(Kitco News) – Gold has been flowing West – and to the United States in particular – since Trump’s tariff threats took center stage in precious metals markets. But although elevated geoeconomic risks could cause intermittent spikes in flows, there are signs that the current disruptions are easing, according to the World Gold Council (WGC).

In their latest analysis, the WGC’s Global Head of Research Juan Carlos Artigas and Senior Market Strategist for Europe and Asia John Reade noted the recent rise in COMEX gold inventories, and the widening spread between futures and spot prices, both sparked by tariff uncertainty.

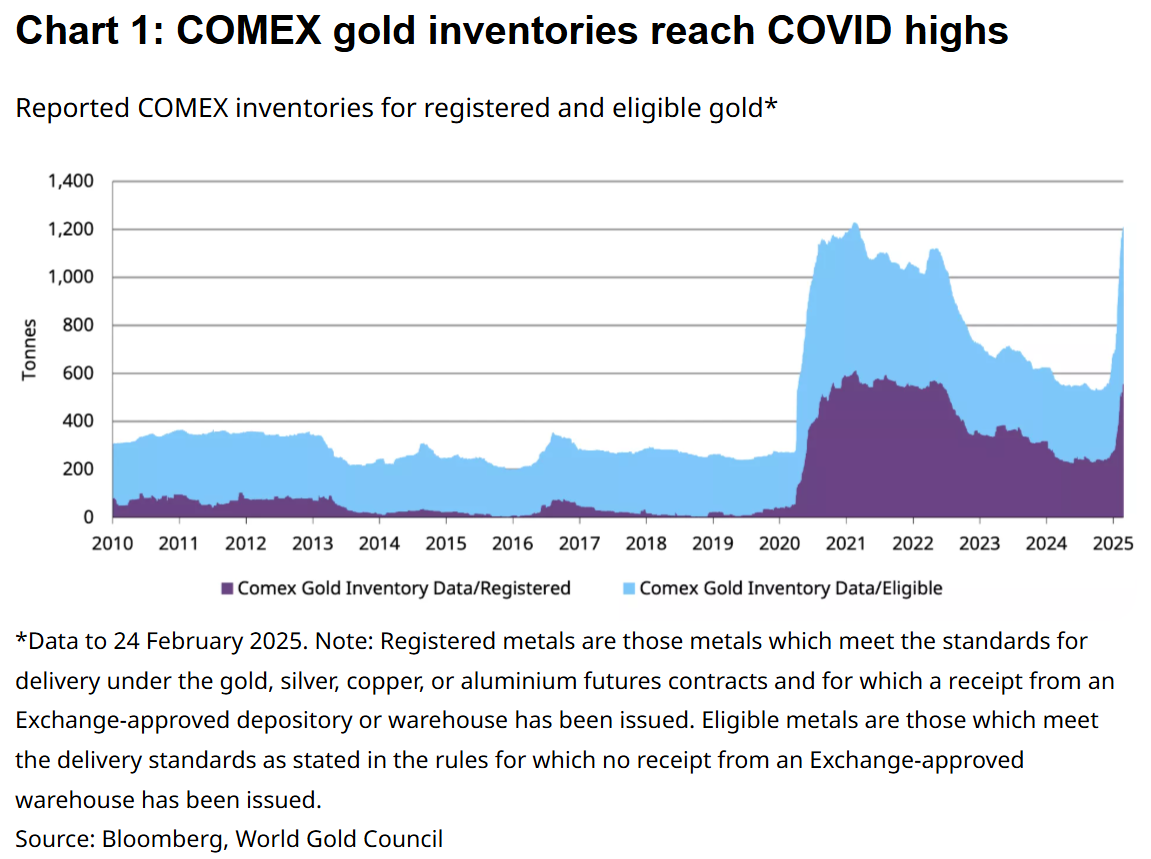

“In late 2024, COMEX inventories started to rise as concerns grew that tariffs could impact gold imports,” they wrote. “This surge of gold imports into the US caught many gold market observers by surprise, as the country is (more or less) self-sufficient in its gold needs, being both a significant producer and a consumer. While gold itself hasn’t been directly targeted, speculation and shifting risk management strategies amid concerns of broad-based tariffs have still had a noticeable impact on prices and trading patterns. This trend has continued into early 2025 and, as of date, COMEX registered and eligible inventories have increased by nearly 300t (9mn oz) and more than 500t (17mn oz), respectively.”

Reade and Artigas explained that speculators and investors “often hold large net-long gold futures positions on the COMEX futures market, while banks and other financial institutions short these futures contracts as counterparties. But these financial institutions are generally not short gold; instead, they run long over-the-counter (OTC) positions to hedge their futures shorts. And because physical gold is more often found in the London OTC market – as a large trading hub and often a cheaper location in which to vault gold – financial institutions typically prefer to hold these hedges in London, knowing that they can quickly – in normal market times – ship gold to the US when there is a need.”

“In recent months, many traders have chosen to pre-empt the threat of tariffs by moving gold to the US, thus avoiding the possibility that they may have to pay higher charges,” they said. “Alongside the increase in inventories, the price of COMEX gold futures contracts – and their spread to spot gold traded in London – also rose, with traders factoring in potential tariff-related costs. For example, the spread between the COMEX active gold futures contract and gold spot reached as much as US$40/oz to US$50/oz (140-180 bps), significantly above the US$13/oz (60 bps) average from the past two years.”

However, they pointed out that these kinds of moves in the gold market are not new. “COMEX inventories – and the differential between futures and spot prices – have risen before, most notably at the onset of the COVID pandemic,” they wrote. “The main question from investors, amidst reports of falling inventories, is: can gold’s largest OTC trading hub, London, cope with the market disruption?”

To answer this question, Artigas and Reade examine the current disruptions in the context of comparable situations, beginning with the Covid-19 pandemic.

“As COMEX inventories rose during COVID, London inventories fell,” they said. “And both eventually normalised. At present, total LBMA reported inventories stand at approx. 8,500t, out of which approx. 5,200t are held at the Bank of England (BoE).”

And while Artigas and Reade noted reports of long queues to retrieve gold at the Bank of England, they said the BoE operates differently from commercial vaults, and “longer wait times create a perception of scarcity that is more likely explained by logistics instead.”

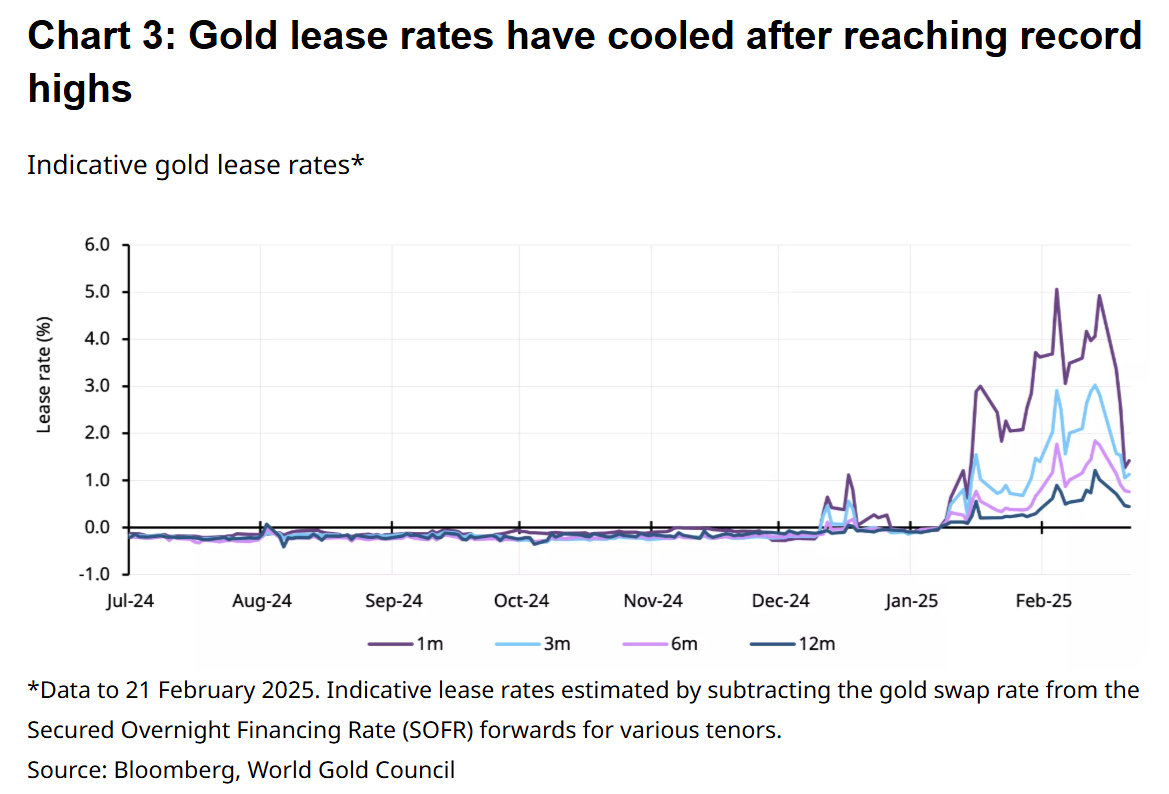

Another consequence of the disruption in flows is an increase in gold’s lending rate. “A calculation based on overnight borrowing rates and gold swap rates, as a proxy, suggests that one-month lease rates reached as high as 5% during January, reflecting ‘tightness’ in the London gold market,” they said.

Artigas and Reade also pointed out that gold’s diverse sources of supply can help support normalization as the current situation unwinds, which appears to have begun.

“Trade data from the Census Bureau suggests that a good portion of gold flowing into the US comes from Switzerland In turn, some of this gold could have originated in the UK as it needs to be refined from Good Delivery (~400 oz) bars into 1 kg bars – the weight accepted for delivery into COMEX futures,” they wrote. “Other sources of gold include Canada, Latin America, Australia and, to a lesser degree, Hong Kong. And then there’s gold from domestic mine production – the US being the fifth largest producer globally – which can be refined locally.”

“Of course, gold flowing into the US from around the world may limit the amount of gold going into other markets, including London, but we believe that the impact should be temporary,” they added. “This is especially true as gold has multiple sources of supply – mine production and recycling – spread around the world, reducing the reliance on imported gold to meet local demand in the medium term.”

The WGC is already seeing signs of normalization in the gold market. “[T]he buildup of COMEX inventories has slowed; the spread differential between gold futures and spot prices is falling, and the bid-ask spread for gold ETFs – many of which vault their gold in London – remain well behaved,” they wrote. “In addition, the lease rates also seems to be cooling down, with data suggesting it is now closer to 1% and well below January’s record high.”

While some of gold’s price gains can be attributed to momentum, the authors’ analysis “suggests that it has been supported by flight-to-quality flows amid increased financial market volatility driven by geoeconomic and geopolitical concerns.”

“Gold has not been a direct target of tariffs, but market reactions to trade uncertainty has driven a significant shift in trading behaviour and impacted the gold price,” they said. “The movement of gold from London to the US, rising COMEX premiums and concerns over availability were largely the result of risk management decisions rather than true supply issues.”

“Now that COMEX inventories appear to be well-stocked and the backlog of withdrawals from the BoE continues to be cleared, these disruptions should ease over the coming weeks,” they concluded. “However, this period serves as a stark reminder that even indirect trade policy concerns can send ripples through global financial markets.”