As the cost of living continues to rise due to ‘sticky’ inflation and non-stop money printing by central banks, the pocketbooks of Americans are becoming increasingly stretched, leading to mounting frustration.

“Frustration over fees in particular – having to pay middlemen in order to move and use their own hard-earned money – is the top driver of discontent with the entire [U.S. financial system],” said Coinbase analysts in their most recent State of Crypto report.

“In 2022, Americans could have saved, at minimum, about $74 billion in credit card transaction fees alone, amounting to an average of $600 per household, and merchants spent more than $126 billion on fees to process credit card transactions,” they noted. “By using blockchain technology instead, they could have paid next to nothing.”

These truths are leading to a new appreciation for crypto and blockchain for many investors, as a recent poll found “that at least three in five Americans want updates to the current system that make it cheaper, faster, and easier to access, and the top reasons why they see potential in crypto are in line: its ease of use, affordability, and streamlined, fully digital, legacy-free nature,” the report said.

The analysts also noted that familiarity with the internet has led many younger consumers to “expect to be able to transact at the speed of the internet, globally, any time of day or night, without overcoming hurdles to participate or waiting on business hours or cross-border delays.”

Because of this, “Americans aged 18-40 are much more likely to own crypto than older Americans, and by wide margins, they’re more likely to believe crypto can make the system cheaper, faster, and fairer,” they said. “But in an era of little bipartisan agreement on any issue, self-identified Democrats and Republicans agree within four percentage points that crypto and blockchain could make the financial system cheaper, faster, and easier to access. The future of money is here.”

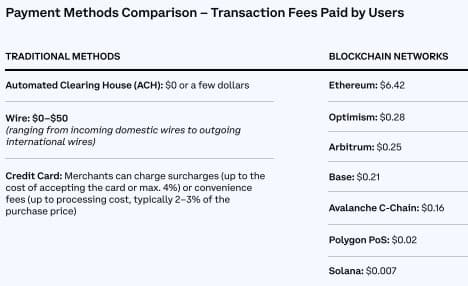

“Payments over blockchain networks can be up to 5,000x cheaper than payments through traditional methods like wires, especially for international money transfers when accounting for the best case scenario of fees less than $0.01,” the report said. “Underbanked and unbanked Americans cite high fees as the top reason why they don’t have bank or credit union accounts.”

And with the global remittance market projected to increase to $50 billion by 2024, “Sending money home to loved ones via blockchain instead of the legacy system for one year could save the sender nearly an additional month’s worth of remittance,” they said. “On average, migrant workers around the world send up to $300 to loved ones every month. Across the course of a year, they could pay nearly another month’s worth – $252 – in currency conversion fees.”

With blockchain networks capable of sending remittances for $0.01 per transaction, a year’s worth of fees would only amount to $0.12, a significant reduction from the current system.

“In the US alone, 15% of Americans have sent a remittance in the previous 12 months,” the analysts said. “Whether they use banks, with fees averaging 10.8%, or money transfer options, with fees averaging 6.2%, or the post offices, charging 5.5%, the impact is immense. The average fee rate of 6.18% means Americans on average spend close to $12 billion on remittance fees per year.”

For merchants, credit card processing fees are the second highest operating expense after labor, they noted, with the average credit card processing fee ranging from 1.5% to 3.5%. “A $1,000 transaction incurring a credit card charge of 1.5% to 3.5% results in fees for merchants ranging from $15 to $35, while a payment on a blockchain network with an average fee of one cent amounts to just $0.01,” they said.

The benefit is even more stark when large transactions are considered, as a $10,000 payment would incur fees ranging from $150 to $350, “while the blockchain transaction continues to cost $0.01.”

“Moving at the speed of the internet, from peer to peer without legacy intermediaries that keep bank hours and otherwise slow things down, crypto enables fast payments, including cross-border payments and remittances; faster payroll to help boost consumer liquidity; and quick execution of smart contracts,” the report said.

The analysts noted that blockchain networks are capable of processing payments “at least 24x and as much as 432,000x faster than traditional methods.”

Citing Bitcoin, which takes one hour to reach full consensus on a transaction, they said “Traditional markets at their fastest complete payments in 24 hours, lagging blockchain by a factor of 24 at best.”

“The fastest blockchain networks, with transaction times under one second, outpace the slowest traditional methods, which take five days, by 432,000x,” they said. “Crypto remittance is 388x faster than traditional methods.”

The ability to speed up the payroll process is another major benefit, they noted. “Payroll processing via blockchain, versus total processing time for traditional payroll, is near-instant versus an average between one and six business days.”

“Benefits of same-day payroll include strengthening loyalty to employers, helping employees take advantage of investments that can earn them interest, and token streaming to access a growing array of DeFi services,” the report said. “79% of employees want same-day wages, and nearly seven in ten would be likely to stay longer with an employer and pick up extra shifts.”

Cryptocurrencies can also simplify the process of accessing a variety of financial services, the report noted. “Requiring only internet access, crypto offers much more accessible, timely access to financial services than the legacy system, including for groups of people and parts of the world that haven’t had much access to the system at all, or whose home currencies might be unstable.”

While setting up a traditional bank account requires paperwork and costs that create high barriers to entry, “Setting up a crypto wallet simply requires creating a private key and possibly completing two-factor authentication, both at no charge,” the analyst said.

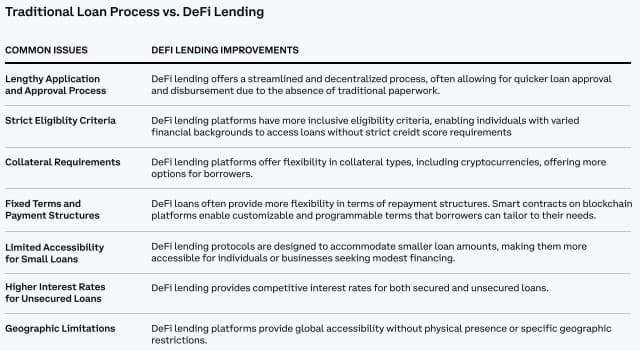

The benefits are even more pronounced when it comes to securing a loan.

“Benchmarked at 60 minutes, DeFi loan approval and processing is about 48x to 144x faster than traditional avenues for loan approval and processing, which can take two to six days,” they said. “More importantly, DeFi loans are more accessible for more people, giving those less served or unserved by the legacy financial system a means to take out loans that can help build a business or buy a home, i.e., build wealth.”

“In countries with unstable governments and currencies, stablecoins like USDC are a neutral, decentralized way for citizens to safeguard their savings and transact across borders,” the analyst concluded. “Since December 2020, the number of active addresses that have transferred stablecoins has increased more than 10x, and the number of active transfers has increased more than 8x.”