset to 55 neutralized overbought froth. The price has dropped below the 50-day SMA on the four time frame which shows that the bulls are running out of steam. The MACD is also showing signs of losing some momentum.

Gold trading: MH Markets UAE

Conclusion: A Market Poised for Breakout or Correction

In sum, last week's labor/inflation soft spots and this week's Fed/JOLTS gauntlet frame gold's December denouement: a $4,000+ bastion amid policy penumbras and economic schisms. With 710 tonnes/quarter CB demand and Red Sea frictions, $4,300 beckons—but tariff shadows and wage persistence could enforce $4,050 pauses. Gold doesn't surf headlines; it mines the margins. Allocate 5–10%, layer wisely—the Fed's dots will draw the line.