(Kitco News) – Central bank digital currencies (CBDCs) have been receiving a lot of attention in 2024 as U.S. politicians and lawmakers have intensely debated the merits of digital money, with the for and against teams holding firm in their positions.

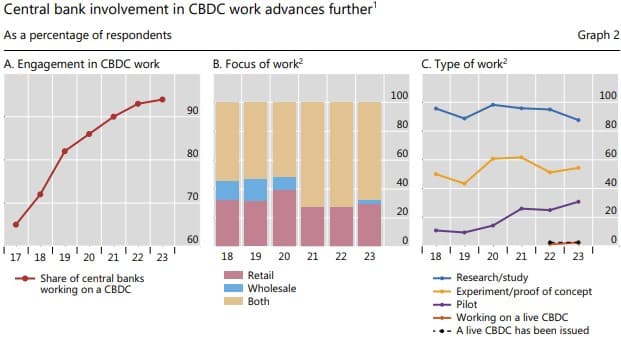

While some have moved to prohibit the creation of a CBDC in the U.S., including the passage of the CBDC Anti-Surveillance State Act by the House of Representatives, globally, the movement to launch digital versions of fiat continues to gain steam. According to the latest survey of central banks from the Bank of International Settlements (BIS), 94% of surveyed central banks are exploring a CBDC.

The survey was conducted in 2023 and included responses from 86 central banks, who “shared insights into their involvement in CBDC work, as well as their motivations and intentions for potentially issuing one.”

The study asked respondents about their engagement in the development of retail (rCBDC), wholesale (wCBDC), or both types of CBDCs and how advanced the work was.

“Central banks’ involvement in CBDCs was already high in 2022 and remained largely constant: at the end of 2023, 94% of responding central banks were engaged in CBDC work,” the report said. “Most central banks are working on both retail and wholesale CBDCs, though not all. Around 30% of central banks focus on retail CBDCs only and 2% are working on wholesale CBDCs only. More than half of the respondents (54%) are experimenting with proofs of concept and one out of three (31%) are running a pilot.”

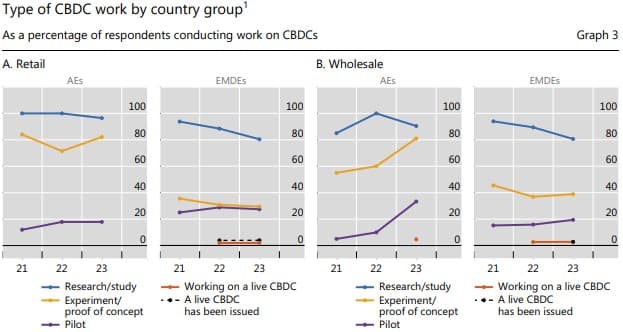

“The survey suggests that central banks are proceeding at their own speed, taking diverse approaches and considering different design features,” the BIS said. “Over the course of 2023, there has been a sharp uptick in experiments and pilots with wholesale CBDCs – mainly in advanced economies (AEs), but various emerging market and developing economies (EMDE) also stepped up their wholesale CBDC work.”

“The share of AE central banks running proofs of concept (81%) or pilots (33%) rose steeply (from 60% and 10%, respectively),” the BIS said. “The share of EMDE central banks working on a wholesale CBDC proof of concept (39%) or pilot (19%) also grew, though less significantly (from 37% and 16%, respectively).”

The survey found that central banks have been studying the implications of retail CBDC for monetary policy implementation and bank intermediation. “Research on wholesale CBDC has been looking into the role of central bank money as a settlement asset for transactions on distributed ledgers,” the report said.

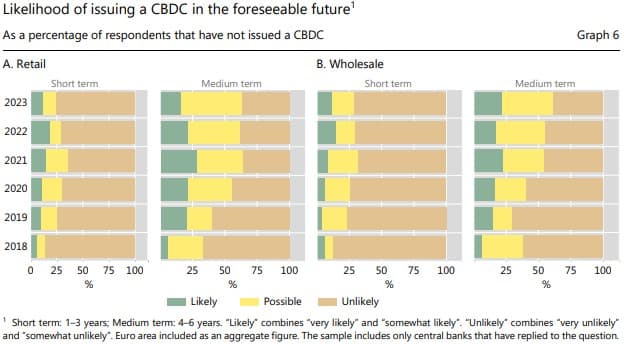

Highlighting the pushback from politicians and lawmakers regarding CBDCs for public use, the survey determined that “the likelihood that central banks will issue a wholesale CBDC within the next six years now exceeds the likelihood that they will issue a retail CBDC.”

As for the key drivers behind central banks' exploration of CBDCs, “Preserving the role of central bank money was a primary concern for more than two-thirds of respondents,” with some mentioning that “a retail CBDC could help ensure the singleness of money, which refers to the convertibility at par between different forms of money,” the BIS said.

“Various central banks have raised concerns that this singleness of money may be threatened by the emergence of new forms of privately issued money,” they added. “Others reported that a wholesale CBDC would enforce the role of central bank money as a settlement asset in a tokenised ecosystem.”

Increasing financial inclusion is another primary driver. “While it is still a more important reason for EMDEs than for AEs, more AE central banks reported financial inclusion as one of their drivers than last year,” the survey found. “In particular, various participating AE central banks reported that a retail CBDC can bring additional benefits in terms of access to digital financial services (often referred to as digital financial inclusion).”

A notable difference from past surveys is the time frame within which central banks expect to launch wCBDCs or rCBDCs.

“Compared with last year, slightly fewer central banks consider it likely that they will issue a retail CBDC within the next three years (12%, down from 18%) or within four and six years (16%, down from 21%),” the BIS said. “This decrease is mainly driven by an adjustment of expectations among EMDE central banks. In addition, more central banks – in both EMDEs and AEs – indicated that short- or medium-term issuance could be a possibility, which can be interpreted as an increased degree of uncertainty. As in previous years, the likelihood of issuing a retail CBDC is generally greater for EMDE central banks than for AE central banks.”

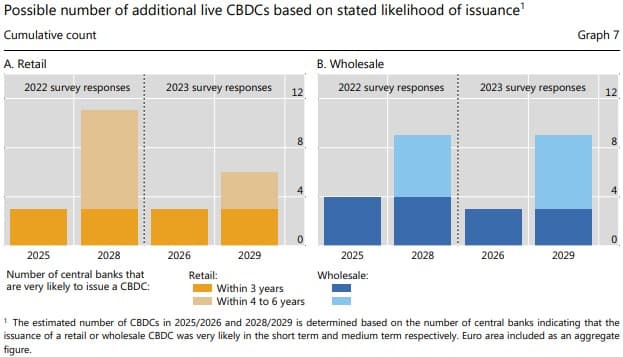

“In sum, the likelihood that a wholesale CBDC will be issued within the next six years is now greater than that for retail,” the report said. “Based on the number of central banks that indicated that they would be very likely to start issuing a CBDC over the next few years, there could be six additional retail and nine wholesale CBDCs publicly circulating towards the end of this decade. In line with the downward-adjusted expectations for retail CBDC issuance, this is fewer retail CBDCs than were predicted last year.”

Central banks have also “enhanced their engagement with stakeholders” to help craft the optimal CBDC design as uptake by stakeholders is crucial to ensuring long-term adoption and use.

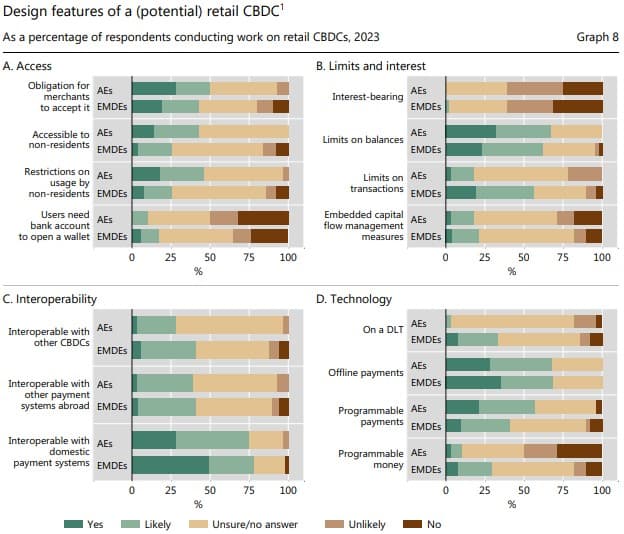

The six-year time horizon highlights that many CBDC features are still undecided, but high on the list for wCBDCs are the interoperability and programmability features that will help ensure a smooth transition and promote wider adoption.

“For retail CBDCs, more than half of central banks are considering holding limits, interoperability, offline options and zero remuneration,” the BIS said. “Differences exist between AEs and EMDEs, for example with respect to the potential use of a distributed ledger and transaction limits.”

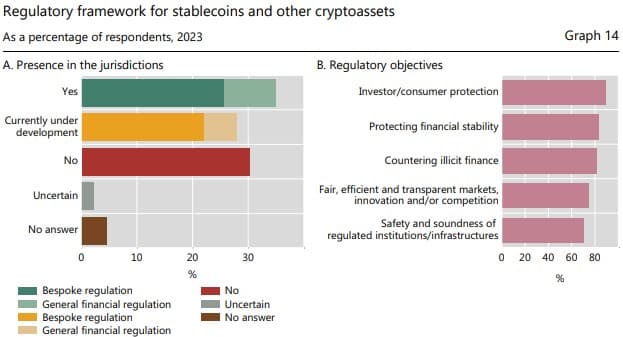

Regarding stablecoins and the potential challenge they pose to CBDC uptake, the BIS survey found that, to date, “stablecoins are rarely used for payments outside the crypto ecosystem. Moreover, about two out of three responding jurisdictions have or are working on a framework to regulate stablecoins and other cryptoassets.”

The BIS also noted increasing efforts by governments to establish clear regulations around crypto assets.

“More than 60% of responding jurisdictions currently have or are developing a regulatory framework for stablecoins and other cryptoassets,” the report said. “Most of these jurisdictions opted for or are developing bespoke regulation (48%), as the opportunities, risks and/or features of cryptoassets would not neatly fit within their existing regulatory frameworks.”

“Existing (and upcoming) regulatory frameworks mainly aim to protect investors and consumers (89%), to safeguard financial stability (83%) and to counter illicit finance (82%),” the BIS added. “Also, many jurisdictions decided to regulate cryptoassets with the aim of promoting market efficiency, innovation and competition (74%) and ensuring the safety and soundness of regulated institutions (70%).”

“Each jurisdiction is unique in terms of economic and social conditions, payment markets and policy objectives. This influences decisions on whether and when to issue a CBDC and on whether and how to regulate stablecoins,” the BIS said. “As jurisdictions may move in different directions or faster than others, global cooperation is key.”

“Although decisions on CBDC and payments regulation are sovereign ones, jurisdictions must collaborate and coordinate in order to offer users a safe and efficient payment experience, both domestically and internationally,” the report concluded. “In the end, payment innovations offer opportunities and risks for all. The best way to navigate through these is to embrace the diversity and advance together.”