(Kitco News) – While the recent conflict in the Middle East has increased gold’s short-term price volatility, the medium-to-long term outlook remains constructive as elevated geopolitical risk, rising fiscal deficits and continued central bank buying will support higher prices, according to Rodolphe Bohn, FX and Commodities Strategist at HSBC.

Bohn noted that gold has had a volatile start to 2026, with prices falling from $5,415 per ounce in late January to $4,400 by March 26 as the conflict with Iran escalated.

“During this risk-off phase, oil prices surged, the US dollar strengthened as the market’s preferred safe-haven assets, yields rose, and equities fell,” he wrote. “Gold did not act as a straightforward ‘geopolitical hedge’, as investors sold bullion to raise liquidity while the US dollar absorbed most of the safe-haven demand.”

“However, the recent ceasefire has shown that gold can rebound quickly as market stabilise.”

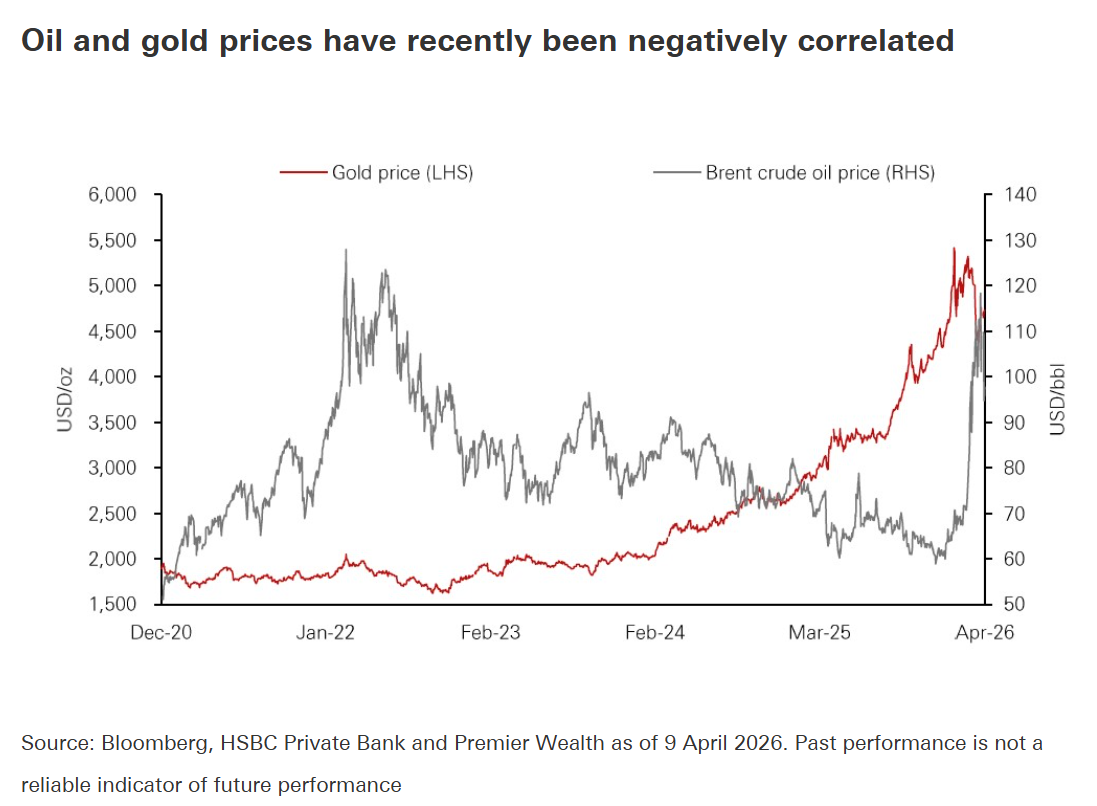

Bohn said the relationship between gold and oil prices is dynamic, and it and can shift depending on the nature of the shock. “Although there was a clear positive correlation between the two commodities leading up to the conflict, the relationship quickly neutralised as oil and gold prices moved in opposite directions,” he said. “When the US dollar rallies, it usually puts pressure on both gold and oil, but the Middle East supply shock pushed oil prices higher even as the US dollar rally weighed on gold. In the current market environment, a strong rise in oil prices does not necessarily trigger the same dynamics in gold prices.”

Bohn said monetary policy remains critical to the yellow metal’s future direction, and while HSBC isn’t counting on a boost from rate cuts, stubborn inflation and rising threats to growth will be supportive.

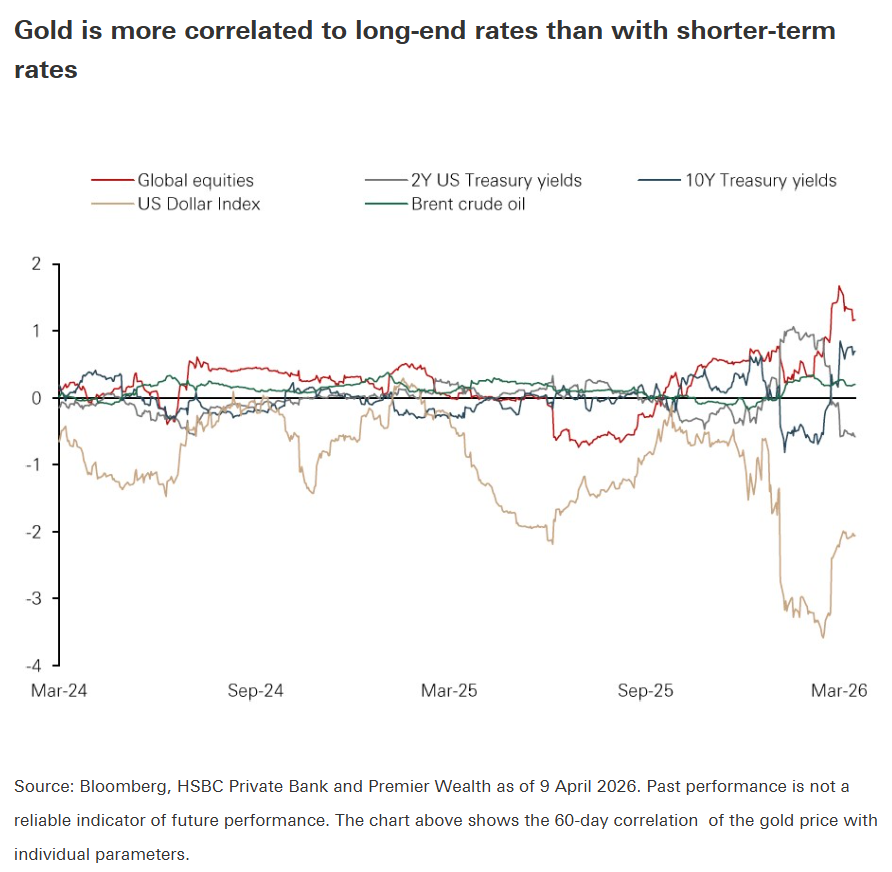

“High real yields can be a headwind for gold as it offers no yield,” he noted. “Long-end rates have mattered more since the conflict began, as they have moved alongside a stronger US dollar, weaker equities, and higher oil prices. Although we still expect Fed policy rates to remain unchanged through 2026 and 2027, which could limit gold’s upside, stagflation risks should continue to support demand for gold.”

Meanwhile, HSBC sees ongoing fiscal dynamics and central bank demand providing longer-term support for gold prices.

“Rising deficits and debt levels in the US and other countries are encouraging demand for hard assets, especially when investors are concerned about financial stability and policy flexibility,” Bohn said. “IMF estimates put US debt close to 100% of GDP in 2025, and higher defence spending globally is adding to debt burdens. These developments are unlikely to reverse in the medium term, providing support for gold prices in the longer run.”

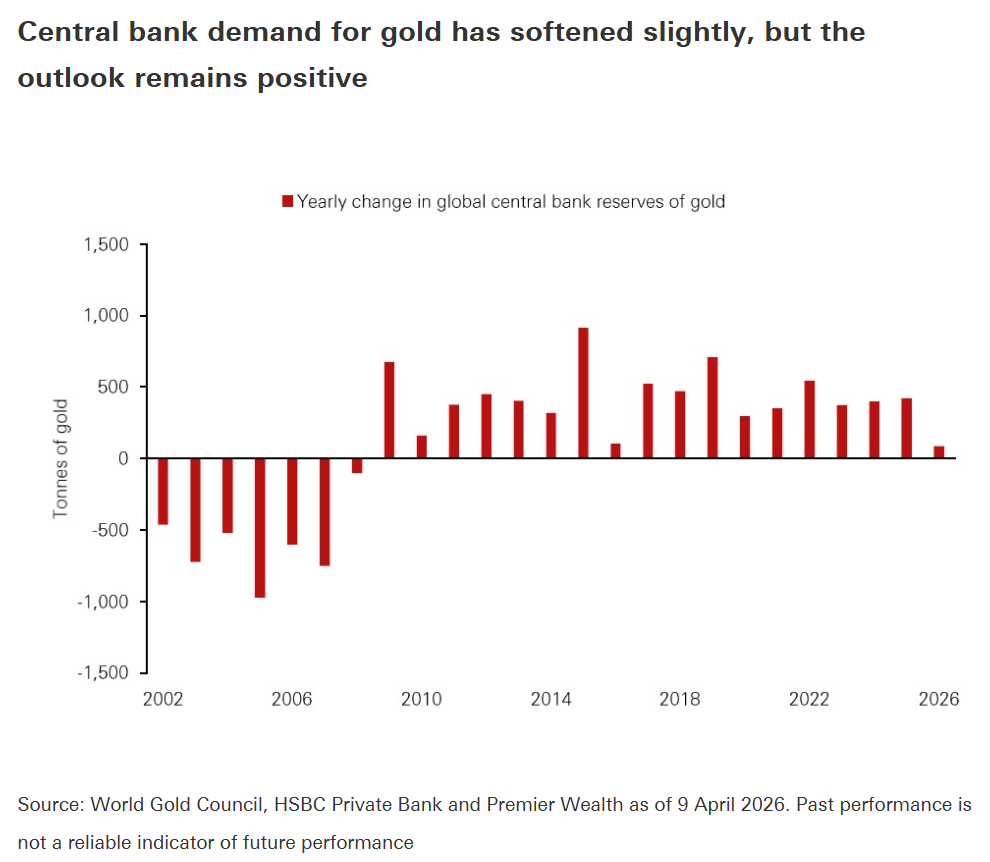

“Central bank demand has cooled from the peaks seen between 2022 and 2024, and some central banks have sold gold to preserve FX reserves amid higher energy import bills and defence spending,” he noted. “Even so, Central banks demand should improve later in the year as long-term diversification policies reassert themselves.”

Beyond investment demand, Bohn also noted that high gold prices are reshaping physical supply and demand, with jewelry demand particularly hard-hit. “Demand for coins also remains weak, while institutional demand for large bars has been firmer, supported by regulatory changes in markets such as India and China,” he said. “On the supply side, mine output is set to rise modestly in 2026–27, and recycling should increase as high prices mobilise more scrap into the market.”

“These shifts leave more bullion for investors to absorb,” he warned. “If investment demand stays weak for an extended period, that additional supply can cap rallies. Nonetheless, retail investors’ demand has recently become more significant for gold prices.”

“The near-term direction for gold depends on broader de-escalation in the Middle East: a ceasefire that persists or evolves into a complete cessation of hostilities in the region, the formal reopening of the Strait of Hormuz, and oil prices stabilising at lower levels,” Bohn concluded. “Such conditions would reduce financial stress, ease inflation fears, and support lower yields.”

“We maintain a bullish view on gold over the medium-to-long term.”