(Kitco News) – Policymakers have averted “a global recession and a period of stagflation” and brought inflation down considerably, but unmanageable debt loads and growing trade disputes continue to threaten growth, according to IMF Managing Director Kristalina Georgieva.

Georgieva said the economic policies countries choose “will define how this decade is remembered — will it go down in history as ‘the Turbulent Twenties,’ a time of disturbance and divergence in economic fortunes; the ‘Tepid Twenties,” a time of slow growth and popular discontent; or ‘the Transformational Twenties,’ a time of rapid technological advancements for the good of humanity?”

Georgieva was speaking on Thursday at an event hosted by the Atlantic Council in Washington, DC.

Citing the IMF’s upcoming 2024 World Economic Outlook, slated for release on April 16, Georgieva said that global growth is “marginally stronger on account of robust activity in the United States and in many emerging market economies.” She noted that [s]ustained household consumption and business investment and an easing of supply chain problems helped” and that “inflation is going down.”

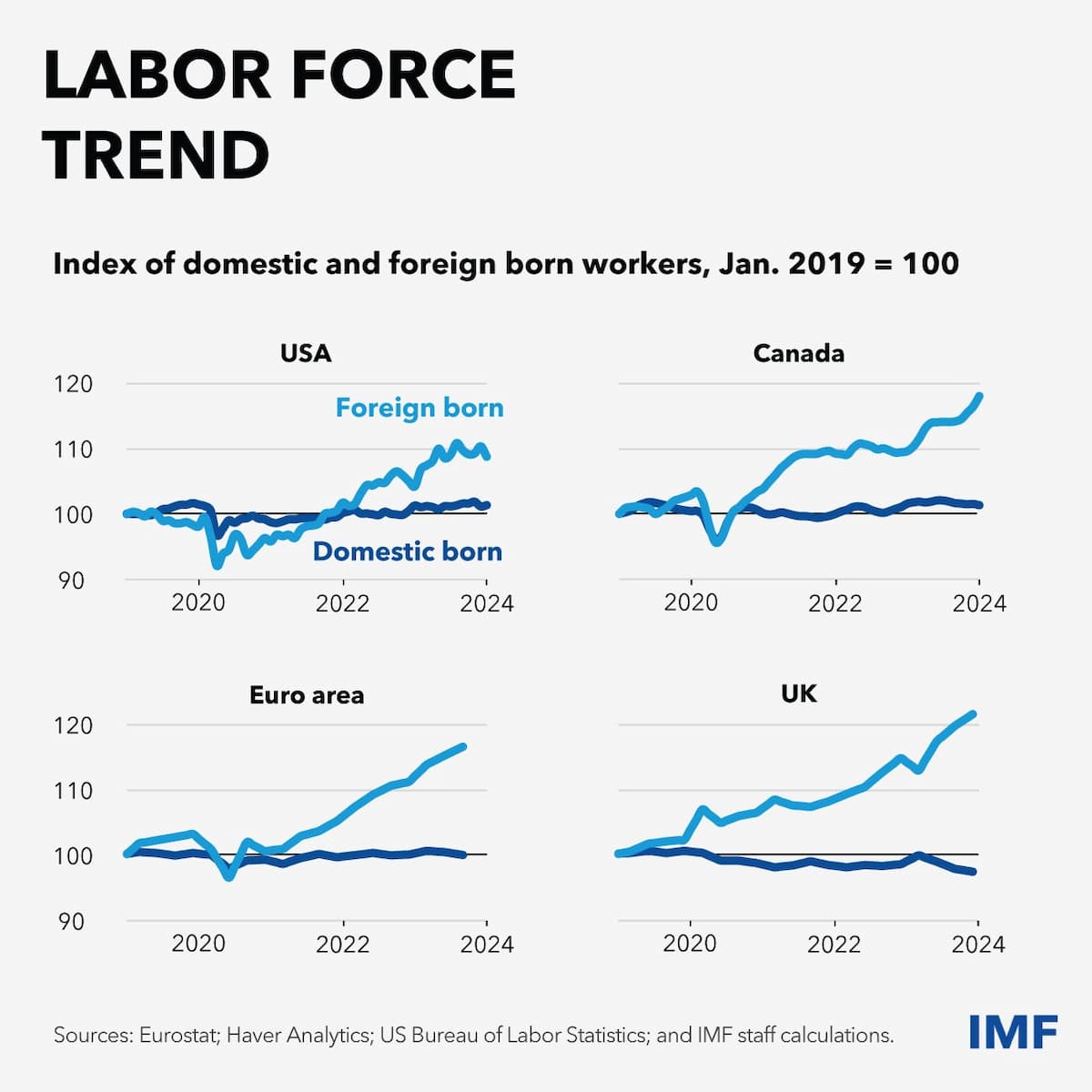

She pointed to “strong labor markets and an expanding labor force” as a significant contributor to the resilience of the world economy and said that immigration “has been especially helpful in countries with aging populations.”

“We have avoided a global recession and a period of stagflation—as some had predicted,” Georgieva said. “But there are still plenty of things to worry about.”

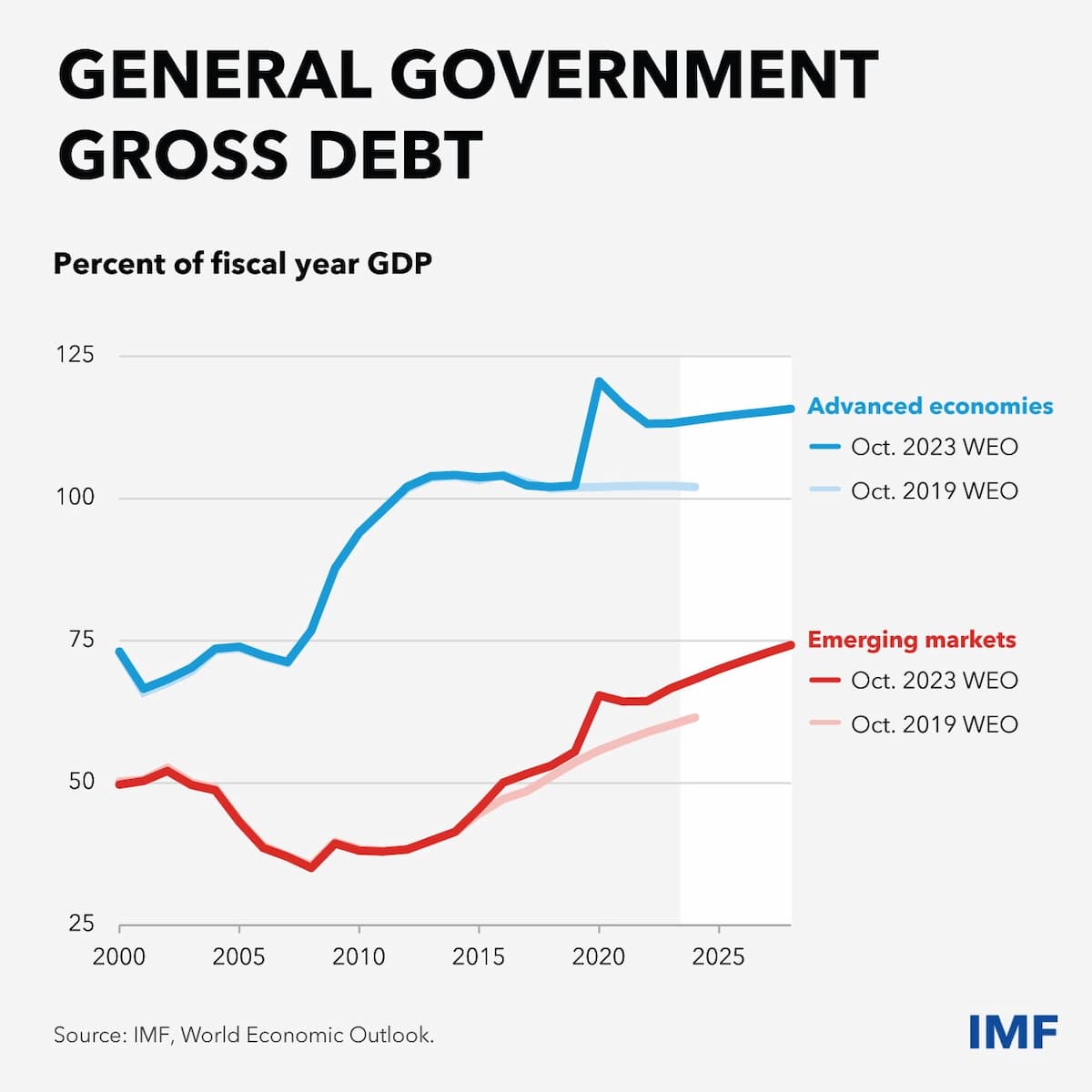

She said that by historical standards, global economic activity remains weak. “Prospects for growth have been slowing since the global financial crisis. Inflation is not fully defeated. Fiscal buffers have been depleted. And debt is up, posing a major challenge to public finances in many countries,” she said.

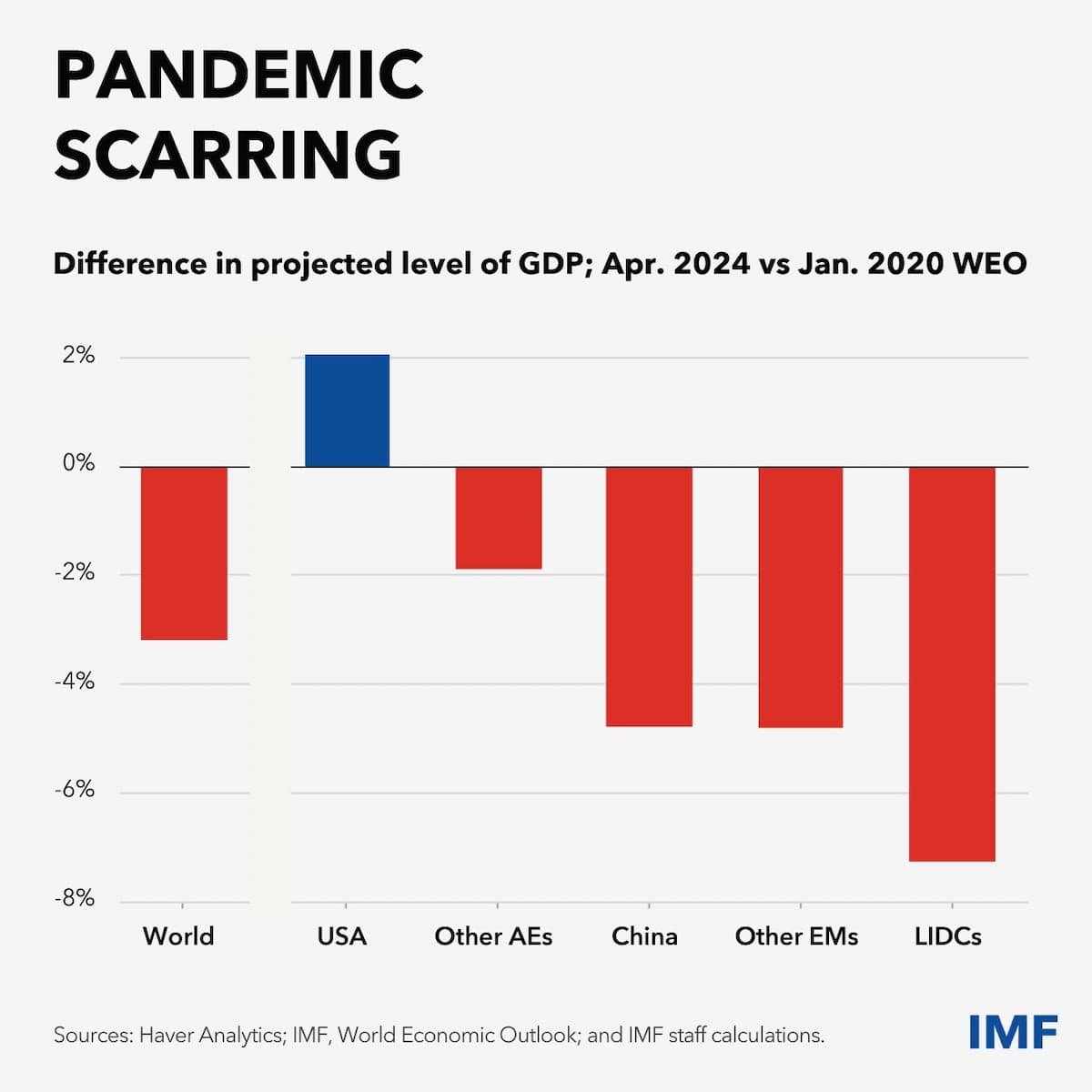

She said that the effects of the pandemic continue to be felt. “The global output loss since 2020 is around $3.3 trillion, with the costs disproportionately falling on the most vulnerable countries,” Georgieva said. “And we see a growing divergence within and across country groups.”

She noted that the United States “has experienced the strongest rebound” among advanced economies, while “activity in the euro area is recovering much more gradually” due to high energy prices and weaker productivity growth.

“But the most striking divergence is for low-income countries for whom scarring has been the most severe,” she said. “Among these nations, fragile and conflicted-affected economies are bearing the heaviest burden.”

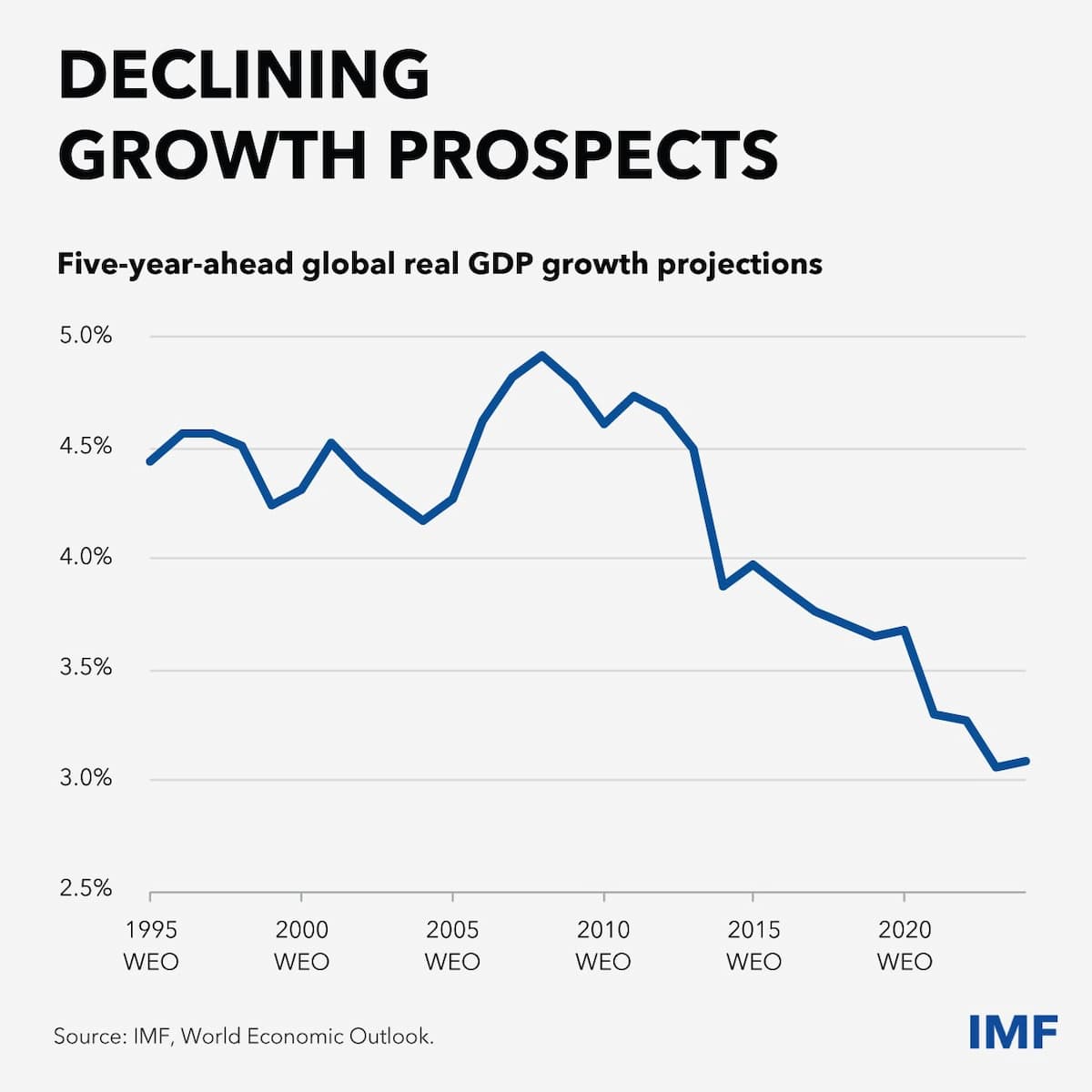

Georgieva pointed to “a significant and broad-based slowdown in productivity” as the primary driver of weaker growth.

“Our analysis shows it accounts for over half of the growth slowdown in advanced and emerging economies, and nearly all in low-income countries,” the IMF director said. “As a result, our medium-term outlook for global growth remains well below its historical average—just above 3 percent.”

Georgieva said that to avoid the ‘Tepid Twenties’ and make this decade the ‘Transformational Twenties,’ the first order of business is “to bring back price stability.”

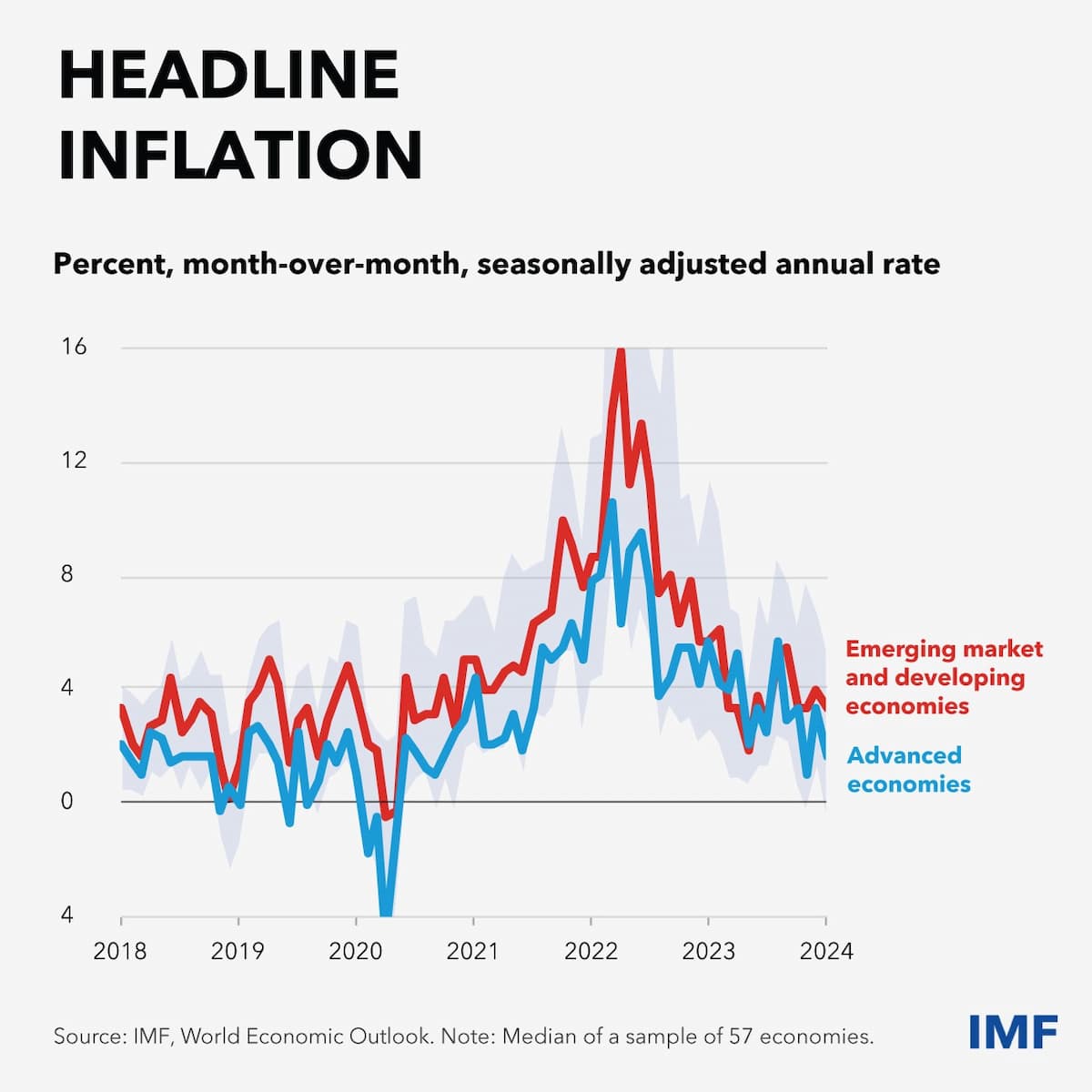

“This is the task of central bankers, many of whom are carefully calibrating this important policy choice—when to cut interest rates and by how much,” she said, noting that “good policy” has brought headline inflation in advanced economies down to 2.3% by Q3 2023 from 9.5% 18 months earlier. “For the median emerging market and developing economy, inflation declined to 4.1 percent,” she added.

Georgieva said the IMF expects this trend to continue throughout the year, which will enable the central banks of the world’s major advanced economy to begin cutting rates in H2 2024.

“But the pace and timing of the monetary pivot will vary,” she said. “Some central banks have already begun to loosen, mostly in emerging markets where inflation was tackled early. But elsewhere—primarily in advanced economies—they are still holding off for now. They must carefully calibrate their decisions to incoming data.”

She said central banks must maintain their independence as “policy credibility is vital in the fight to restore price stability.”

“Where necessary, policymakers must resist calls for early interest rate cuts,” Georgieva said. “Premature easing could see new inflation surprises that may even necessitate a further bout of monetary tightening. On the other side, delaying too long could pour cold water on economic activity.”

The second key policy priority, according to the IMF, should be “to rebuild fiscal buffers.”

“Fiscal buffers are exhausted, and debt levels in most countries are simply too high,” she said, noting that the current trend of rising debts “began more than a decade ago” while interest rates were very low. “The pandemic necessitated an unprecedented fiscal response to protect lives and livelihoods,” she said, during which “[d]ebt surged even more.”

Georgieva said that the current “era of far higher interest rates” is pushing up the cost of servicing all that debt, with advanced economies excluding the U.S., projected to spend 5% of government revenues this year on interest payments on public debt.

“But the cost of servicing debt is most painful in low-income countries,” she said. “Their interest payments are set to average about 14 percent of government revenue—roughly double the level from 15 years ago.”

Georgieva said that fiscal prudence is hard for both rich and poor countries, and this is particularly true “in a year with a record number of elections and at a time of high anxiety due to exceptional uncertainty and years of shocks,”

She said IMF forecasts show deficits “will still be too high to stabilize debt in over one third of advanced and emerging economies, and in more than one quarter of low-income countries” and the organization is calling for the adoption of “credible medium-term fiscal frameworks as the ultimate ‘good policy’ choice for countries.”

We also recommend more focus on closing tax loopholes, strengthening tax collection, and improving the quality of public spending. Fiscal strength allows countries to support the most vulnerable parts of society and to invest in a better future.

The third key priority for the IMF is “policies to reinvigorate growth,” adding that “strengthening governance, cutting red tape, increasing female labor market participation, [and] improving access to capital” could raise output by 8% in four years.

Georgieva said speeding up “the green and digital transition” could be even more impactful. “How well we handle them will define the legacy of this decade,” she said.

She said that AI in particular “brings huge potential benefits but also risks,” noting a recent IMF study that showed AI could affect “up to 40 percent of jobs across the world and 60 percent in advanced economies.”

Georgieva also addressed the ongoing Russia-Ukraine war, saying “there are already signs that trade relations are being re-shaped.”

“As trade flows are re-routed, ‘connector’ countries may benefit,” she said. “But supply chains are lengthening, with potential costs at each step.”

She also pointed out that industrial policies “are back on the agenda,” with over 2,500 policy interventions recorded worldwide last year. “China, the EU, and U.S. account for almost half of the total,” she said.

Georgieva ended by cautioning policymakers against unilateralism. “Working together is the choice of good policies,” she said.