(Kitco News) – The recent gold rally is set to lose momentum, but strong fundamentals will keep prices in an elevated range in 2025 and beyond, according to economist Diego Cacciapuoti at Oxford Economics.

In a recent report, Cacciapuoti noted that gold’s price rally has surpassed their already bullish expectations.

“After anticipating the price consolidation in December 2023, we have been consistently vocal about gold's upside potential due to its strong fundamentals, and in early July we re-opened our long on gold prices,” he said. “Strong structural demand – from emerging market central banks and the PBoC in particular – have laid the ground for a very supportive environment.”

Cacciapuoti cautioned, however, that they believe gold prices are vulnerable to consolidation in the near term.

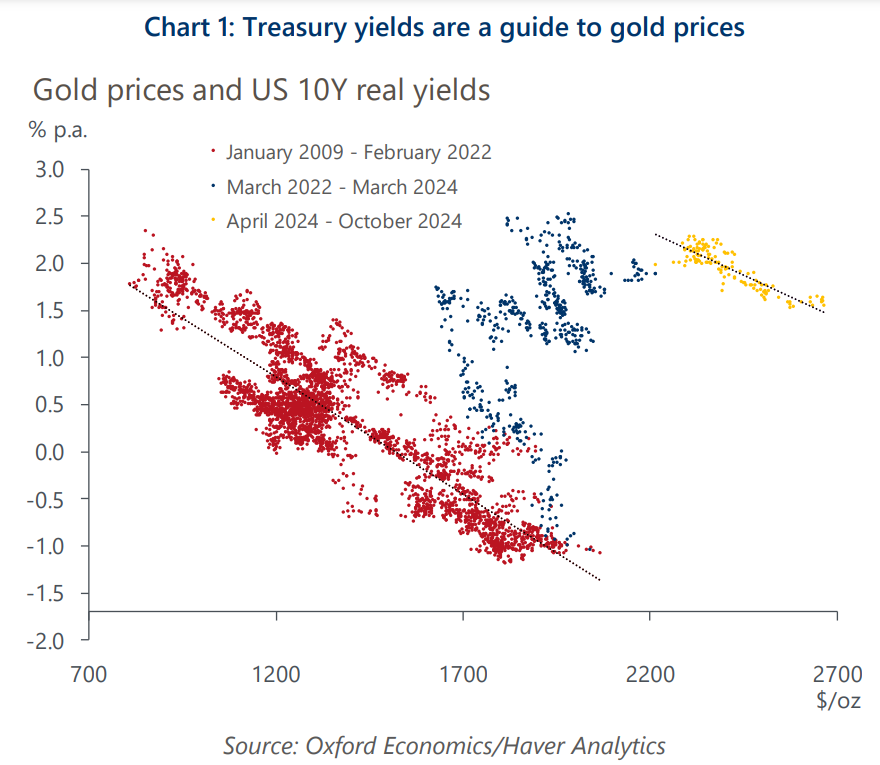

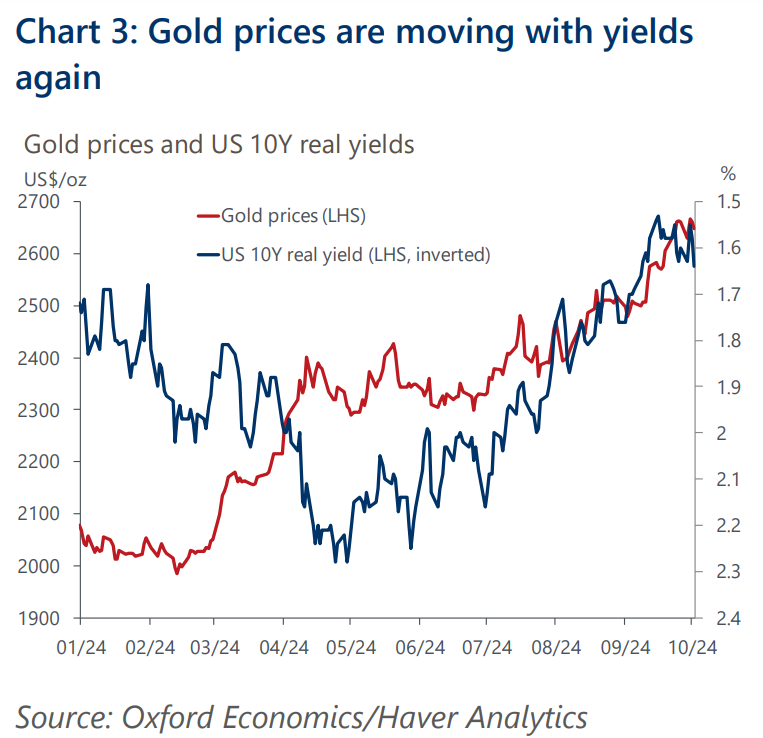

“This is because the rally has been supported by the fall in real yields, which have reduced the opportunity-cost of holding non-yielding assets such as gold,” he wrote. “Yields continue to offer guidance on the direction at the margins for gold prices, even if the negative relationship between gold prices and US yields has recently softened on increased safe-haven demand. Since April – when real rates peaked – lower yields have consistently supported gold again.”

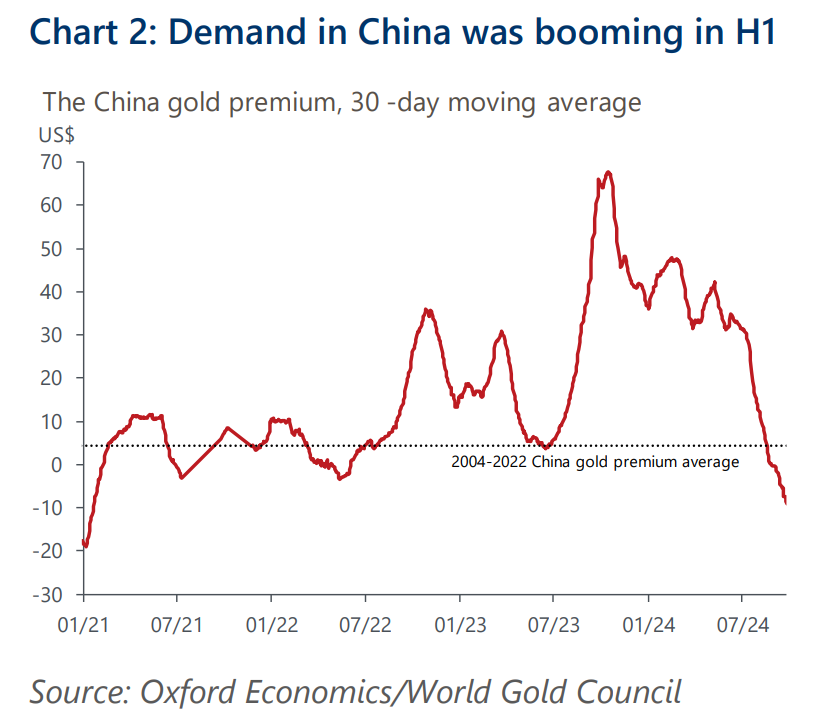

He noted that the negative correlation between real yields and gold paused in the first half of 2024. “At the time, investors were focused on the worrying inflation outlook, and bought gold to protect against the rising risk that inflation may become embedded in the long term,” he said. “In addition, Chinese consumers were diverting private savings away from the subdued property and equity markets toward gold.”

Cacciapuoti said that these two factors, along with strong central bank buying, were able to support gold prices and drive the rally despite rising real yields. “Now, with these forces fading, we think gold is again trading on real yields, and the historical negative correlation has been re-established to a degree,” he wrote.

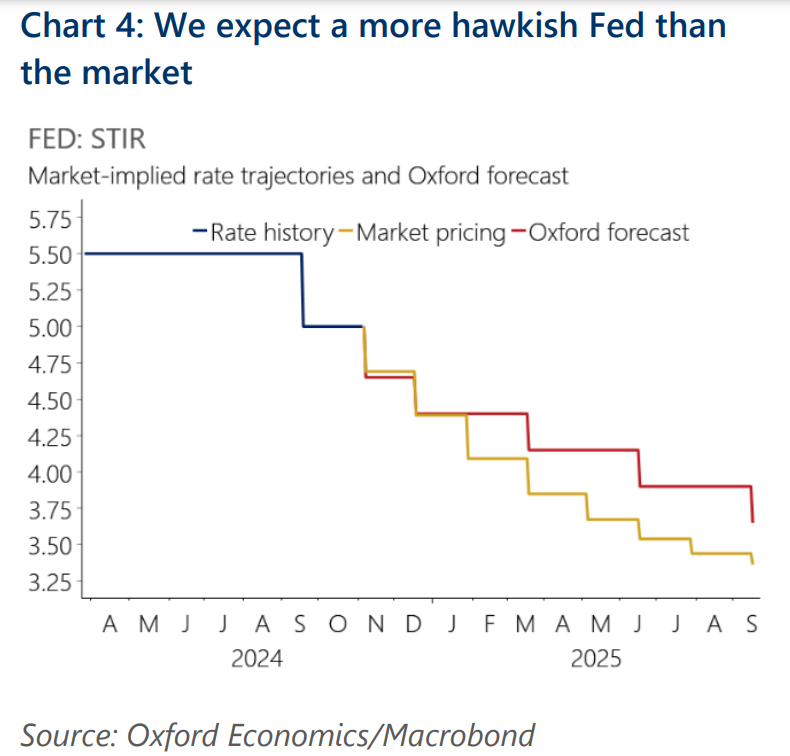

“Given we think the recent decline in Treasury yields will be difficult to sustain in the near term, we think this element of support for gold prices will fade for a while, which leaves room for a gold price consolidation in the very near term,” he wrote. “Markets were too far ahead of the curve last week in pricing 50bps of Fed rate cuts at the November meeting. While we now agree the Fed will cut in November too, we believe it will be in no rush to cut rates by more than 25bps as the US economy is on track to achieve a soft landing.”

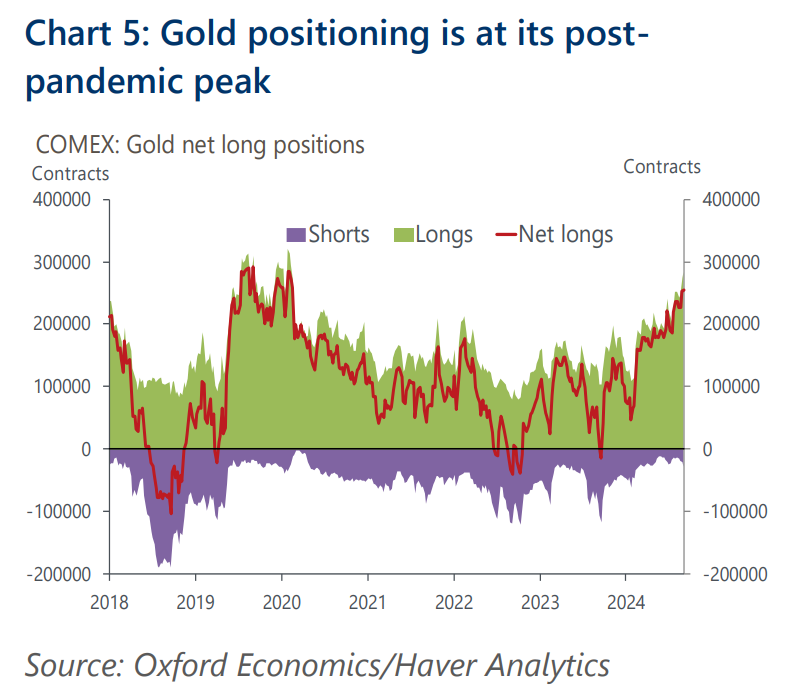

As a result of this updated rate path, Oxford Economics now expects gold prices to come under increasing pressure, and they anticipate some profit-taking. “Investors' positioning is at a postpandemic record-high, and increases have been very small recently despite the large price rallies,” Cacciapuoti said. “This suggests speculators might be losing appetite for the bullion.”

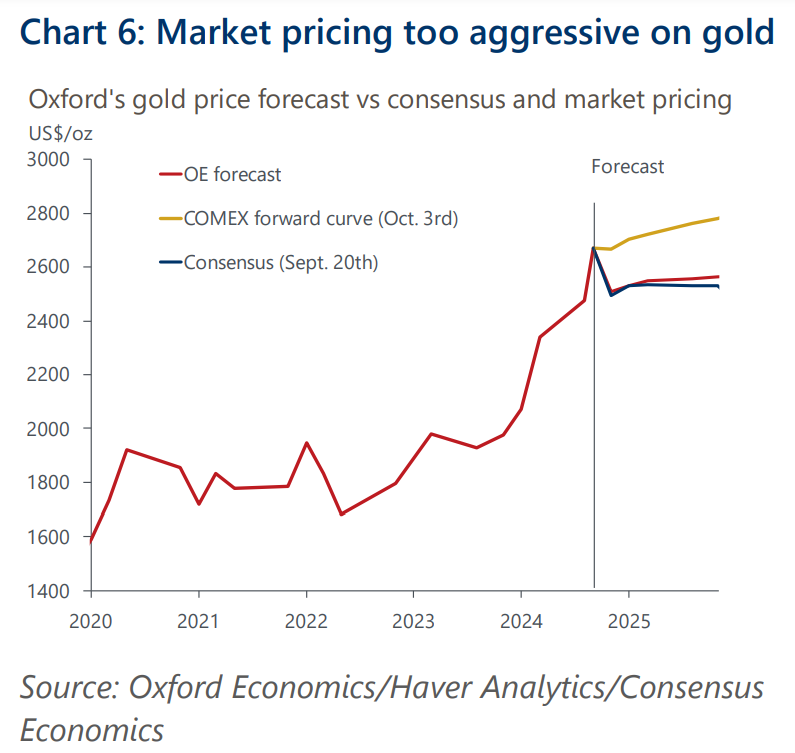

“In fact, with the rally showing signs of exhaustion, we think gold will consolidate just above US$2500/oz – significantly below the very aggressive current market pricing (forward curve),” he noted.

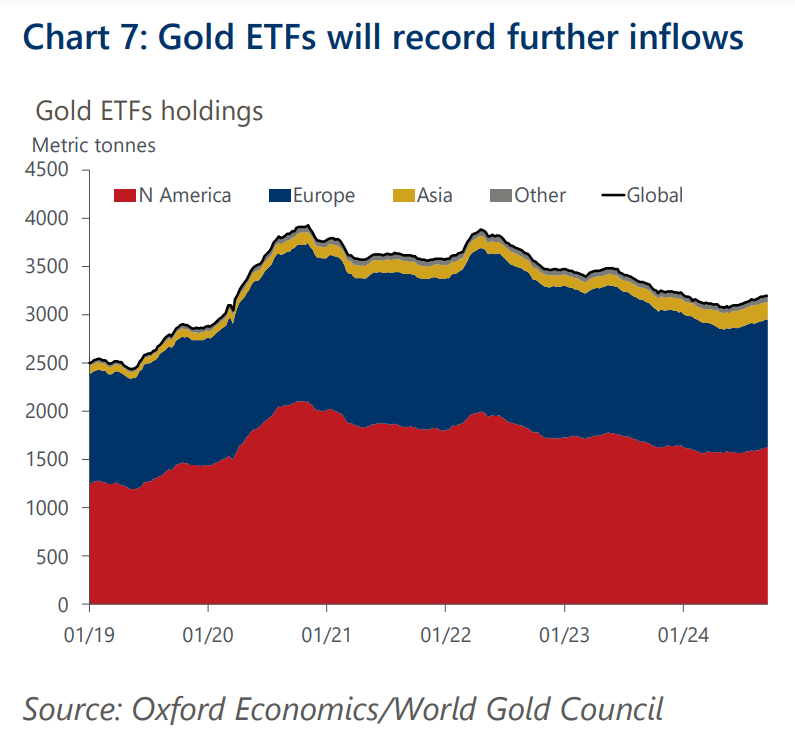

Cacciapuoti still believes that after prices consolidate lower in line with fundamentals, the yellow metal will bounce back, and they are maintaining their strategically bullish view. “This is because falling yields will continue to support ETF demand, which has been rising since May this year (Chart 7), a little after real rates peaked,” he said.

The other structural element Oxford Economics believes will continue to support gold prices is sovereign buying, which they think is nowhere near slowing down.

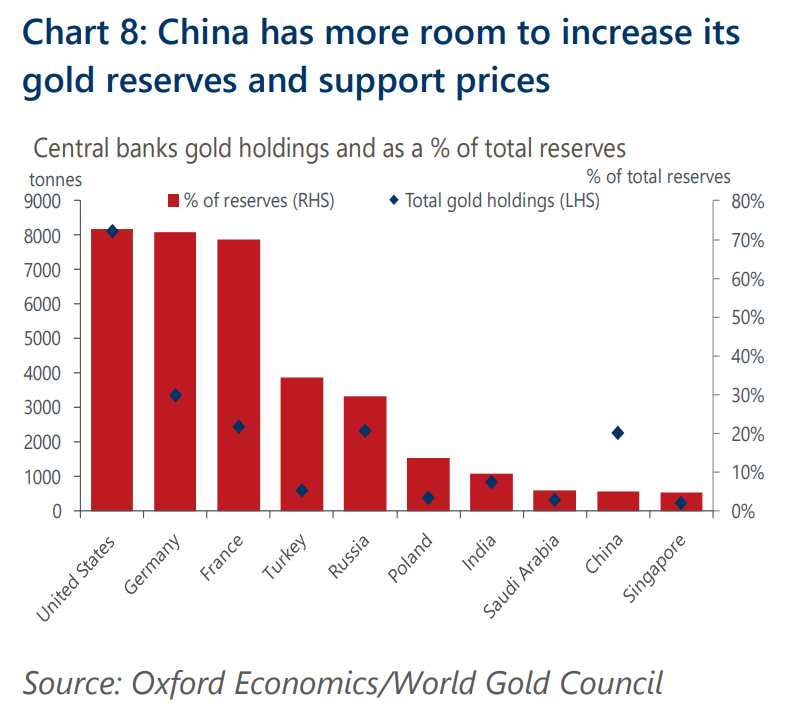

“Some of the largest recent buyers, such as China, still having huge room to continue diversifying their reserves toward gold,” Cacciapuoti wrote. “This is because China's gold holdings are a small percentage of its reserve assets compared to other economies. It also has quite large reserves in absolute levels, which means that even a 1ppt increase in official gold reserves can have a significant impact on gold prices.”

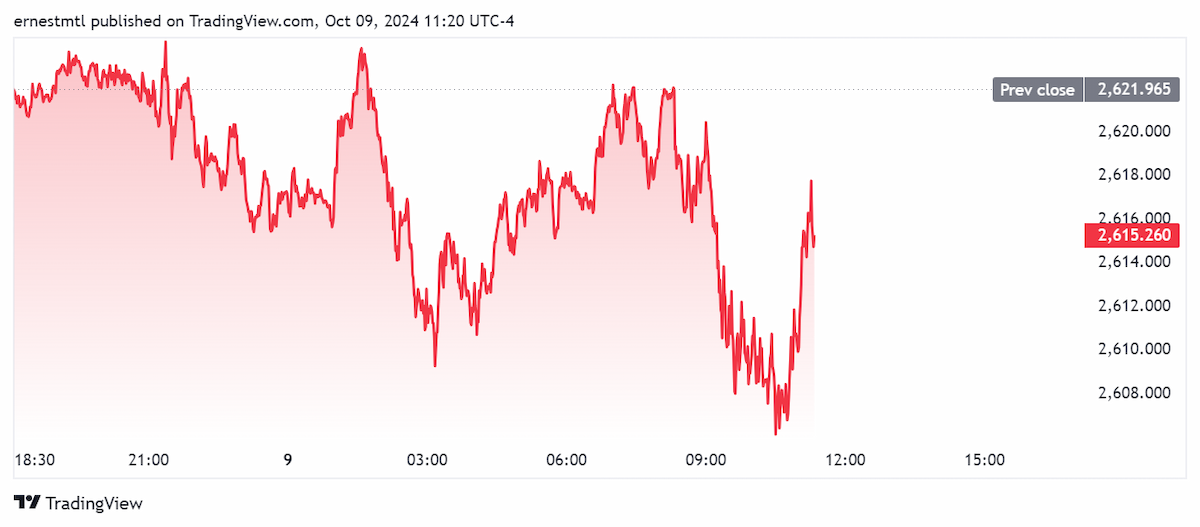

Gold is continuing the week’s volatile price performance on Wednesday morning with spot gold completing a triple-top at $2,622 per ounce just before 8:30 am EDT before setting a session low of $2,605.26 at 10:30 am.

Spot gold last traded at $2,615.01 for a loss of 0.27% on the daily chart.