(Kitco News) - After surging to its highest level since April’s all-time highs, the gold market is experiencing some expected profit-taking. However, gold’s overnight rally, triggered by Israel’s preemptive attack on Iran, which involved a barrage of airstrikes that eliminated top military officers and targeted nuclear and missile sites, demonstrates that gold remains a critical safe-haven asset.

In fact, according to one renowned economist, it may be the last safe-haven asset, as the U.S. dollar and U.S. Treasuries have not seen the same inflows as gold amid the renewed conflict in the Middle East.

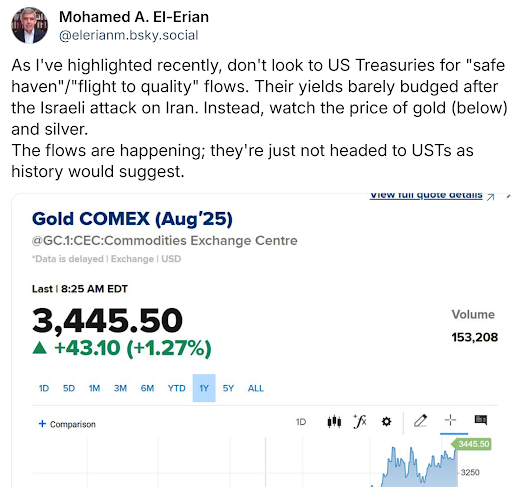

In a Friday social media post, Mohamed El-Erian, former CEO of PIMCO and current president of Queens’ College, Cambridge, warned investors not to rely on the U.S. dollar and Treasuries as safe havens.

“Their yields barely budged after the Israeli attack on Iran. Instead, watch gold (below) and silver,” he said.

Although gold prices have retreated from their overnight highs, the market is still holding solid gains above initial resistance at $3,400 an ounce. Spot gold last traded at $3,421.28 an ounce, up more than 1% on the day. Meanwhile, U.S. 10-year bond yields are near session highs at 4.42%, and the U.S. dollar index continues to struggle near multi-year lows at 98.09 points, up 0.17% on the day.

In a commentary published Friday in the Financial Times, El-Erian said that the new conflict in the Middle East is “bad news at a bad time.”

He noted that rising energy prices will stoke inflationary pressures, which could, in turn, hinder global growth.

“Central banks will now need to intensify their vigilance regarding inflationary pressures that have yet to be confidently contained. This makes it less likely that earlier and larger interest rate cuts will be triggered in response to any slowdown. Meanwhile, any fiscal response would come at a time of still-high interest rates and great investor sensitivity to deficits and debt,” El-Erian said.

Along with the imminent economic threats, El-Erian pointed out that the new geopolitical turmoil will further weaken globalization.

“The global economy also faces the risk of negative indirect effects. With time, the uncertainty arising from this new upheaval in the Middle East may well be seen as adding to the ongoing erosion of the US-led global economic order — further energising the forces of economic fragmentation,” he wrote. “It will also not go unnoticed that the two most significant global financial benchmarks, US Treasuries and the dollar, had a relatively muted initial response to the Israeli attack. Both rallied a little, but neither experienced the type of ‘haven gains’ that historical experience would lead us to expect. This also matters longer term.”

Looking ahead, El-Erian said he sees further downside risks to the U.S. dollar as nations continue to diversify their holdings.

“Due to the lengthy influence of the US over the global economy and its long period of economic exceptionalism, much of the rest of the world is ‘overweight’ the dollar and American assets in general,” he said. “The more the US role at the centre of the global order is diminished, the greater the incentive for countries to reduce this overweight.”