(Kitco News) – Asian ETF buying is the latest significant driver of the gold rally, but U.S. stimulus measures and easing geopolitical tensions could drive prices 10% lower by year-end, according to Suki Cooper, Precious Metal Analyst at Standard Chartered.

On Thursday morning, Cooper laid out what she believes are the key tailwinds behind gold’s recent gains.

“I think the number of factors that have led this gold rally,” she told Bloomberg Television. “Part of them were laid back in 2022 when we saw central bank buying really pick up, and that's been a core driver that sustained this rally; the downside has been very well supported. But the big shift that we've seen over the past three months has been the inflows of ETFs. That was largely absent, if you look at most of the 2024 rally, but that's really provided that additional catalyst coming into this year.”

“But what's made the rally sustainable – it took five years to get above $2,000 on a sustained basis, but only a matter of weeks to stay above $3,000 on a sustained basis – is the fact that there are so many different drivers behind this rally,” Cooper added. “It's not that traditional correlation with real yields. It's been concerns around recession risks, concerns around tariffs, and whether we see trade wars. It's been concerns around geopolitical tensions. So there's so many different drivers behind this rally, that it's kept gold prices elevated.”

When asked whether she thinks the long gold trade looks overcrowded after a 40% gain over the last 12 months, Cooper pointed to a number of measures indicating there’s still more room for growth.

“When you look at a chart, it looks like it's quite toppy and it's lots of concerns that price action has been quite frothy,” she acknowledged. “But when we look at some of those measures that we can actually look at, they're not overcrowded. So tactical positioning, we're at lows that we saw back in February 2024. The high for the tactical positioning was back in 2019, so we're not overcrowded there. If we look at ETF flows, we’re round about 400 tonnes off the peak that we saw back in 2020. So even now, when we look at inflows, yes, they've picked up across the US and Europe, but those new inflows are actually coming from China, and I think that's what's making this rally different, is that we've got additional demand here, and it's new demand as well.”

Cooper was also challenged on how much more buying Standard Chartered expects to see from central banks after two historically strong years in a row, and whether this represents a longer-term structural change.

“It has been, because it's not just one central bank, it's not just one region,” she replied. “We've seen multiple central banks coming into the space, citing different reasons why they're adding to gold. Some may be looking for a target allocation, but others may be looking for diversification, it may be strategic. So the fact that we've continued to see this buying, yes, some of those volumes have been scaled back over the past quarter or so as prices have scaled record highs, but that buying is still there.”

Asked what Standard Chartered’s year-end target price for gold is, Cooper said they expect the yellow metal to pull back by around 10% over the next seven months.

“We think there are a number of factors that could start to dampen the gold rally by the end of the year,” she said. “Firstly, if you're looking at the correlation here, it’s weakening in real yields, but strengthening in the dollar. We've seen that gold has been a huge beneficiary of safe haven demand amid a lot of the uncertainty.”

“But as we're going into the end of the year – we think that if we see rate cuts, that could be a surprise that lifts gold up again – but if we start to see stimulus measures in the U.S. and we start to see some of the uncertainty around geopolitical risks starting to unwind, we could actually see gold starting to stabilize at elevated levels,” Cooper said. “So remaining above $3,000, but perhaps potentially past its peak by the end of the year.”

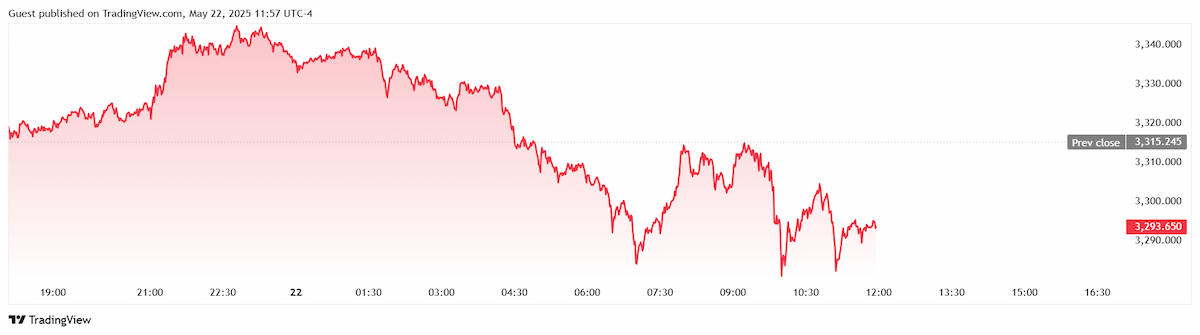

Spot gold slid to a session low of 3,279.23 per ounce at 10 am EDT, and the yellow metal has struggled to reclaim support at $3,300.

Spot gold last traded at $3,293.35 for a loss of 0.66% on the session.