(Kitco News) – The minutes from the January 27-28 Federal Open Market Committee (FOMC) meeting showed members expecting tariff-driven inflation to ease as the year rolled on, but with a large degree of uncertainty about the timing, and with the labor market appearing to stabilize after cooling, several members supported a two-sided statement of monetary policy risk, while two dissented on the rate hold, preferring a quarter-point cut.

In the staff summary of economic conditions, FOMC members were told that the information available at the time “indicated that real GDP continued to expand in 2025, at a rate slightly below its 2024 pace,” while labor market conditions “showed signs of stabilizing following a period of gradual cooling,” and consumer price inflation “remained somewhat elevated.”

“Recent indicators suggested that foreign economic activity expanded at a below-trend pace in the second half of last year,” the minutes noted. “U.S. tariffs continued to weigh on foreign manufacturing activity, notably for Canada and Mexico in autos, aluminum, steel, and related industries. By contrast, in some emerging Asian economies, exports of high-tech products surged amid robust demand from the artificial intelligence (AI) boom. In China, activity was boosted by strong exports to markets other than the U.S.”

Turning to financial conditions, the Fed staff noted that “[t]he market-implied expected path of the federal funds rate, nominal Treasury yields, and swap-based measures of inflation compensation were little changed, on net, over the intermeeting period. Broad equity price indexes rose modestly, on net, while credit spreads remained low by historical standards. The one-month option-implied volatility on the S&P 500 index ended the period roughly unchanged at a moderate level by historical standards.”

The staff’s economic forecasts prepared for the January meeting were stronger than those of the December meeting, “reflecting incoming data, greater expected support from financial conditions, and a small upward revision to the projected path of potential output.”

“Real GDP growth was expected to outpace potential growth through 2028 as the drag from higher tariffs waned and as fiscal policy and financial market conditions continued to support spending,” they noted. “As a result, the unemployment rate was expected to decline gradually starting this year, moving below the staff's estimate of its natural rate by the end of the year and remaining below the natural rate through 2028.”

However, the inflation forecast was slightly higher than December,” reflecting the expectation that resource utilization would be tighter and the path of core import prices would be higher than previously projected.” \

“With the effect of higher tariffs on inflation expected to wane starting around the middle of this year, inflation was projected to return to its previous disinflationary trend,” they added.”

“In an environment of high economic uncertainty, risks around the forecasts for employment and real GDP growth continued to be seen as skewed to the downside,” the minutes read. “Risks to the inflation projection continued to be viewed as skewed to the upside: With inflation having remained above 2 percent since early 2021, a salient risk was that inflation would prove to be more persistent than the staff anticipated.”

The minutes then moved to the discussions among FOMC members about current and future economic conditions.

“Participants observed that overall inflation had eased significantly from its highs in 2022 but remained somewhat elevated relative to the Committee's 2 percent longer-run goal,” the minutes stated. “Participants generally noted that these elevated readings largely reflected inflation in core goods, which appeared to have been boosted by the effects of tariff increases. In contrast to prices for core goods, some participants commented that disinflation appeared to be continuing for core services, particularly for housing services.”

On the inflation outlook, “participants anticipated that inflation would move down toward the Committee's 2 percent objective, though the pace and timing of this decline remained uncertain.”

Regarding the labor market, “participants observed that the unemployment rate had held steady, on net, in recent months, while job gains had remained low. Most participants noted that recent data readings such as those for the unemployment rate, layoffs, and job openings suggested that labor market conditions may be stabilizing after a period of gradual cooling.”

Turning to the outlook for monetary policy, the minutes noted that “several participants commented that further downward adjustments to the target range for the federal funds rate would likely be appropriate if inflation were to decline in line with their expectations, while others “commented that it would likely be appropriate to hold the policy rate steady for some time as the Committee carefully assesses incoming data, and a number of these participants judged that additional policy easing may not be warranted until there was clear indication that the progress of disinflation was firmly back on track.”

“Several participants indicated that they would have supported a two-sided description of the Committee's future interest rate decisions, reflecting the possibility that upward adjustments to the target range for the federal funds rate could be appropriate if inflation remains at above-target levels,” the minutes read. “All participants agreed that monetary policy was not on a preset course and would be informed by a wide range of incoming data, the evolving economic outlook, and the balance of risks”

Voting for the rate hold were Chair Powell along with Williams, Barr, Bowman, Cook, Hammack, Jefferson, Kashkari, Logan, and Paulson. Voting against were Stephen Miran and Christopher Waller, both of whom “preferred to lower the target range for the federal funds rate by 1/4 percentage point at this meeting.”

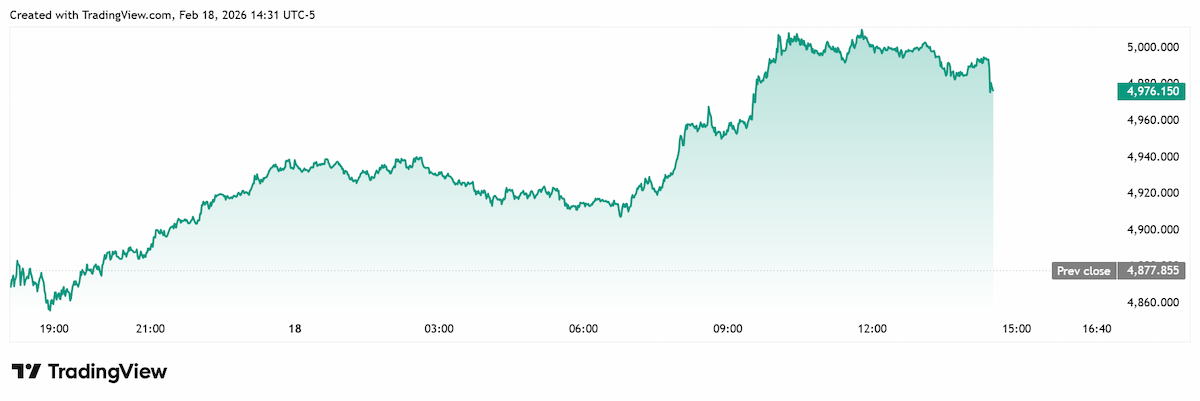

Gold prices continued to trade near session highs following the 2 pm Eastern release. Spot gold last traded at $4,976.42 for a gain of 2.02% on the session.

Jeffrey Roach, Chief Economist for LPL Financial, told Kitco News that he found some of the Fed's projections overly optimistic.

"The combination of above‑potential growth with easing inflation is not common in Fed projections and likely reflects a strong assumed boost from productivity and AI‑related investment," he said. "The Fed almost never forecasts multi‑year above‑trend growth."

Roach said one of the more interesting observations he gleaned from the minutes is the Fed's apparent belief that financial‑stability risks are building under the surface.

"Asset valuations are high, credit spreads are tight, and AI‑related investment has created new pockets of risk, especially in private credit, leveraged firms, and highly concentrated tech names," he said. "They specifically called out the hedge funds. Hedge‑fund leverage and Treasury‑market vulnerabilities remain key concerns."

"Looking ahead, we should monitor potential spillovers from volatile global bond markets and FX," Roach said. "Personally, the anticipation is building for the updated Summary of Economic Projections released at the March 18 meeting. I expect the next cut in Fed funds won’t be until June."