(Kitco News) - The gold market is trading higher ahead of the weekend after the latest data showed consumer sentiment in the U.S. declining more than expected, while inflation expectations rose higher.

The University of Michigan announced on Friday that the preliminary reading of its Consumer Sentiment survey for August was 58.6, which was lower than July’s final reading of 61.7. The data was also well below expectations, as the consensus forecast of economists called for an improvement to 62.

“Consumer sentiment fell back about 5% in August, declining for the first time in four months,” said Surveys of Consumers Director Joanne Hsu. “This deterioration largely stems from rising worries about inflation.”

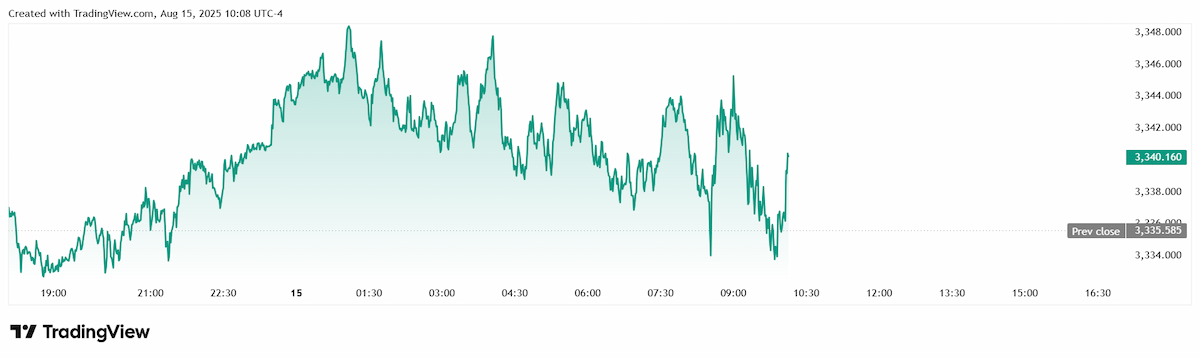

Gold prices shot higher following the 10 am EDT data release, with spot gold last trading at $3,340.27 per ounce for a gain of 0.14% on the day.

The components of the August index showed declines in most areas, with one-year and longer-run inflation expectations rising and consumer spending reflecting the impact of high prices.

“Buying conditions for durables plunged 14%, its lowest reading in a year, on the basis of high prices,” Hsu noted. “Current personal finances declined modestly amid growing concerns about purchasing power. In contrast, expected personal finances inched up a touch along with a slight firming in income expectations, which remain subdued.”

“Overall, consumers are no longer bracing for the worst-case scenario for the economy feared in April when reciprocal tariffs were announced and then paused,” she said. “However, consumers continue to expect both inflation and unemployment to deteriorate in the future.”

The inflation picture continued to deteriorate, with year-ahead inflation expectations rising from 4.5% in July to 4.9% this month. “This increase was seen across multiple demographic groups and all three political affiliations,” Hsu noted. “Long-run inflation expectations also lifted from 3.4% in July to 3.9% in August. This month ended two consecutive months of receding inflation for short-run expectations and three straight months for long-run expectations. Still, both readings remain well below the highs seen briefly in April and May 2025."