(Kitco News) – The hidden driver of the white-hot 2024 gold market may be a short-term rebalancing in equity sentiment, according to private Swiss bank Lombard Odier.

The recent report by Florian Ielpo, Head of Macro and Multi Asset and Didier Rabattu, CIO, of Sustainability Equities, attempted to control for a number of known factors to determine what else might be driving gold prices higher.

The authors note that the precious metal’s dramatic price surge “is particularly striking given that gold did little to protect investors from the effects of accelerating inflation over the past two years. So why rally now?”

They suspect that the rally is being fed by a “complex interplay of known and potentially unknown factors” including traditional fundamental drivers like inflation, real rates and risk aversion, the more recent phenomenon of large central bank purchases, and a “sense of bearishness arising from expensive equity markets.”

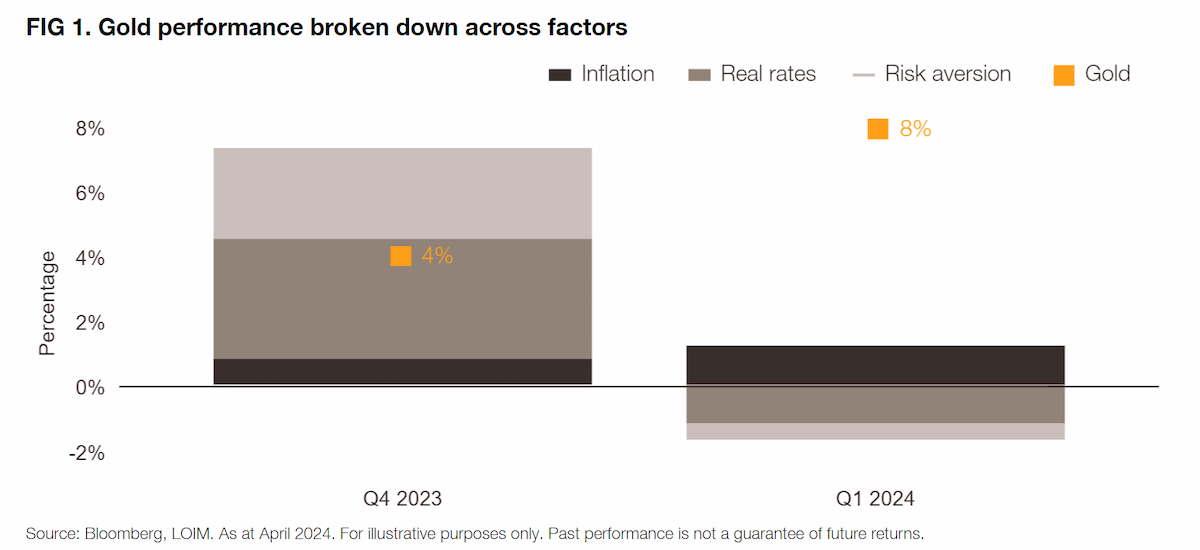

To assess how the known fundamental factors of inflation, real rates and risk aversion have evolved, Lombard Odier estimated their contributions to gold’s performance during Q4 2023 and Q1 2024.

“Figure 1 visually represents these dynamics,” they wrote. “Over the fourth quarter of last year, gold prices actually fell short of what fundamental factors predicted, mainly because of declining real yields and the pervasive effects of October’s market volatility. Gold was expected to gain about 7% but only rose around 4%.”

The analysts noted that the opposite was observed in the first quarter of this year. “[W]hile fundamentals predicted that gold’s performance should have been near zero, it actually gained about 8%,” they said. “This suggests a potential ‘catch-up’ effect, with the gold price adjusting to previous fundamentals. However, the concurrent rise in real yields has puzzled market observers, hinting at other influences.”

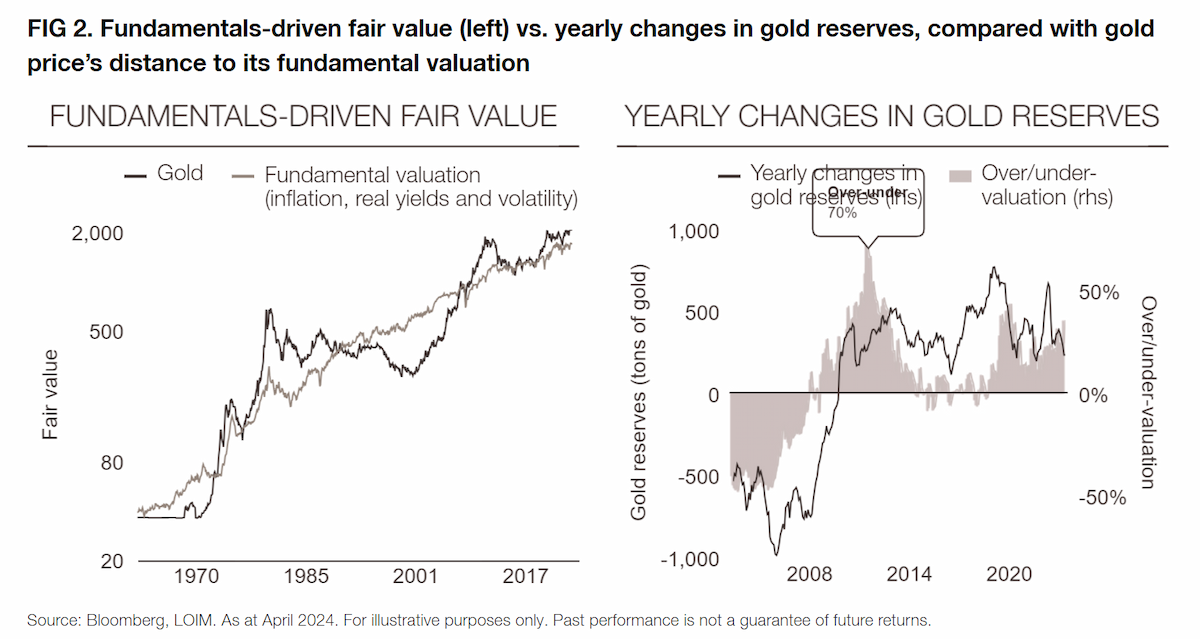

They pointed out that identifying the missing factors is very challenging, but comparing the price a fundamental model suggests for gold with its actual market price “can offer insights into what fundamental aspect might be overlooked.”

The authors demonstrate this approach in Figure 2. “The left side displays the outcome of our fundamental model, which currently values gold at approximately USD 1,700 per ounce,” they wrote. “On the right, the chart traces the evolution of this discrepancy since 2003, juxtaposed against the evolution of central bank gold reserves, as an additional explanatory factor.”

They acknowledged that this analysis “clearly identifies central bank gold reserves as a potential missing link” in their previous assessment of fundamental factors.

“This correlation was particularly noticeable from 2003 to 2008, a period characterised by low gold purchases, and then from 2009 onwards when central banks significantly increased their gold acquisitions, averaging about 400 tons per year,” they said. “However, while this factor has been influential, it alone cannot account for the recent dynamics of gold prices.”

“Other elements may then be impacting gold's valuation, necessitating a broader investigation.”

The authors wrote that the inability of central bank gold purchases to fully account for the dramatic increase in the precious metal's price has led some to believe that despite the strong performance of equities this year, there may be growing unease about them. “This hypothesis is underscored by the notable increase in gold prices during the first two weeks of April, potentially signaling a defensive shift among investors,” they said. “Indeed, as credit spreads widened and implied volatilities increased during this period, gold prices ascended, suggesting that market sentiment may be partly driving this rally.”

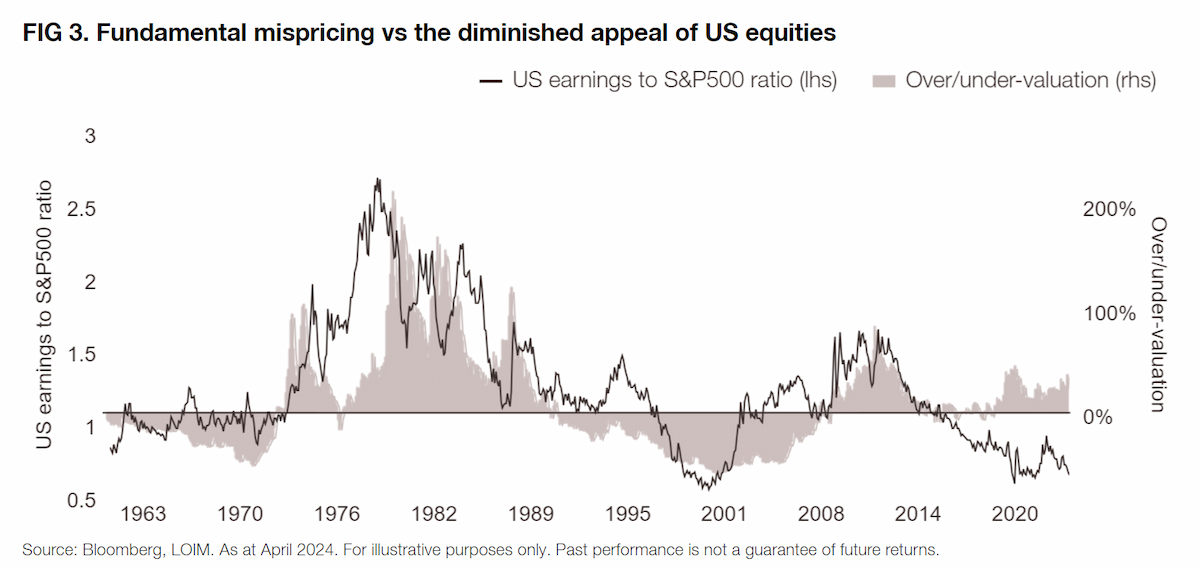

Their analysis of gold’s unaccounted-for rise led them to another potential explanation. “Figure 3 compares the distance between gold prices and their fair value to a gauge of US stock market attractiveness that uses the ratio of US corporate earnings (as per the GDP report) to the price of the S&P 500,” they wrote. “When earnings growth outpaces stock prices, this ratio widens, indicating that the appeal of stocks has diminished. Historically, this metric has accounted for a significant portion of the discrepancies between gold prices and the metal’s fundamental factors. So, while stocks are near all-time highs, the gold market might be reflecting a temporary aversion to stocks among the broader investment community.”

“This sentiment aligns neatly with the current pause in the equity-market rally,” they concluded. “It also could be a critical piece of the puzzle in understanding the recent movements in gold prices.”