(Kitco News) – Commodities have a proven track record as a hedge against inflation, and gold may be the ideal investment given the likely post-election policies in the U.S., according to a new report from Goldman Sachs Research.

“Investors are alert to US inflation risks as corporate earnings exceed expectations, the US persistently runs large budget deficits, and because of the opportunity for inflationary policies following the presidential election in November,” Goldman Sachs analysts wrote in a post published Wednesday. “Commodities have demonstrated strong resilience in the face of inflation and have been a critical hedge for bonds and equities when prices and wages are climbing.”

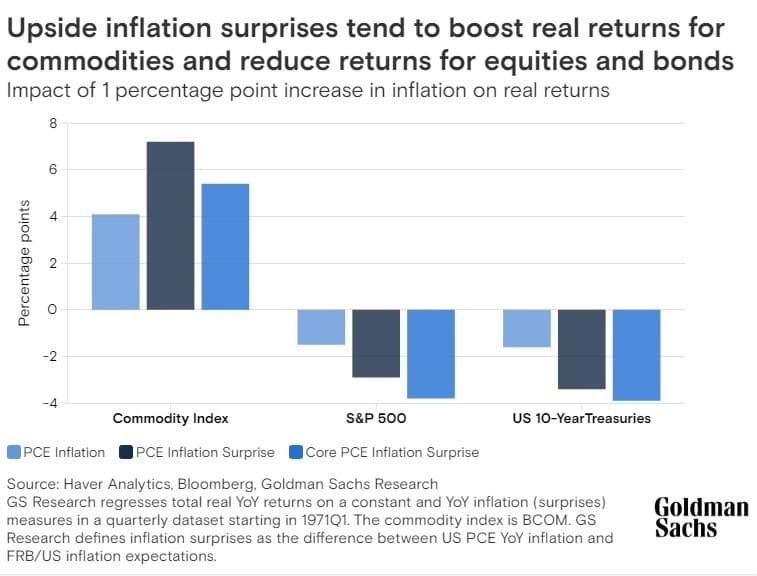

The report’s authors, head of oil research Daan Struyven and analyst Lina Thomas, found that “[a] 1 percentage point surprise increase in US inflation has, on average, led to a real (inflation adjusted) return gain of 7 percentage points for commodities, while that same trigger caused stocks and bonds to decline 3 and 4 percentage points, respectively.”

The Goldman Sachs Research team found that “commodities provide a direct hedge against negative commodity supply shocks, which tend to depress bond and stock returns as interest rates rise, as well as providing a hedge against lower stock returns as rising prices cause GDP growth to slow,” they said. “Commodities also tend to rally when inflation is boosted by economic growth, and they can provide wealth preservation when central bank credibility declines.”

The Goldman researchers examined five of the most inflationary periods over the past half century: “the oil embargo of the early 1970s, the Iranian Revolution later that decade, China’s economic boom in 2005, its late-cycle boom in 2007-2008, and the post pandemic recovery that began in 2021,” and noted that each period was marked by supply, demand, and/or growth shocks.

“Despite the different make-up in inflation drivers, commodities outperformed equities and bonds across all five episodes,” Struyven and Thomas wrote. And the results were the same with inflation surprises exceeding one percent.

However, the report noted that not all commodities responded the same way to each type of inflationary shock.

For example, gold “typically only guards against very high inflation and large inflation surprises caused by losses in central bank credibility and geopolitical supply shocks,” but the authors said that the yellow metal “usually didn’t perform well in response to positive demand shocks when the central bank responded swiftly by hiking rates.”

Energy commodities generated the strongest real returns across assets amid upside inflation surprises. “That’s because energy usually responded both to supply and demand shocks,” they said. “While refined oil products remain the most important commodity for global consumer prices, recent episodes have shown that natural gas has significant inflation hedging benefits as well.”

Agricultural commodities performed well in multiple scenarios. “Like energy, agriculture and livestock have provided similar inflation protection, as agriculture prices typically rose in response to negative energy supply shocks and could also rise during positive demand shocks,” the researchers found.

And industrial metals saw outsized gains in some situations, but not in high-interest-rate environments. “Given their large exposure to cyclical manufacturing and the housing sector, industrial metals have demonstrated they could offer protection against demand-led inflation,” they said. “Industrial metals generated especially high returns (average total real returns of 30%) late in the cycle when economy-wide inflation risks are the largest.”

“One caveat is that the average real return for industrial metals has been only modestly positive when inflation surprises have been in the top 20% of history,” they warned, “probably because of their greater sensitivity to interest rate hikes.”

Goldman Sachs Research then turned their attention to the potential economic impact of the U.S. election in November. “Goldman Sachs Research’s US economists and cross-asset strategists expect that a unified government is more likely to see larger fiscal deficits, large shifts in fiscal policy, and downward pressure on bond returns than a divided government,” they said.

“A sweep by Democrats could lead to significant increases in corporate taxes, which, along with tariff increases, could be negative for stocks,” they wrote. “There may be higher inflation risks, and more risks to bond returns, under a Republican sweep amid, on the supply side, higher tariffs, slower immigration, and tighter sanctions on Iranian oil. On the demand side, lower taxes and stronger attempts to influence Fed policy may push up inflation.”

Goldman said the biggest swing factor will be the market reaction to geopolitical shocks, including tariffs. And based on their research, the yellow metal looks to be the best hedge against the likely combination of geopolitical risks and inflationary pressures.

“Gold emerged as the best commodity to serve as a potential hedge against inflation and geo-political risks,” they wrote. “Goldman Sachs Research’s base case is that gold appreciates to $2,700/troy ounce by year-end, an increase of about 16%, on solid demand from central banks in emerging markets and from Asian households. Gold could help shield against potential stock market drops if a trade war erupts, and it has upside if concerns mount about the US debt load or if the Fed is subordinated by a new administration.”

“Goldman Sachs Research also sees opportunity in oil as a geopolitical/inflation hedge,” they added, “both because of its strong historical record as a broad inflation hedge and because there’s potential for a hawkish shift in US policy against some major oil-producing countries.”