(Kitco News) – The spread between the Shanghai and London gold prices rose sharply in December, but 2024 gold withdrawals from the Shanghai Gold Exchange (SGE) were well below their ten-year average, according to Ray Jia, Research Head, China at the World Gold Council (WGC).

In the latest WGC China update, Jia pointed to the sharp divergence of Chinese and international price benchmarks in December.

“The gold price in USD fell by 2% while the SHAUPM in RMB saw a mild gain of 0.1% – due to a 1% depreciation of the local currency against the dollar,” he said. “In general, rising US Treasury yields and the strengthening dollar – driven by changing expectations of the Fed’s future rate path – outpaced support from rising geopolitical risks, higher inflation expectations and improved market momentum.”

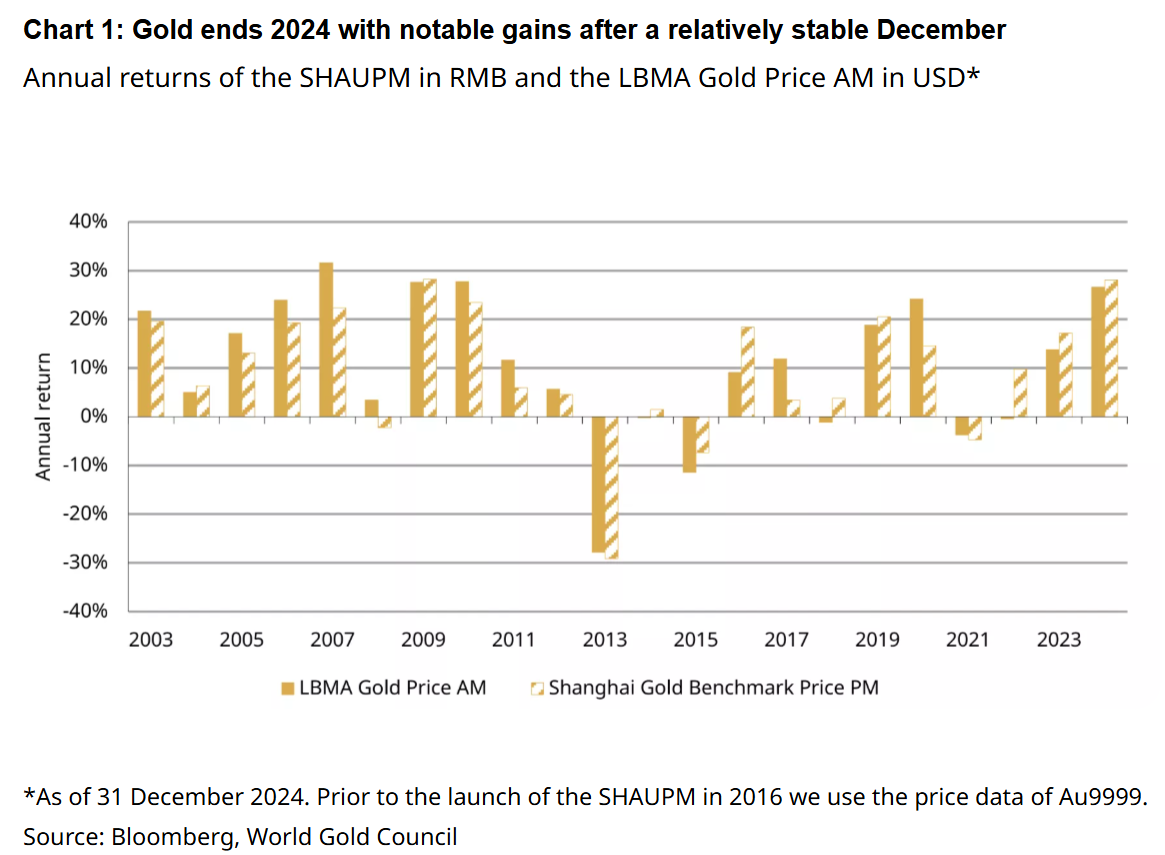

He noted that 2024 was a strong year for gold by any metric, with the RMB gold price gaining 28%, its best performance since 2009, while gold priced in USD saw its largest gain (27%) since 2010.

“Spiking geopolitical risks around the globe and continued central bank gold purchases were main drivers of the international gold price,” Jia said. “And a weakening Chinese yuan against the dollar, we believe, bolstered the RMB gold price further.”

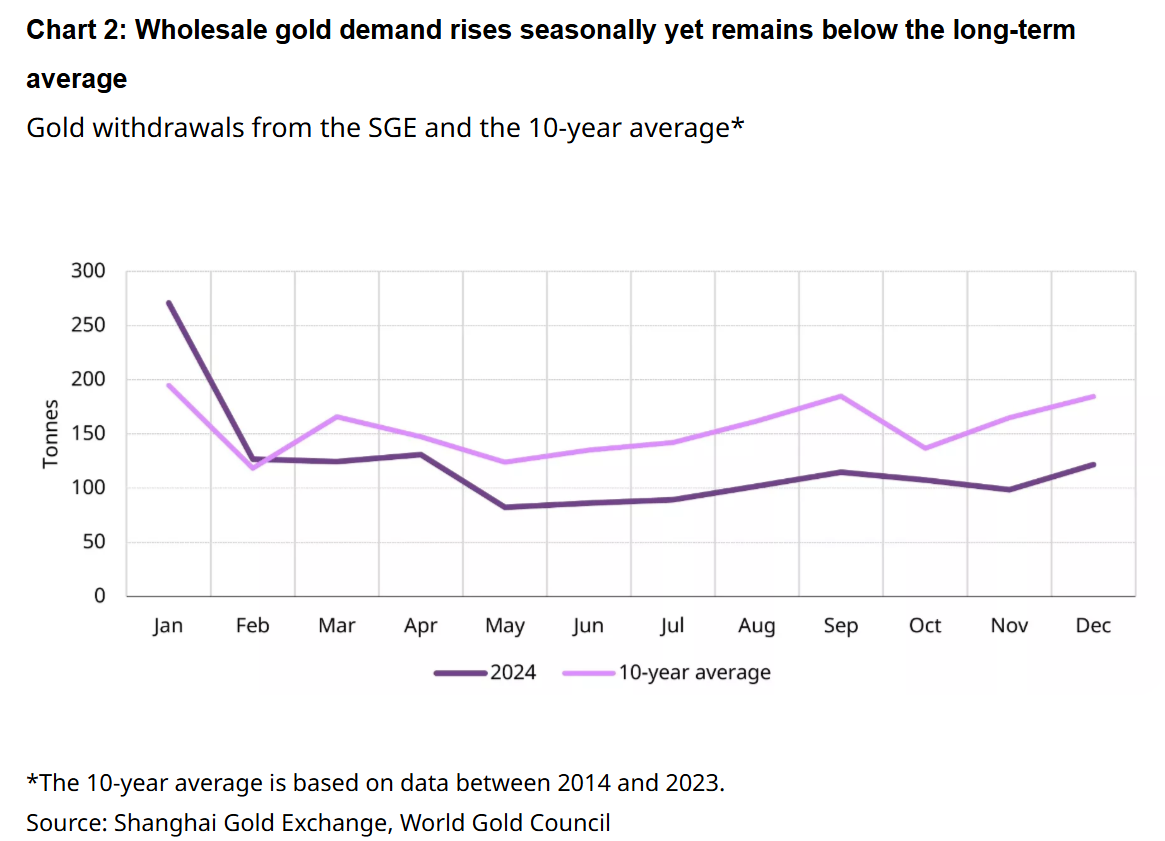

But despite a rebound in December, wholesale market in China delivered a subpar performance in 2024.

“China’s wholesale gold demand improved during the last month of the year,” he said. “Total gold withdrawals from the SGE rose to 122t in December, up 24% on November. And the Shanghai–London gold price spread turned positive again towards the end of 2024 thanks to improving demand.”

“This is in line with our observations in Shenzhen, China’s gold jewellery manufacturing hub: wholesalers and manufacturers told us that their showrooms were busier in December as retailers stocked up for the anticipated year-end sales boom,” Jua added. “But they also mentioned that while there was a seasonal pick-up m/m, their sales remained below previous years. This is reflected in the 26% y/y fall in total gold withdrawals from the SGE, which were 34% lower than their 10-year average.”

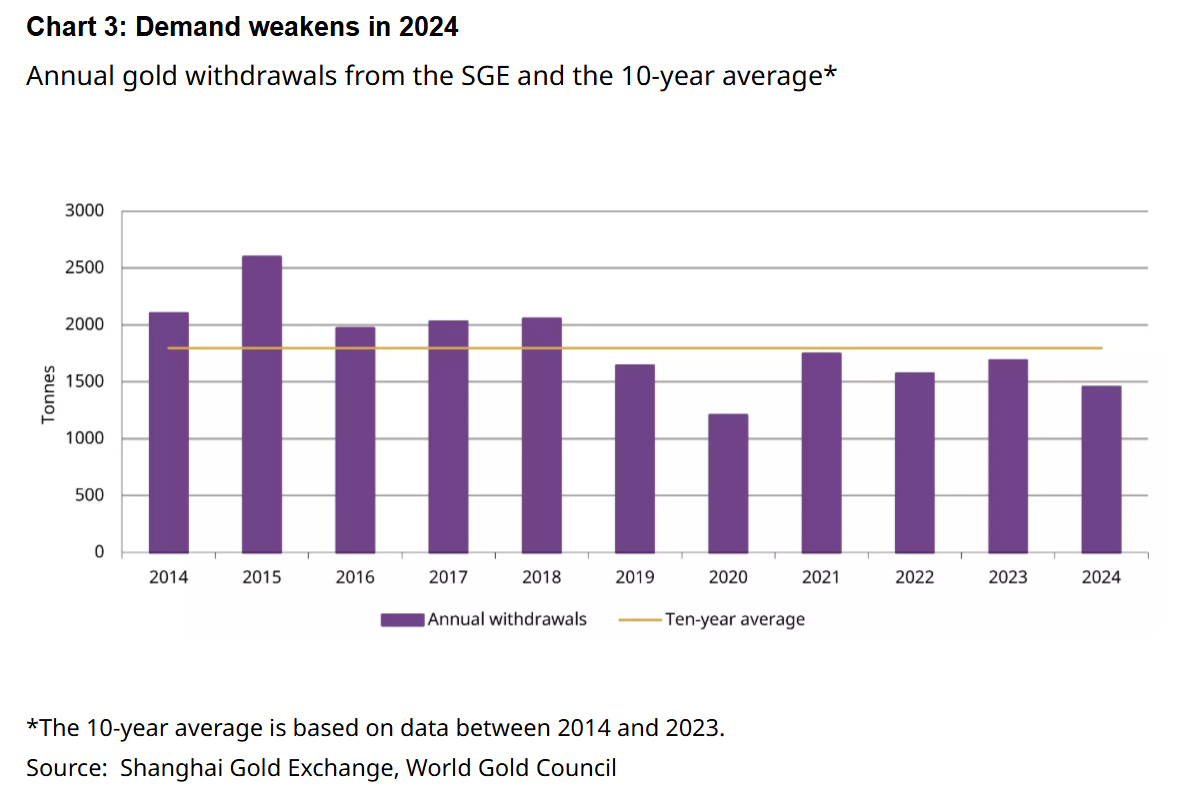

Following a strong start in 2024, Chinese gold demand was relatively soft from February onwards.

“Banks, refiners and jewellery manufacturers withdrew a combined 1,455t of gold from the SGE, 15% less than in 2023 and 22% lower than the 10-year average,” he noted. “This is mainly due to a notable weakness in gold jewellery consumption – the major component of China’s gold demand – as the surging gold price and concerns of an economic slowdown limited affordability for consumers. But the same factors, alongside a weakening currency, proved supportive for investment buying, and this partially countered jewellery’s decline.”

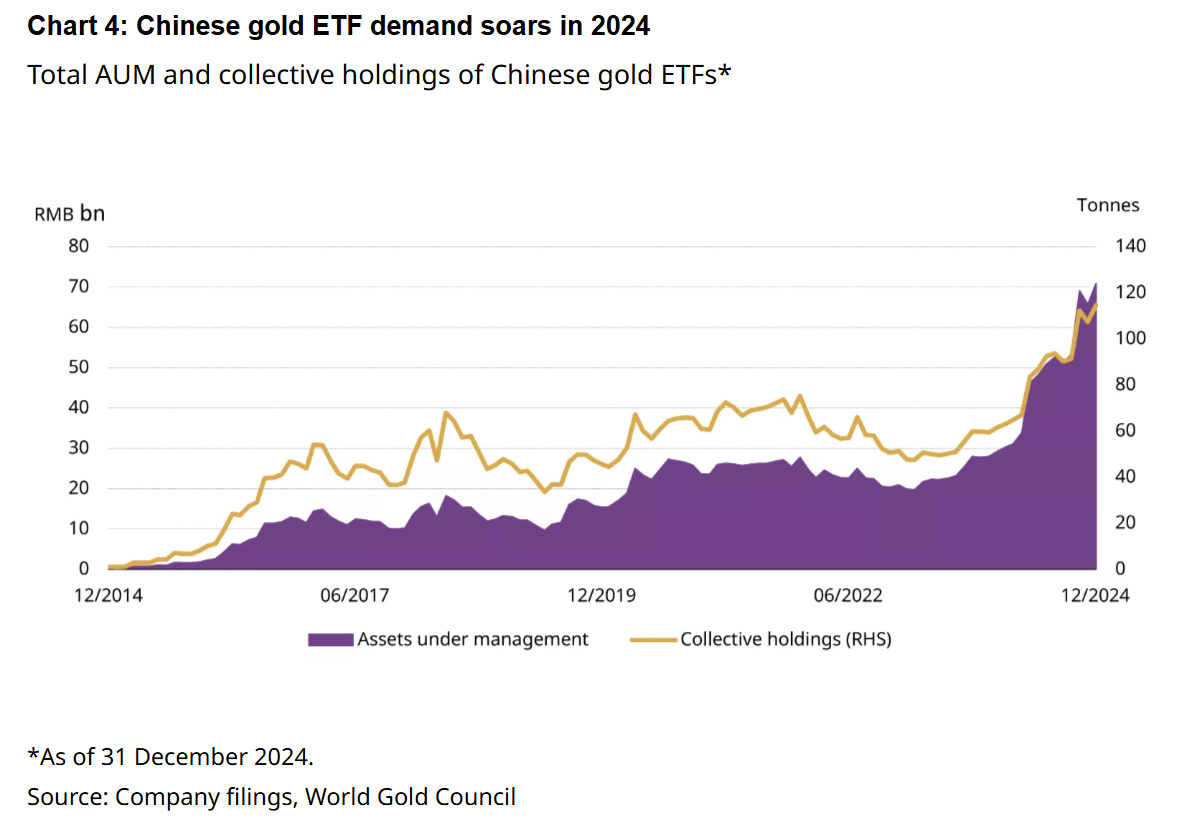

But Chinese gold ETFs were extremely strong, with holdings reaching another record high last year.

“Chinese gold ETFs added RMB4.5bn (US$635mn) in December, pushing the total AUM to RMB71bn (US$9.7bn), the highest on record; holdings also reached a record level of 115t, a 7.5t increase during the month,” Jia wrote. “Although the local equity market experienced another monthly gain, the depreciating RMB and plummeting government bond yields – amid economic uncertainties and intensifying expectations of continued rate cuts – drove investors to gold. The announcement from the PBoC that gold purchases had resumed also likely boosted investor interest.”

“Investor demand for gold ETFs jumped in 2024, attracting RMB31bn (US$4.4bn), the strongest on record,” he added. “The total AUM of Chinese gold ETFs surged by 150% during the year, while holdings soared by 87%, or 53t.”

Jia pointed to three key factors that drove ETF demand in 2024 “The strong gold price performance which attracted investor attention,” as well as “Plunging government bond yields which reflected expectations of continued rate cuts and rising safe-haven demand as the future of China’s economy remains shaky to many.” The third factor was “A weakening local currency which pushed up value-preserving demand.”

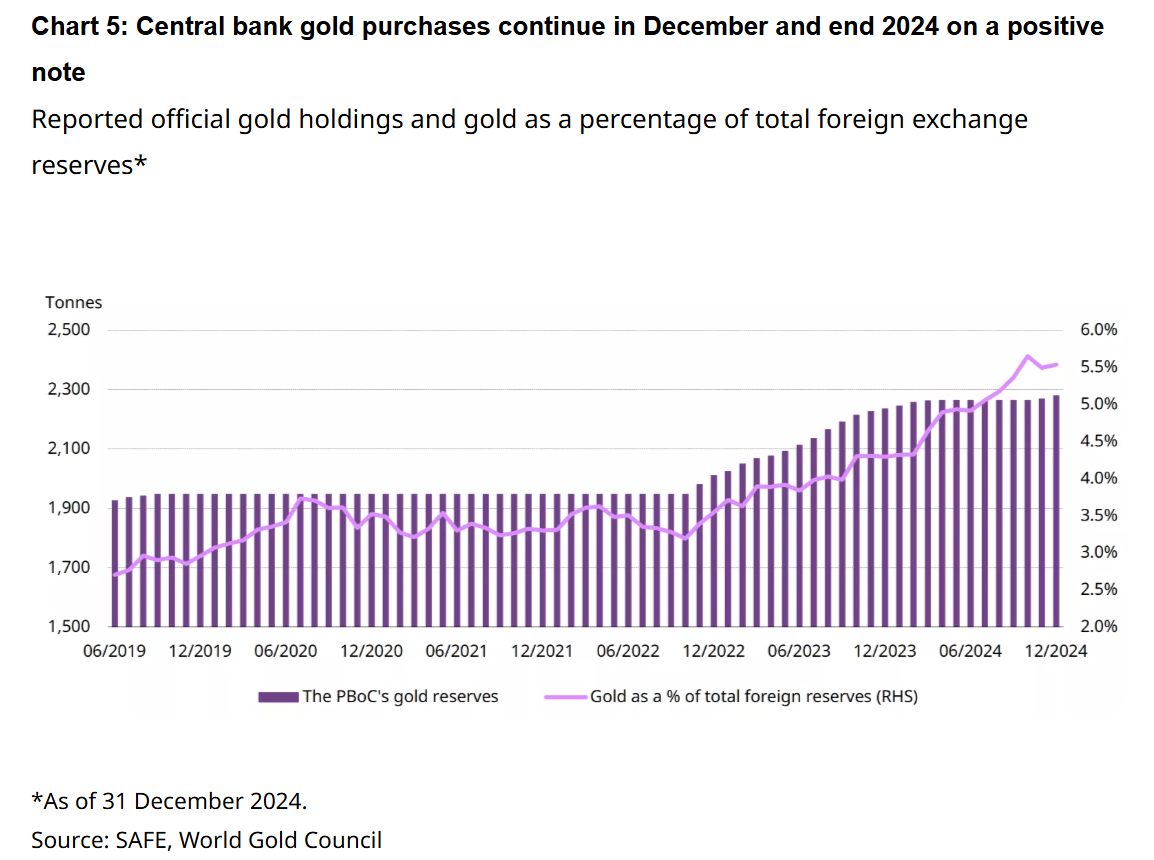

Sovereign demand was also reignited at the end of the year, with China’s central bank announcing gold purchases two months in a row.

“The PBoC moved again, reporting a 10t gold purchase in December following November’s 5t addition,” he said. “China’s official gold holdings now stand at 2,280t, accounting for 5.5% of total foreign reserves, a record high.”

Jia noted that the PBoC ran hot and cold on gold in 2024. “[A]fter kicking off the year with four consecutive monthly purchases, no activity was reported between May and October,” he said. “Over the course of the year, China reported 44t of gold purchases, the lowest since 2022 when the central bank resumed its gold buying announcements.”

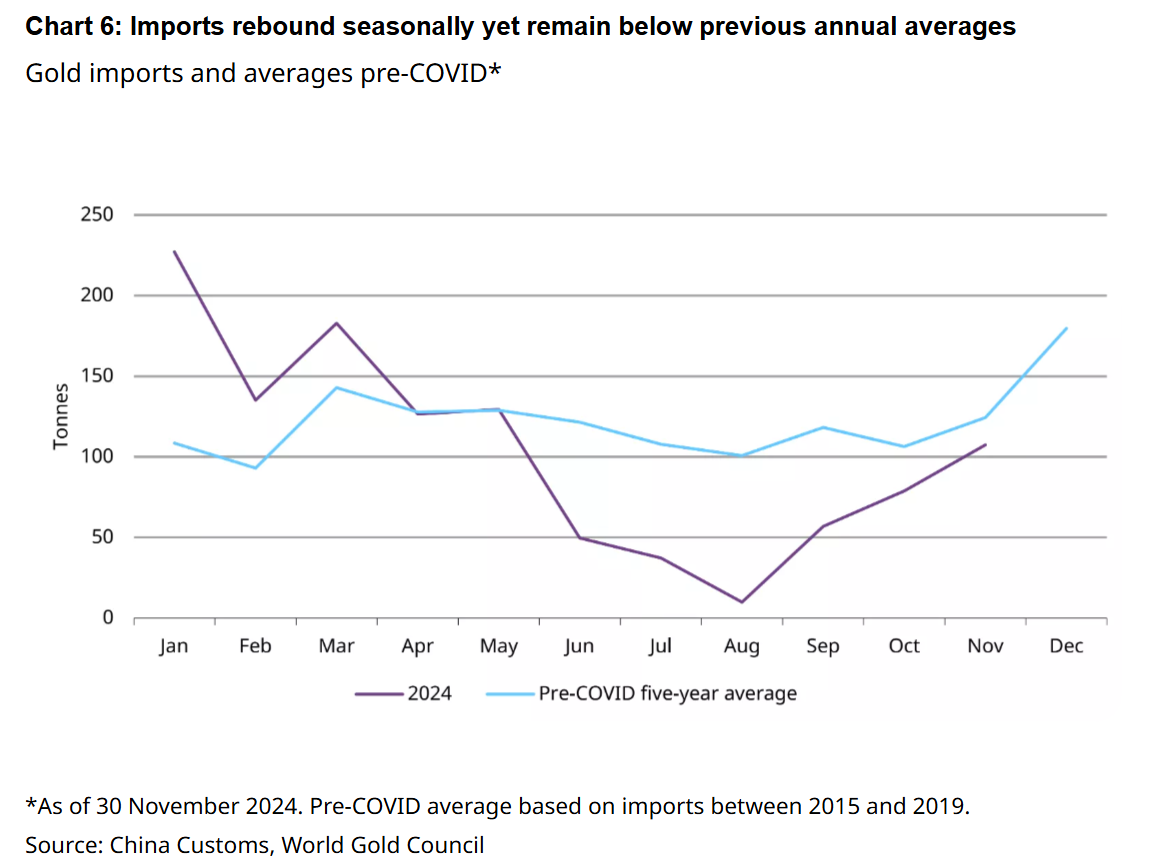

Gold imports, meanwhile, followed their usual seasonal trend higher into the end of the year, but WGC data showed that high prices had an impact on imports.

“Following another m/m rise in October (+39%), November imports increased by a further 36%, totalling 108t,” he wrote. “We believe this is seasonal, given China’s gold demand tends to rise ahead of the Chinese New Year holiday in late January or early February. However, due to subpar wholesale gold demand, imports were below their pre-COVID five-year average (124t) and 23% lower y/y.”

Looking ahead, Jia said the World Gold Council expects the peak buying season through the Chinese New Year holiday – which runs from Jan. 28 to Feb. 4 this year – to boost gold jewelry consumption.

“Investment buying is likely to continue to draw support from falling government bond yields and a weak local currency – driven by intensifying expectations of more rate cuts to boost the economy and concerns around rising US tariffs,” he said.