(Kitco News) - Gold gave back its late-2023 gains in January despite strong seasonal factors, but Red Sea tensions, election uncertainty, and eventual rate cuts will support gold prices this year, according to the World Gold Council.

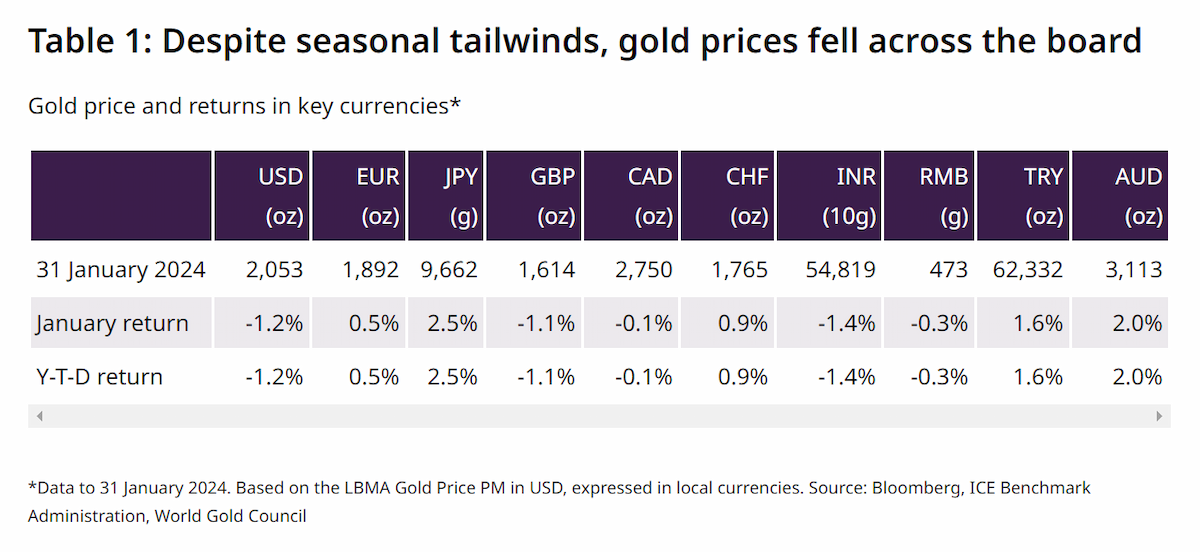

“Gold prices fell back to US$2,053/oz, to finish the month 1% lower, and departing from historical seasonal strength,” the WGC noted in their latest monthly market report.

“A retracement following such a stellar finish to the year was probably on the cards, with global gold ETF outflows accelerating to 51t and a reduction in COMEX futures net longs (-206t) the main contributors, as per Gold Return Attribution Model,” they said.

“Added to this was the headwind of higher Treasury yields and the US dollar as US economic strength sharply surprised to the upside, and hopes of early monetary policy cuts were dashed,” they noted.

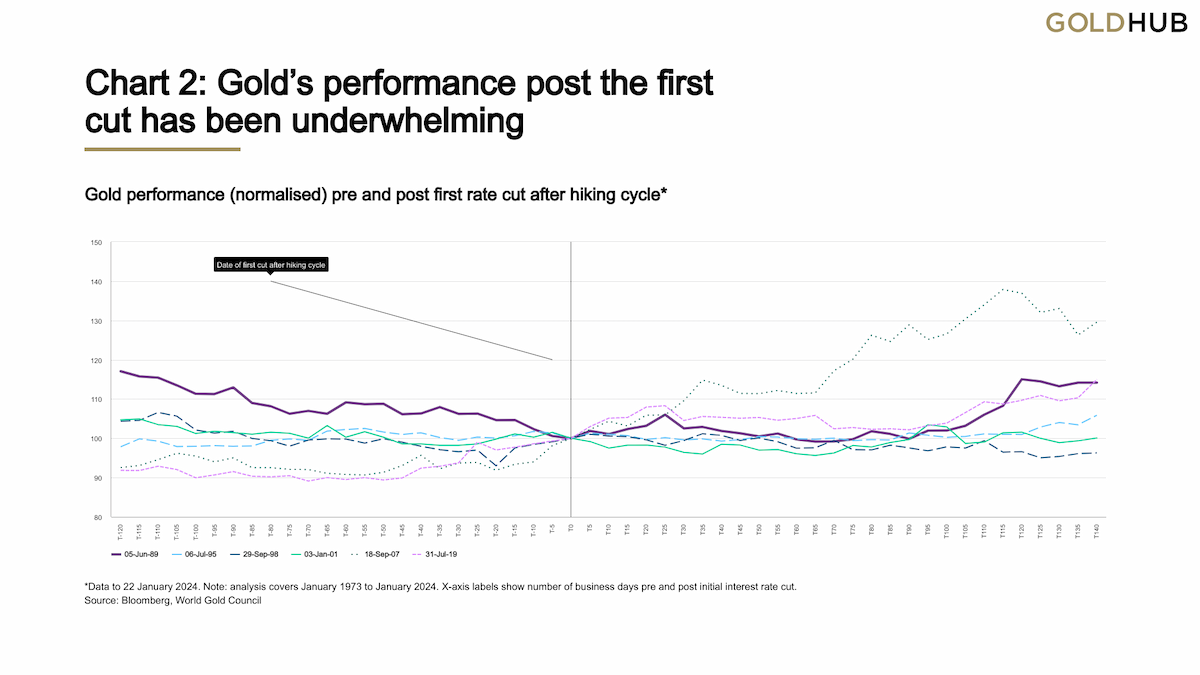

Looking ahead, WGC analysts noted that while the Federal Reserve’s interest rate reductions have historically provided a boost to gold prices, the initial rate cut is not always a major catalyst.

“Falling rates […] are on average good for gold, but the first Fed cut after a hiking cycle has been a bit of a damp squib in the past, producing near-term rallies only if and when a material economic or equity correction has ensued, pushing longer maturity yields lower,” they wrote.

“This makes sense if the cut is highly anticipated, or if it is bathed in soft-landing rhetoric,” the WGC noted. “After all, recessions historically didn't become evident until some time after that first cut, if they materialised at all.”

The analysts said the U.S. economy’s journey back to target inflation and a potential soft landing “was always likely to be bumpy and narrow,” and they noted a number of “concerning developments that could shake up the ‘immaculate disinflation’ the US has experienced over the past few months,” which would in turn push back the date of the Fed’s highly-anticipated pivot.

The first of these is the emergence of relatively easy conditions in financial markets. “Financial conditions, a leading indicator of real GDP, has gone from bottom 10% to top 90% of readings in six months,” the WGC said. “This suggests economic conditions are likely to remain at ease at least in the short term,” and were GDP to pick up, “inflation may have a tough time falling.”

The second factor is stubbornly high labor costs. “Rebalancing in the labour market has occurred in job openings and quit rates, not unemployment,” they noted. “The employment cost index tends to go where the National Federation of Independent Business’s small business compensation plans go. At the moment that is up, and up close to where the Fed last squirmed hawkishly.”

Rental rates are the third factor which could give the Fed pause. “Rents are not forecast to fall much in 2024 and are likely to contribute 17-20bps to core inflation in January and February,” the analysts said. “That leaves almost no room for other contributions before core inflation exceeds the Fed’s target.”

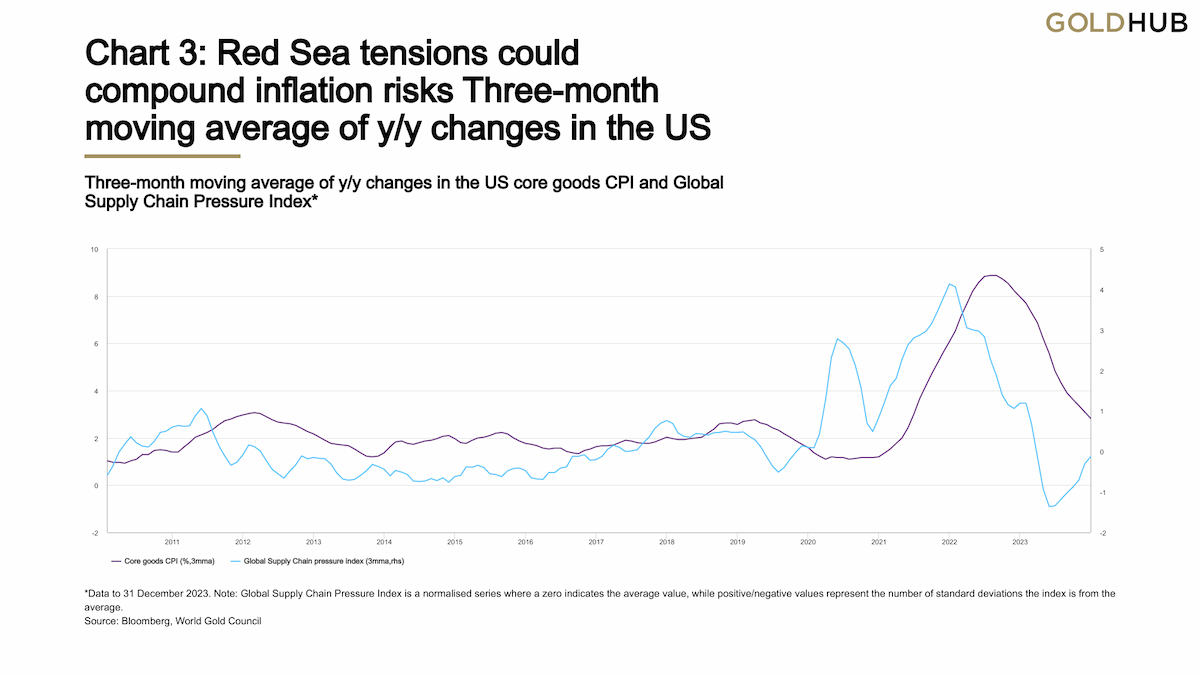

The final development which could keep rates higher for longer is the conflict in the Middle East. “Red Sea tensions have started to impact freight costs, which could lead to more general supply-chain pressures that were a major cause of the inflation surge in 2022, particularly in Europe,” they said.

“[A]t this juncture, US core Personal Consumption Expenditures (PCE) on a 3- and 6-month annualised basis look right on cue for cuts,” they said, but added that based on these factors, “the inflation genie may not be firmly back in the bottle.”

The Council cautioned that yields could climb back up if inflation growth and employment data remain elevated, “which, all else equal, could be a headwind for gold.”

“However, higher bond yields would likely also pressure equities, which once again look particularly frothy and could result in stock market volatility,” they said. “Added to this, a steady stream of elections are coming thick and fast, bringing with them lots of known unknowns about geopolitical stability. There are more to follow in March as well, and of course there are the US primaries.”

“The general level of uncertainty is poised to keep some investors with one hand on their gold,” they concluded.