(Kitco News) – While seasonal factors generally provide a tailwind for gold prices in August, the precious metal faces powerful crosswinds from Jackson Hole, the U.S. election, and ongoing equity volatility, according to the latest monthly report from the World Gold Council (WGC).

“Following a small drop in June, gold posted a strong monthly gain in July to finish 4% higher at US$2,426/oz. Another all-time high was reached mid-month before a modest decline into month end. A strong Japanese yen rally, likely fuelled by a carry trade unwind, ensured it was the only major currency in which gold did not gain during the month.”

“According to our Gold Return Attribution Model (GRAM), gold was propelled higher by lower 10-year Treasury yields and, to a lesser extent, a weaker US dollar,” they said. “The main negative contribution came from COMEX futures, where an increase in open interest was larger than the increase in net longs, leading to a decrease in the ratio – one of our model inputs.”

The WGC noted that the beginning of August saw the third-highest spike in the volatility index (VIX) on record as multiple factors – including a Bank of Japan rate hike, de-leveraging across financial markets, and the weak U.S. nonfarm payrolls report – drove risk assets sharply lower. “Some of the ground has since been made up, but a return to pre-selloff exposure might take time,” they said.

“Market positioning is turning increasingly dovish following recent weak US data prints,” they said. “However, the one-sided bet on cuts leaves some room for disappointment, given a still healthy economy and the Fed’s historical reticence ahead of elections. This could translate to a downside risk for gold should the Fed language not deliver as the market expects.”

August is typically kind to gold prices, but the WGC noted a number of significant risk factors that could disrupt gold’s potential gains.

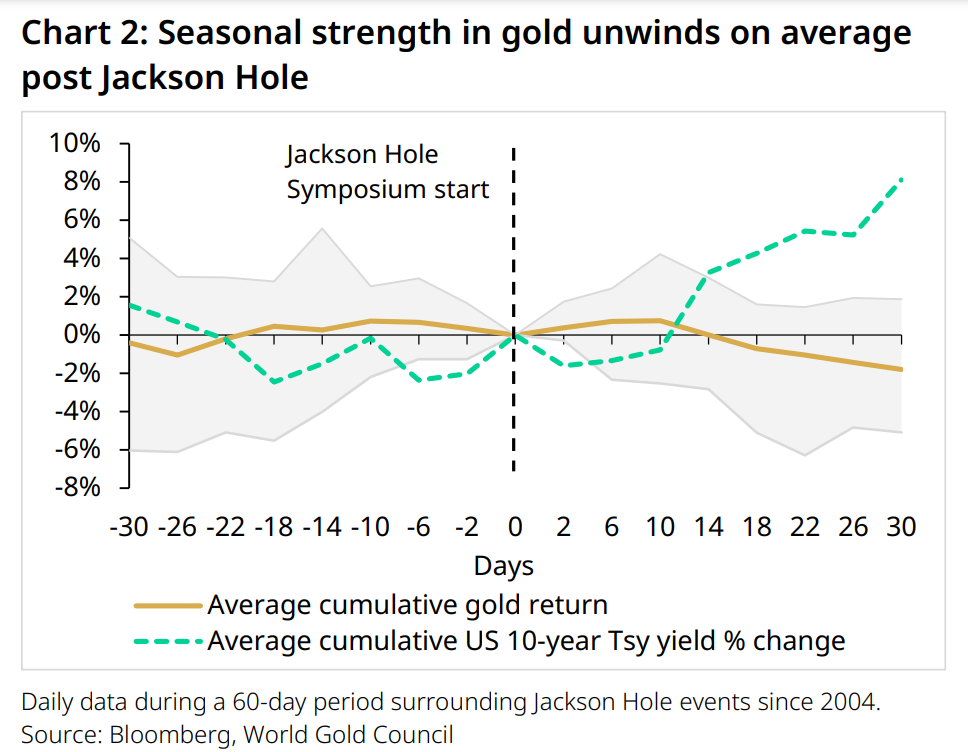

The first of these is the Federal Reserve’s policy tilt coming out of their annual summer symposium.

“Jackson Hole hosts the 47th annual symposium (August 22-24) and comes just weeks before the first expected cut(s) by the Fed (September 18),” the WGC said. “Language will be key as will data leading up to the event. The 31 July FOMC meeting appeared to embolden that a cutting cycle will start in September. Confidence can also be derived from the fact that the Fed very rarely likes to surprise, outside of an exogenous shock.”

But they noted that upcoming data could still steer the Fed in a different direction. “The last few weeks have seen a seesawing of data - alongside huge volatility in equities - with good retail sales, strong GDP and PCE inflation data, as well as PMIs (from S&P) firmly in expansion territory,” they wrote. “But this was followed by much weaker data from the ISM as well as softer non-farm payrolls, leaving a measure of uncertainty on the table.”

“For gold, the symposium has – on average over the last decade – been followed by initial strength then a weakening a few weeks later as bond yields have tended to trend higher.”

They noted, however, that these trends could also reflect an unwind from the previous month’s price action.

“Since the Fed pivot in late December 2023, the Street and broader media have continued to clamour for rate cuts, likely reflecting on one hand a desire to keep the risk-asset party going, and on the other, concerns that the Fed is once again falling behind the curve,” they noted. “Current pricing leaves little room for disappointment. Following the weak August data prints, two cuts are now priced with almost 100% certainty, according to the CME. Speculative positioning in 2-year and 10-year Treasury futures are at multi-year highs. Equities have delivered a stellar expansion in valuations so far this year and we don’t know whether the current pullback will be material. Gold net long positioning is not extreme, but it’s reasonably high.”

“It appears that the Fed has historically been reticent in delivering on expectations ahead of elections, perhaps in an attempt to ward off accusations of political interference,” the WGC said. “A small measure of caution is therefore warranted. If speeches at Jackson Hole hint that expectations are too dovish; equities, bonds and gold are at risk of a downward lurch.”

The second factor U.S. politics, also has the potential to cause significant crosswinds to precious metals prices this month.

“Since President Biden stepped aside for Kamala Harris to carry the torch as the Democratic candidate, polls have dramatically tightened and some forecasts now favour a Democrat victory,” they said, noting the upcoming Democratic National Congress on August 19.

“The distinction between policies is not as clear as it has been historically,” the WGC said. “The fiscal largesse of which Democrats are normally accused is likely to be similar under a Trump administration. To boot, under Trump, materially higher tariffs, preference for a weaker US dollar and anti-immigration are some of the policies that present upside risks to inflation and downside risks to growth.”

“Our view is that gold is likely to benefit from uncertainty more than any political proclivity, and the running mate (VP) confirmation for Harris, is likely to further stir the pot,” they said. “Post the election, the level of national debt and deficit will probably continue to concern investors and keep interest in gold high.”

The third risk factor for gold prices this month comes from stocks, and the tech sector in particular, which has come under considerable pressure recently.

“Q2 earnings for Nvidia, the AI darling and top performer of US equity markets, will be released at the end of August and will cap some poor results from other sector leaders alongside the recent sell off in other indices,” the WGC noted. “For the first time in a while, the market appears nervous. Despite an expectations-beating Q1, two events have dampened the euphoria: a large sale of stock by the CEO Jen-Hsun Huang in June and July, and poorly received guidance from Tesla, Google, Amazon and Intel. NVDAs share price has dropped 28% since peaking in June, while the Nasdaq composite is 12% off its July highs (as of 5 August).”

“Nvidia’s earnings call could be make or break for stocks,” they warned.

The WGC analysts pointed out that while September is usually a weak period for U.S. equities, August tends to be flat with lower volumes as traders go on holiday. “So far this year, August appears to be front-running September weakness,” they said. “Gold’s typically strong negative correlation during equity sell offs should sustain investor interest and their capacity to respond will likely remain, given that positioning isn’t stretched. So far it has done its job.”

“Our take is that these events will keep uncertainty high rather than providing any definitive resolution,” the WGC concluded. “The start of Fed rate cuts is largely premised on normalising economic data. While the employment report and ISM data surprised to the downside, other data has come in quite hot. Suffice to say, the type of economic landing we can expect remains unclear, as such markets pricing two cuts with almost 100% certainty has its risks; for risk assets but also bonds and gold.”

“For gold, elevated uncertainty and event risk is likely to keep interest from investors high,” they added. “So far, it has done a good job in protecting portfolios.”