(Kitco News) – Federal Reserve Chair Jerome Powell used the press conference that followed the central bank’s hefty 50 basis point cut to the benchmark interest rate to insist that the move was not made to support incumbent President Joe Biden on the one hand, nor was it a response to an impending economic collapse on the other.

Powell acknowledged at the outset that recent inflation and employment data led the FOMC to the conclusion that 50 basis points was justified.

“We had the two employment reports, July and August,” Powell said. “We also had two inflation reports, including one that came in during blackout. We had the QCEW report that suggests the payroll report numbers that we're getting maybe artificially high and will be revised down. We have also seen anecdotal data like the Beige Book.”

“We concluded this was a right thing for the economy, for the people that we serve, and that's how we made our decision,” he said.

Asked how markets should determine whether to expect a 25 or 50 bps cut at future meetings, Powell said “A good place to start is the SEP. If you look at the SEP, you will see that it's a process of recalibrating our policy stance away from where we were a year ago when inflation was high and unemployment low, to a place that's more appropriate given where we are now and where we expect to be.”

“There is nothing in the SEP that suggests the committee is in a rush,” he added. “This process evolves over time.”

Powell was asked about the latest Fed projections, which show that the FOMC expects the Fed funds rate to still be above the estimate of long-run neutral by the end of next year, and whether this suggests that officials see the short-run neutral rate as a little higher.

“We know that the policy stance we adopted in July of 2023 came at a time when unemployment was 3.5%,” Powell said. “Today, unemployment is up to 4.2%, inflation is down to a few tenths above 2%. We know that it is time to recalibrate our policy to something that is more appropriate given the progress on inflation, and on employment moving to a more sustainable level. The balance of risks are now even.”

The Fed chair was then asked how close the FOMC vote was in favor of 50 bps, and whether it was clear that this would be the outcome going into the September meeting.

“We left it open going into blackout,” Powell replied. “There was a lot of discussion back and forth, excellent discussion, today. There was also broad support for the decision that the committee voted on.”

“All 19 of the participants wrote down multiple cuts this year,” Powell added. “All 19. That's a big change from June. We made a good, strong start to this, and that's really, frankly, a sign of our confidence that inflation is coming down toward 2% on a sustainable basis. That gives us the ability. We can make a good, strong start. And I'm very pleased that we did.”

Asked about whether the larger cut represents growing concern about the state of the labor market, with the latest Fed projections indicating that unemployment would top out at 4.4%, Powell insisted this was realistic.

“The labor market is in solid condition, and our intention with our policy move today is to keep it there,” Powell said. “You can say that about the whole economy. The U.S. economy is in good shape, it's growing at a solid pace, inflation is coming down. The labor market is at a strong place. We want to keep it there.”

Powell was also challenged on whether the 50 bps cut means the central bank is late to start the easing cycle. “We don't think we're behind,” he replied. “We think this is timely. You can take this as a sign of our commitment not to get behind.”

The Fed chair was challenged on why the economy should not expect a further deterioration in labor market conditions if policy is still at a restrictive level.

“The level of conditions is pretty close to what I would call maximum employment, you're close to mandate on that,” Powell said. “So what is driving it? Clearly payroll job creation has moved down over the last few months, and bears watching. But ultimately, we believe with an appropriate recalibration of our policy, that you can continue to see the economy growing, and that will support the labor market.”

“In the meantime, if you look at the growth and economic activity data, retail sales data we just got, second quarter GDP, all of this indicates an economy that is still growing at a solid pace,” he added. “So that should also support the labor market over time.”

Powell was asked what the FOMC will learn between now and the November meeting that will inform the size of the next move.

“More data than usual,” he replied. “We'll see another jobs report, and we actually get a second jobs report on the Friday before the meeting, and inflation data. We'll get all this data, and we'll be watching.”

Asked about the likelihood of a return to the ‘cheap money’ era that preceded the inflation of recent years, Powell said they can only speculate, but he thinks it’s unlikely.

“Intuitively, many, many people would say we're probably not going back to that era where there were trillions of dollars of sovereign bonds trading at negative rates, and it looked like the neutral rate might be negative,” he said. “It seems so far away now. My own sense is that we're not going back to that, but honestly, we'll find out. It feels to me that the neutral rate is probably significantly higher than it was back then. How high is it? I just don't think we know.”

Powell also fielded a number of questions about whether today’s large rate cut before the election was politically motivated, and designed to support the incumbent president.

“We do our work to serve all Americans,” Powell insisted. “We're not serving any politician, any political figure, any cause, any issue, nothing. It's just maximum employment and price stability on behalf of all Americans. It's a good institutional arrangement which has been good for the public. I hope and strongly believe it will continue.”

The final question for the Fed chair was whether the FOMC saw any potential shock on the horizon that could drive the U.S. economy into recession.

“I don't think so,” Powell replied. “I don't see anything in the economy that suggests that the likelihood of a recession, of a downturn is elevated. You see growth at a solid rate, you see inflation coming down, and see a labor market that is still at very solid levels.”

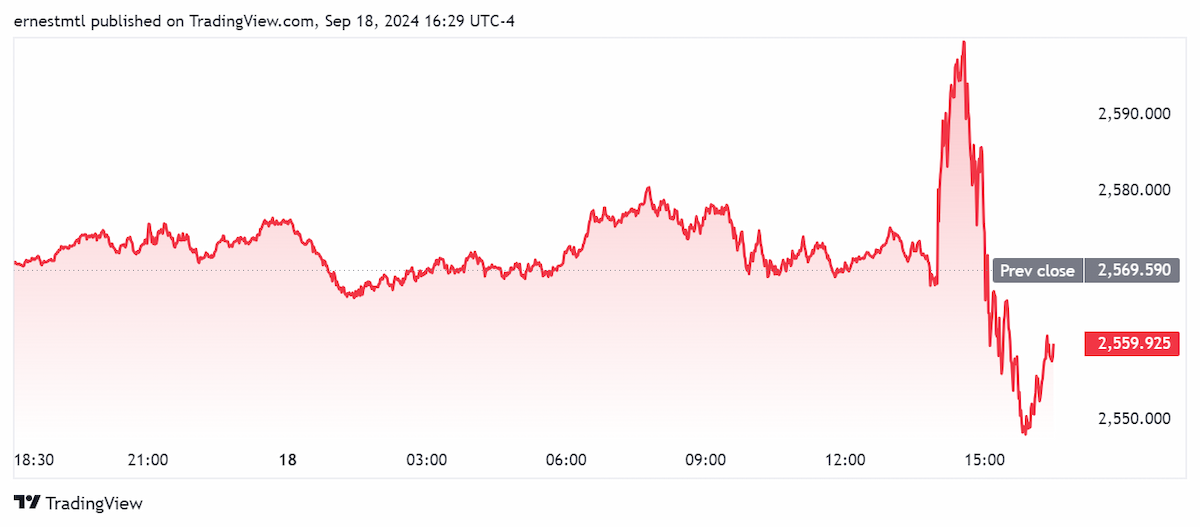

Spot gold whipsawed throughout Powell’s 50-minute press conference, setting both a session (and all-time) high of $2,600.29 per ounce and a then-session low of $2,556.99 during his remarks.

Spot gold last traded at $2,559.92 per ounce for a loss of 0.38% on the daily chart.