(Kitco News) - The gold market continues to establish itself as a global financial asset as traditional pillars of strength weaken due to higher prices, according to the latest research from the World Gold Council (WGC).

On Tuesday, the WGC released Global Demand Trends for the second quarter. In an interview with Kitco News, Joseph Cavatoni, the Market Strategist for North America at the WGC, said there is a distinct shift in the demand profile emerging in the gold market, with Western investment demand starting to pick up as jewelry demand falters.

“We are seeing a shift from jewelry, pure consumption, maybe a form of savings, to pure savings in bars and coins. Now we have to see if one can compensate for the difference,” he said.

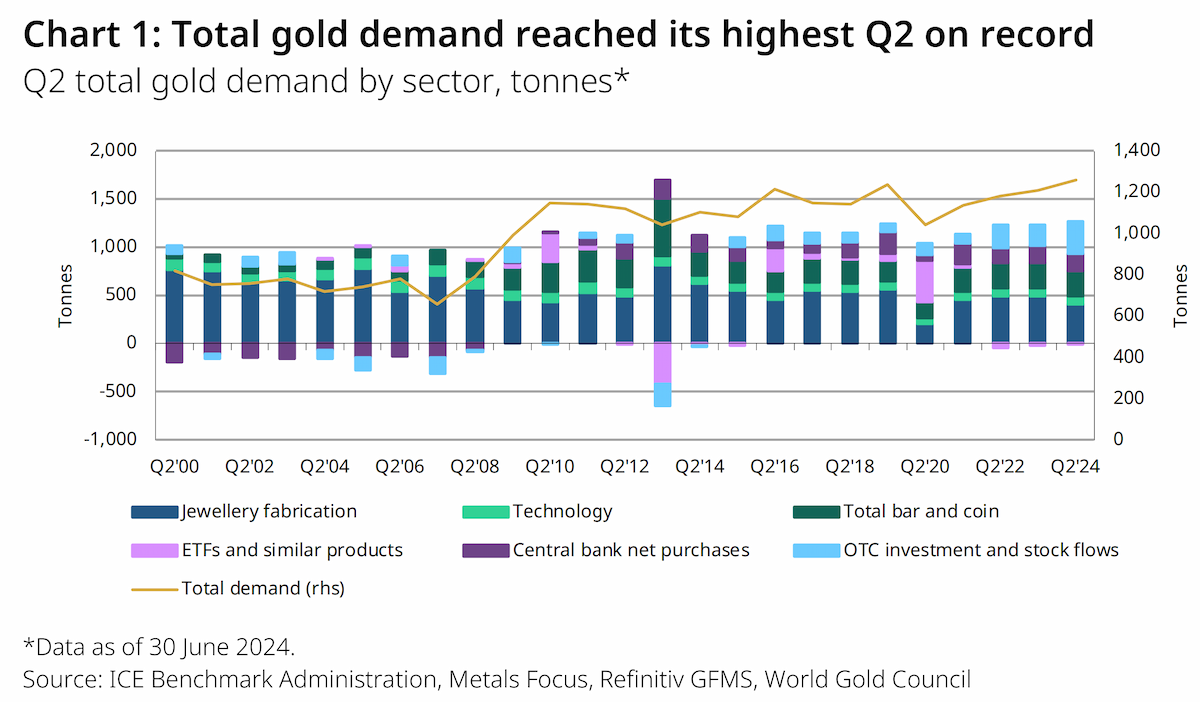

The WGC reported that record-high gold prices in the second quarter had a significant impact on global jewelry demand, which dropped 19% from the second quarter of 2023. Gold jewelry consumption fell to 391 tonnes between April and June, its lowest level in four years.

Total global demand also presents a conflicted outlook. Physical demand, excluding over-the-counter markets (OTC), fell to 929 tonnes last quarter, a 6% decline from last year. However, when including OTC markets, gold demand increased by 4% year-over-year to 1,258 tonnes – the highest Q2 in the WGC’s data series, dating back to 2000.

“OTC investment of 329t was a significant component of Q2 total gold demand. Together with continued central bank buying, it helped drive the price to a series of record highs during the quarter,” the analysts said in the report.

“The second-quarter report does an amazing job of highlighting something we often discuss: gold is global and has different use cases, and you need to understand all of them when you're trying to understand the forward trajectory of the price,” Cavatoni said in the interview.

Although investment demand hasn’t played a significant role in the market as the price action has been driven by demand among Eastern consumers, investors, and central banks, Cavatoni noted that the trend is starting to shift as investors prepare for the Federal Reserve’s easing cycle.

He pointed out that the shift in the marketplace can be seen in the second-quarter data. The WGC noted that the pace of outflows from gold-backed exchange-traded funds slowed sharply in the second quarter. Global holdings declined by just 7 tonnes during the quarter, with inflows in May and June offsetting April’s losses.

Cavatoni explained that European gold ETF demand has led the market in recent months as investors looked to hedge against geopolitical uncertainty and lower interest rates as the European Central Bank began cutting rates before the Federal Reserve.

Cavatoni added that Europe could be a strong test case for the North American market as the Federal Reserve is expected to cut interest rates in September. He also mentioned that the U.S. Presidential Election would create some volatility in the marketplace.

“It’s all playing out that Western investors are gearing up to increase their allocation to gold,” he said.

Looking at physical demand, the WGC reported that bar and coin demand fell 5% in the second quarter to 261 tonnes, as investors capitalized on higher prices.

“Similar to last quarter, Western investors have continued to show strong interest in gold bars and coins, but this has been countered by equal – if not greater – selling interest as the price reached record levels, resulting in far lower net levels of demand,” the analysts said in the report.

However, the OTC market remains robust. The OTC market differs from the physical market as larger bars are bought and sold in direct exchanges. While the market can be fairly opaque, Cavatoni said there are still ways to measure OTC demand.

“The positioning of speculative investors in the US futures market can be indicative of it: net long positions held by money managers increased again in Q2, reaching levels not seen since April 2020 at 575t. The trend of gold demand among high-net-worth individuals across global markets was reportedly a continued contributor to OTC investment in Q2,” the analysts said in the report. “Demand from this sector has been in response to concern over the U.S. debt burden, geopolitical risks, and attraction to the strong price rise.”

Central banks are still net buyers, but demand has slowed

Central bank gold demand continues to attract a lot of attention in the marketplace; however, the attention is not nearly as positive as it was at the start of the year. In the first quarter, the WGC noted that central bank purchases were the strongest on record.

Fast forward to the second quarter, and central banks increased their official reserves by 183 tonnes between April and June. Central bank demand was 6% higher than in the second quarter of last year but down 39% from the first quarter.

The drop came as the People’s Bank of China halted its gold purchases in May and June, ending an 18-month shopping spree.

Cavatoni described the recent headlines about China’s gold reserves “as a lot of noise in the marketplace.”

“You have to look at the broader landscape because Poland is still active, and other central banks are still active; India is still buying,” he said. “There's still a strong case for central banks to buy gold.”

While central banks continue to buy gold, the WGC said that it is too early to determine if the purchases will match or exceed the volume of the previous two years.

Tech sector becomes a robust source of demand for gold

While the traditional pillars of support for gold continue to wax and wane with the tide, the tech sector is proving to be an interesting source of demand.

The WGC said that gold used in industrial applications rose to 81 tonnes in the second quarter, an 11% increase from last year. This is the third successive quarter where tech demand has seen double-digit growth.

“The continued recovery of demand in the technology sector in Q2 was primarily due to high-end chips used in growing application areas such as AI and high-performance computing,” the WGC said.

Gold supply remains relatively steady

Although some support pillars in the gold market weakened in the second quarter, overall demand continues to outweigh supply.

The report said that the total gold supply grew to 1,258 tonnes, an increase of 4% from last year. At the same time, mine production hit a record for a second quarter at 929 tonnes.

“Combined with Q1 production of 859t – also a record for the time of year – this generated record H1 mine production of 1,788t – 2% more than the previous high set in H1 2023,” the WGC said.