(Kitco News) – The minutes from the June 11–12 Federal Open Market Committee (FOMC) meeting showed that while members shared very similar views about the prospects for growth in the U.S. economy and the degree to which inflation had improved, they also showed diverging views about whether the economic situation would warrant rate cuts to support weakening employment or rate hikes to rein in stubborn inflation.

In the staff summary of economic conditions, FOMC members were told that financial conditions had “eased modestly” over the intermeeting period due mainly to higher equity prices. “Taking a somewhat longer perspective, the manager noted that financial conditions had changed little since March but eased notably since the fall,” the minutes read.

The staff also provided a brief overview of the market’s policy rate expectations. “The path of the federal funds rate implied by futures prices shifted a bit lower over the intermeeting period and indicated one and one-half 25 basis point cuts by year-end,” the minutes said. “This shift appeared to reflect mostly changes in perceived risks rather than base-case expectations because the modal path implied by options was virtually unchanged and remained consistent with, at most, one cut this year. The median of modal paths of the federal funds rate obtained from the Open Market Desk's Survey of Primary Dealers and Survey of Market Participants—taken before the May employment report—was also little changed.”

The staff also noted the first interest rate cuts from the European Central Bank (ECB) and the Bank of Canada (BOC). “Market participants reportedly had not expected easing cycles to begin at the same time across economies but appeared to expect that most advanced-economy central banks will have started easing policy within the next several months,” they said.

The staff’s economic forecast prepared for the June meeting was similar to the one from the previous meeting. “The economy was expected to maintain a high rate of resource utilization over the next few years, with real GDP growth projected to be roughly similar to the staff's estimate of potential output growth,” they said. “The unemployment rate was expected to edge down slightly over the remainder of this year and the next and then to remain roughly flat in 2026.”

“Total and core PCE price inflation were both projected to be lower at the end of this year than they were at the end of last year,” the minutes noted. “The staff's inflation projections for this year—which included a preliminary reaction to the May CPI data—were little changed, on balance, from the inflation forecast at the time of the previous meeting. The inflation forecast was higher, however, than at the time of the March meeting and the March Summary of Economic Projections (SEP) submissions.”

“Inflation was still expected to decline further in 2025 and 2026, as demand and supply in product and labor markets continued to move into better balance,” they wrote. “[B]y 2026, total and core PCE price inflation were expected to be close to 2 percent.”

The minutes then moved to the discussions among FOMC members about current and future economic conditions.

“In their discussion of inflation developments, participants noted that after a significant decline in inflation during the second half of 2023, the early part of this year had seen a lack of further progress toward the Committee's 2 percent objective,” they read. “Participants judged that although inflation remained elevated, there had been modest further progress toward the 2 percent goal in recent months. Participants observed that some of this progress was evident in the smaller monthly change in the core PCE price index and a lower trimmed mean inflation rate for April, with the May CPI reading providing additional evidence. Recent data had also indicated improvements across a range of price categories, including market-based services.”

“Some participants commented that sustained achievement of the 2 percent inflation objective would be aided by lower overall services price inflation, and some noted that shelter price inflation had so far been slow to come down,” they added. “A few participants also highlighted the strong increases recorded this year in core import prices. Nevertheless, participants suggested that a number of developments in the product and labor markets supported their judgment that price pressures were diminishing.”

Looking ahead at the inflation outlook, FOMC members “highlighted a variety of factors” that they believed would contribute to continued disinflation. “The factors included continued easing of demand–supply pressures in product and labor markets, lagged effects on wages and prices of past monetary policy tightening, the delayed response of measured shelter prices to rental market developments, or the prospect of additional supply-side improvements,” they wrote. “The latter prospect included the possibility of a boost to productivity associated with businesses' deployment of artificial intelligence–related technology.”

“Participants observed that longer-term inflation expectations had remained well anchored and viewed this anchoring as underpinning the disinflation process,” they added. “Participants affirmed that additional favorable data were required to give them greater confidence that inflation was moving sustainably toward 2 percent.”

Regarding the employment situation, members noted that “demand and supply in the labor market had continued to come into better balance” and said that “many labor market indicators pointed to a reduced degree of tightness in labor market conditions,” including “a declining job openings rate, a lower quits rate, increases in part-time employment for economic reasons, a lower hiring rate, a further step-down in the ratio of job vacancies to unemployed workers, and a gradual uptick in the unemployment rate.”

Turning to the growth forecast, FOMC members “noted that recent indicators suggested that economic activity had continued to expand at a solid pace,” they expected that real GDP growth in 2024 “would be below the strong pace recorded in 2023,” and they pointed out that “recent data on economic activity were largely consistent with the anticipated slowing.”

“Participants continued to assess that the risks to achieving their employment and inflation goals had moved toward better balance over the past year,” the minutes stated. “Participants cited a number of downside risks to economic activity, including those associated with a sharper-than-anticipated slowing in aggregate demand alongside a marked deterioration in labor market conditions, or with strains on lower- and moderate-income households' budgets leading to an abrupt curtailment of consumer spending. A few participants pointed to downside risks to economic activity associated with the fragility of some parts of the CRE sector or the vulnerable balance sheet positions of some banks.”

The minutes said that some FOMC members also shared reasons why they believed inflation could remain above the 2 percent target for longer than expected. “These participants pointed to risks that inflation could stay elevated as a result of worsening geopolitical developments, heightened trade tensions, more persistent shelter price inflation, financial conditions that might be or could become insufficiently restrictive, or U.S. fiscal policy becoming more expansionary than expected; the latter two scenarios were also seen as implying upside risks to economic activity,” they said. “Several participants also cited the risk of an unanchoring of longer-term inflation expectations.”

Turning to the outlook for monetary policy, “participants noted that progress in reducing inflation had been slower this year than they had expected last December,” the minutes stated. “They emphasized that they did not expect that it would be appropriate to lower the target range for the federal funds rate until additional information had emerged to give them greater confidence that inflation was moving sustainably toward the Committee's 2 percent objective.”

“In discussing risk-management considerations that could bear on the outlook for monetary policy, participants assessed that, with labor market tightness having eased and inflation having declined over the past year, the risks to achieving the Committee's employment and inflation goals had moved toward better balance, leaving monetary policy well positioned to deal with the risks and uncertainties faced in pursuing both sides of the Committee's dual mandate,” they noted. “The vast majority of participants assessed that growth in economic activity appeared to be gradually cooling, and most participants remarked that they viewed the current policy stance as restrictive.”

However, the minutes also noted that some FOMC members expressed doubts about the degree to which the current policy was restrictive. “Some remarked that the continued strength of the economy, as well as other factors, could mean that the longer-run equilibrium interest rate was higher than previously assessed, in which case both the stance of monetary policy and overall financial conditions may be less restrictive than they might appear,” the minutes stated. “A couple of participants noted that the longer-run equilibrium interest rate was a better guide for determining where the federal funds rate may need to move over the longer run than for assessing the restrictiveness of current policy.”

The minutes also said “[s]everal participants observed that, were inflation to persist at an elevated level or to increase further, the target range for the federal funds rate might need to be raised,” while “A number of participants remarked that monetary policy should stand ready to respond to unexpected economic weakness.”

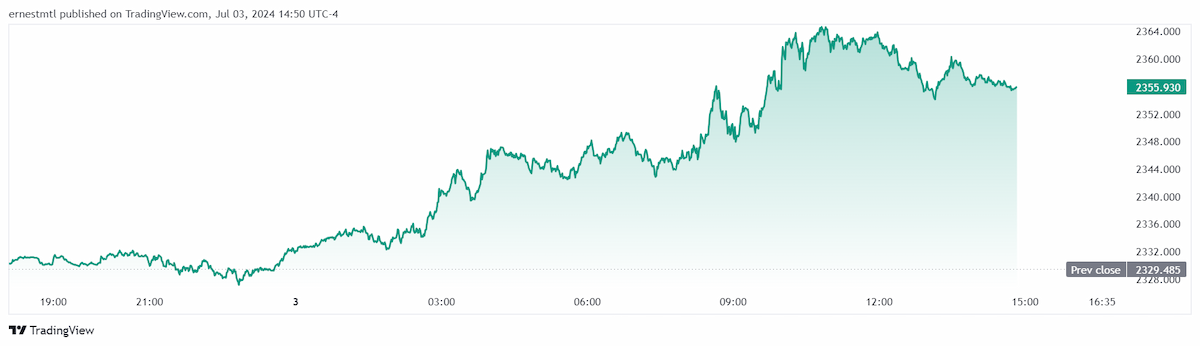

Gold prices were remarkably stable following the publication of the FOMC minutes, with spot gold trading in only a $2 range since the 2 pm EDT release. Spot gold last traded at $2,355.93 for a gain of 1.13% on the session.