(Kitco News) – Even as commodities have given back all of 2024’s gains, precious metals have continued to shine, and now ETF investors are showing renewed interest in gold, according to Ole Hansen, Head of Commodity Strategy at Saxo Bank.

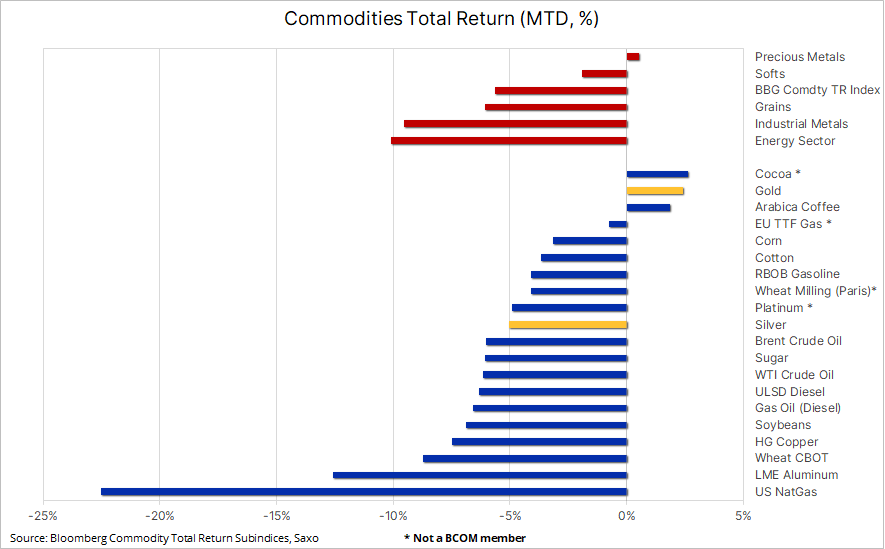

“[T]he commodities sector has erased this year’s gains amid China growth worries, a sharp sell-off in energy led by natural gas, and weakness across industrial metals, with copper suffering a major round of long liquidation from investors due to a mismatch between weak short-term fundamentals and an overriding positive long-term outlook,” Hansen wrote in a report published Tuesday. “Additionally, crop-supportive weather across the northern hemisphere has raised the prospect of another bumper crop production season.”

“These developments have caused the Bloomberg Commodity Total Return Index to suffer a 5% setback this month, leaving the index close to flat on the year, with the only sector barely in the black this month being precious metals, thanks to gold’s continued resilience amid a number of different supportive developments.”

Hansen cited the recent Gold Demand Trends Q2 2024 report from the World Gold Council, which showed record demand despite record-high prices. “OTC investment of 329t was a significant component of Q2 total gold demand,” he noted. “Together with continued central bank buying, it helped drive the price to a series of record highs during the quarter.”

The report showed that “regional investment trends continued to diverge” with demand for bars, coins and ETFs remaining robust in the East against a marked decline in the West, but Hansen pointed out that “Western ETF investment flows have, however, started to return so far in Q3.”

Turning to the price action, Hansen highlighted that gold’s new all-time high price was just below Saxo’s $2,500 per ounce end-of-year target after market participants took recent U.S. data as confirmation that the Fed’s rate-cutting cycle would begin in September rather than December.

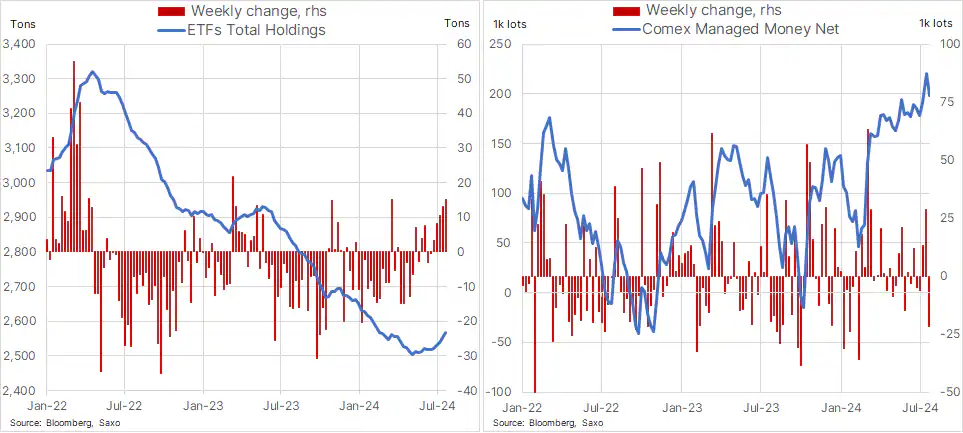

“Lower funding costs for holding a position in a non-interest paying metal, such as gold, will increase its attractiveness, and during July we have seen some early signs that interest rate-sensitive investors have started to warm up to gold, with the total holdings across the major exchange-traded funds showing the biggest monthly increase since March 2022 when total holdings peaked above 3200 tons, only to suffer months of net selling amid rapid rising US interest rates,” he said.

“Managed money accounts such as hedge funds and CTAs jumped into gold back in February and March at prices well below USD 2200, and deep in-the-money positions and with that the lack of selling pressure from position adjustments help explain why the yellow metal has only seen relatively small corrections during the past few months,” Hansen said. “As opposed to silver, which has suffered much higher volatility and bigger corrections after recent established longs were forced to reduce amid weakness across the industrial metals sector, not least copper.”

He noted that since ETF holdings began declining in April 2022, gold prices have rallied from below $1,900 per ounce to nearly $2,500, “and it highlights gold’s strong support from multiple different sources other than yields, rates and the dollar.”

The most significant sources of support that Hansen sees for the yellow metal are “Geopolitical risks related to Russia/Ukraine, the Middle East and not least uncertainty regarding the November US president election,” strong retail demand in China related to the declining economy and property market and risk of Yuan devaluation, “Continued central bank demand amid geopolitical uncertainty and de-dollarisation,” and the rising debt-to-GDP ratios among major economies including the United States.

“In addition, we are now increasingly seeing the positive impact of an incoming US rate cutting cycle, a period that historically has seen the yellow metal perform well,” he said. “Traders will be looking to Wednesday’s US FOMC meeting for guidance, and while we expect the meeting to have a minimal impact on rates repricing, the market is likely to maintain expectations of upcoming rate cuts, potentially already from September, based on concerns that inflation is now on a downward trajectory to 2% while the US economy is slowing as consumers are pulling back on spending, which accounts for roughly 70% of the country’s economic activity.”

“With three US rate cuts priced in this year, as opposed to the FOMC’s projection of just one, some short-term disappointment cannot be ruled out, but overall the direction towards higher prices in the months and quarters ahead remains,” Hansen concluded. “Key support can be found in the USD 2280 area while short-term resistance has emerged around USD 2325.”