(Kitco News) – History indicated that silver is now overvalued in relation to gold, even as sky-high prices are forcing key industries to innovate away from the gray metal, while gold prices continue to move sharply higher despite the de-escalation between the U.S. and Europe over Greenland, according to precious metals analysts at Heraeus.

In the latest update, the analysts wrote that silver’s dramatic outperformance of gold over the last nine months suggests that the rally may be topping out in the near term.

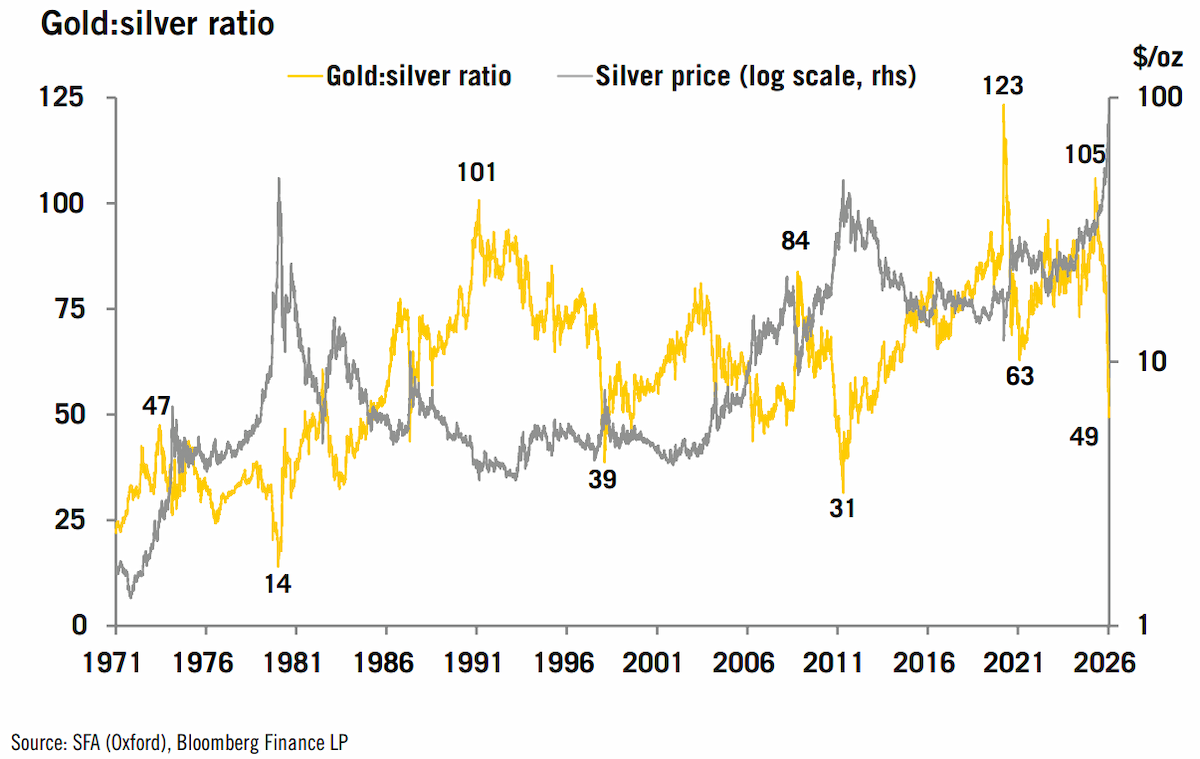

“Historically, silver has outperformed gold in the closing stages of price rallies,” they said. “The gold:silver ratio has fallen from 105 in April 2025 to a low of 49 last week, the lowest level since 2013, even as the gold price continued to hit record highs. The gold:silver ratio has been lower than today several times in the past, but has rarely seen such a large swing in such a short time.”

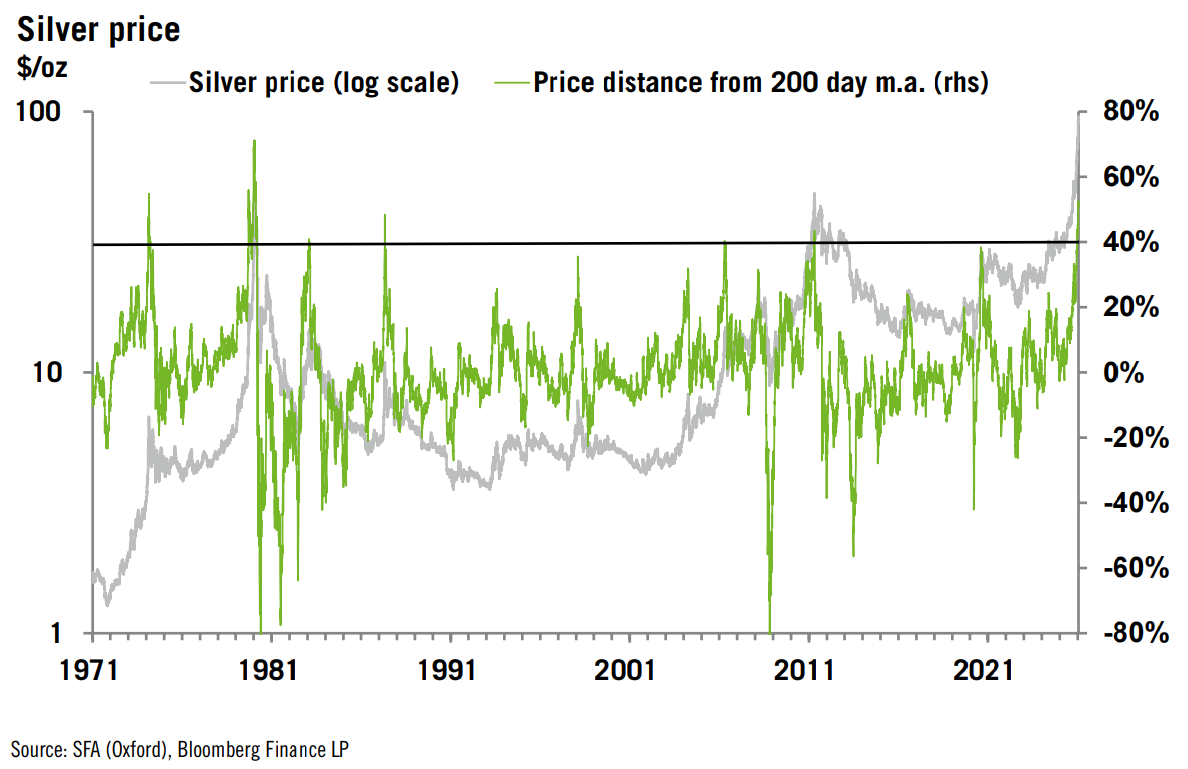

“The silver price rally has become the most extreme since 1980 when the Hunt brothers were trying to corner the market,” the analysts said. “On 23 January, when the silver price rose above $100/oz, it was 54% above its 200-day moving average. In 1980, the silver price at its peak was more than 70% above its 200-day moving average. In 1974, the price also made it as far as 54% above its 200- day moving average before correcting (peak-to-trough drop of 44%), but then the rally continued into 1980.”

“As has been amply demonstrated over recent weeks, even though a price appears to be extreme, it can continue to rally,” they cautioned. “While investors may have legitimate concerns about geopolitical risks, US monetary and fiscal policy, and the fate of the US dollar, history suggests that this rally is much nearer to its end than its beginning. Whether the current bull market will prove to be similar to the 1970s with a correction midway or the bull market will end once the price peaks remains to be seen. Whatever happens, price volatility will likely remain high for some time.”

Heraeus analysts noted that the gray metal’s move above $100 per ounce last week was largely driven by strength in the gold market as geopolitical tensions surrounding Greenland drove safe-haven flows.

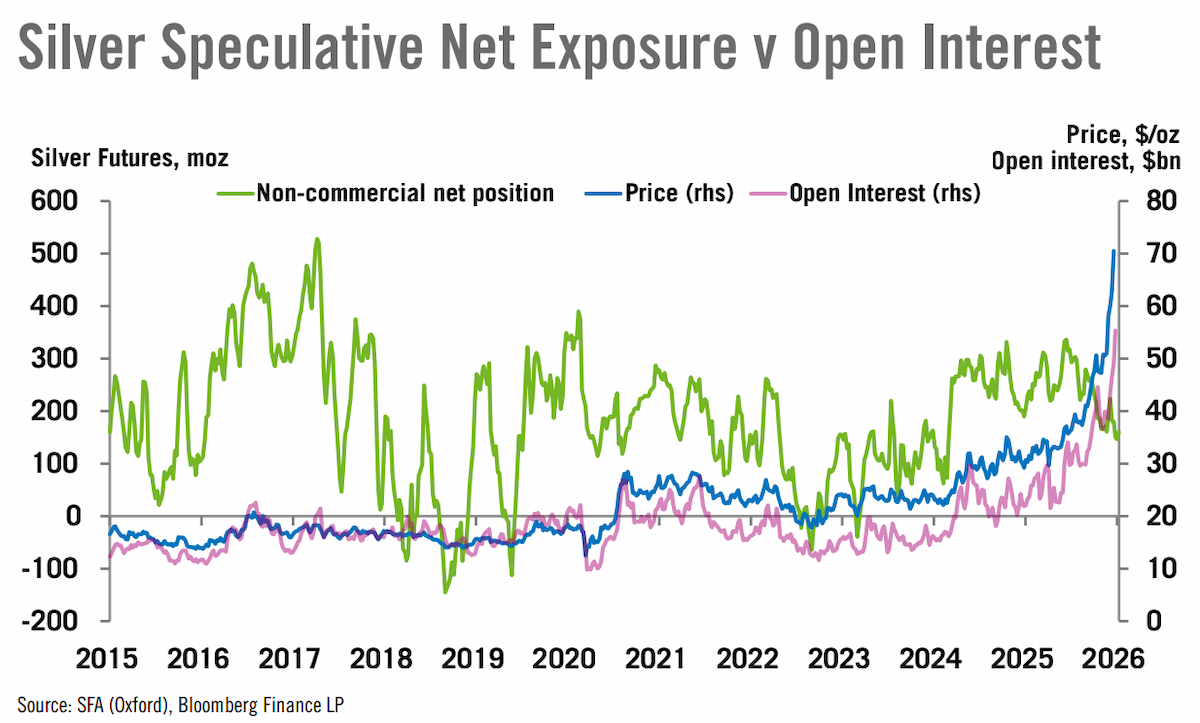

“From a technical perspective, this rally now looks very extended,” they wrote. “The daily relative strength index (RSI) remains above 70, signalling overbought conditions, although currently there is a divergence as the RSI was much higher at the lower price peak in late December. Speculative net long futures exposure has continued to build through January, increasing from 146 moz to 160 moz week-on-week. That said, positioning remains well below the extremes seen in 2025, when speculative net length peaked close to 300 moz, suggesting that there is still potential for further investor engagement.”

Heraeus said the high prices are now eroding industrial demand in price-sensitive sectors. “In photovoltaics, manufacturers are reducing silver intensity and substituting towards copper-based metallisation, with hybrid silver-copper solutions already entering commercial production,” the analysts said. “Recently, China-based metallisation paste supplier DK Electronic Materials announced the commercial development of high-copper paste systems in gigawatt-scale PV production.”

“If industrial demand continues to adapt to high price environments, this could act as a moderating force on the fundamentally driven component of silver prices.”

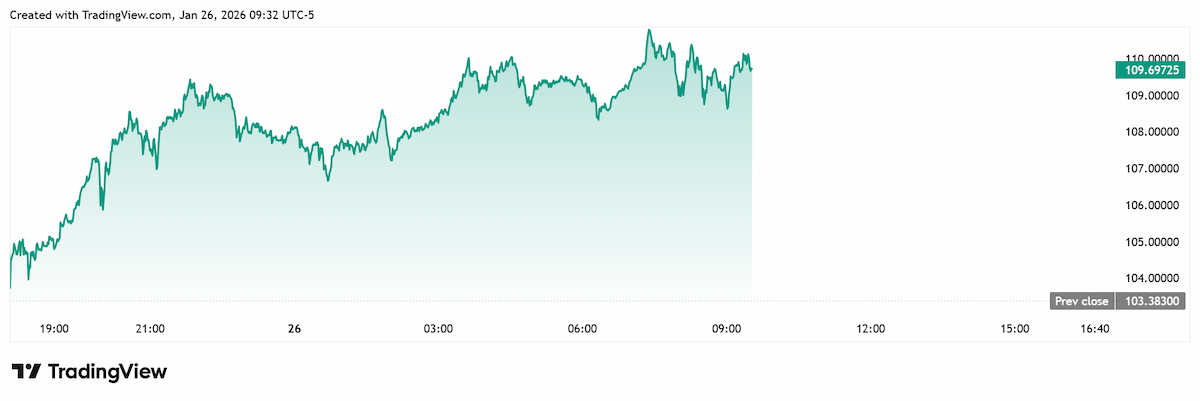

Silver prices are continuing to rocket higher on Monday, with the spot price hitting a new all-time high of $110.899 per ounce just before 7:30 am EST.

Spot silver last traded at $109.672 per ounce for a gain of 6.08% on the daily chart.

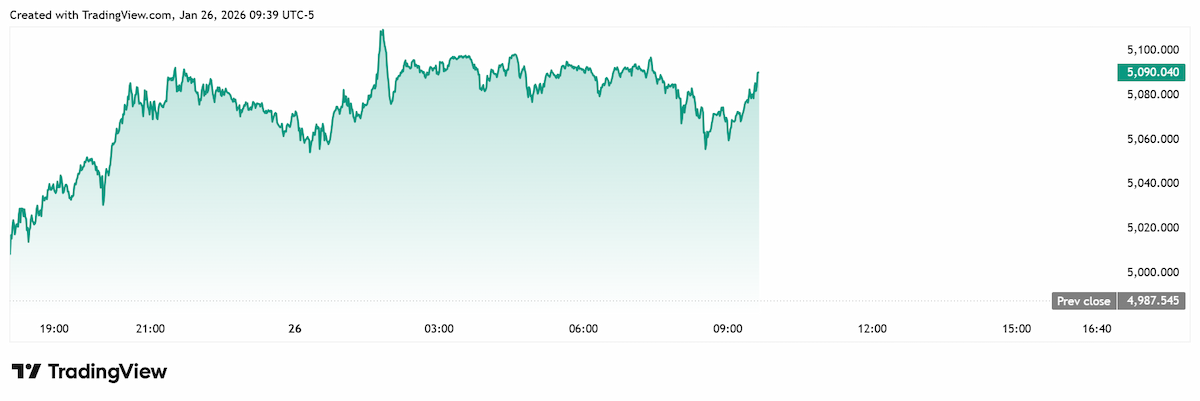

Turning to gold, Heraeus analysts noted that gold ignored last week’s Greenland deescalation on its way to $5,000 per ounce.

“$5,000/oz could act as an attractor in the short term, but once the price gets there, the question is: can the rally be sustained?” they asked. “That may depend on trader sentiment and whether sufficient market participants move from looking for more gains to taking profits.”

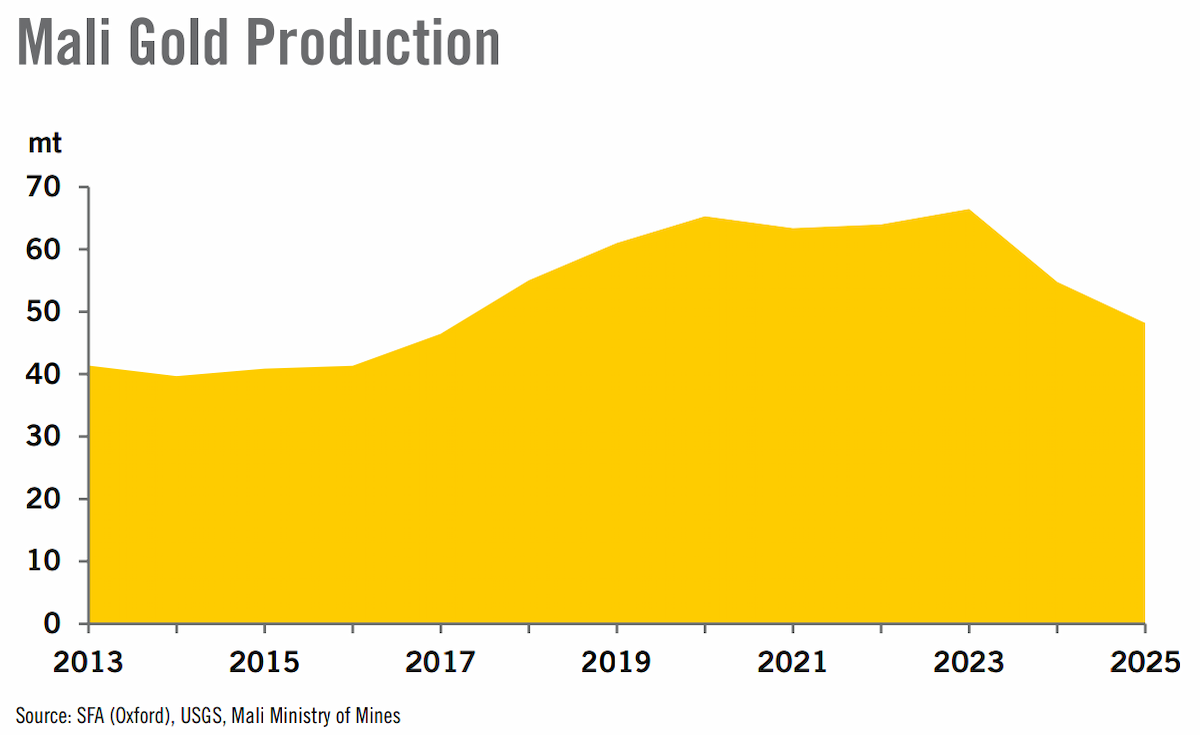

The analysts noted that Mali’s commercial gold production fell 23% to 42.2 tonnes in 2025. “The Loulo Gounkoto mine, the country’s largest, had production suspended for several months during a dispute between the Malian government and Barrick, the mine’s owner,” they said. “The mine operated under a state appointed administrator in the second half of the year, but output was just 5.5 tonnes, down from 22.5 tonnes in 2024. Artisanal gold output remained unchanged at 6 tonnes in 2025.”

Following the agreement between Barrick and the government, the company is set to regain operational control of the mine. “Higher output is likely this year, although a return to full production could take many months,” Heraeus said. “Barrick’s Q3’24 report indicated production could be around 19 tonnes in 2026, but that could be optimistic and further details will likely be provided when the company reports its fourth-quarter results.”

Gold also set a new high of $5,111.51 per ounce earlier Monday morning, and the price is approaching that level shortly after the North American open.

Spot gold last traded at $5,090.34 per ounce for a gain of 2.06% on the session.