(Kitco News) – The gold market is overbought according to several key metrics, and while platinum prices may be carving out a bottom, the same cannot be said for copper, according to Daniel Ghali, senior commodity strategist at TD Securities.

“I absolutely think there's risk,” Ghali said of $2,500 gold in an interview with BNN Bloomberg late Wednesday afternoon. “The setup today in gold markets, any way you slice, it is just not the same as it was a few months ago.”

Ghali said that heading into 2024, there was a historic dislocation between money-manager positioning in gold and the market’s rate expectations.

“That's really what, in our opinion, kicked off the rally in gold markets,” he said. “They were historically under-positioned, and that was curious, heading into what was widely expected to be the first year of a rate-cutting cycle. The rally was then extended by very significant buying activity in physical markets.”

But Ghali said the situation in the gold market has shifted dramatically since that time.

“When you fast forward to today, money manager positioning isn't just bloated, it is at historical maximum levels,” he said. “We're talking about the same levels that marked very significant local highs around the Brexit referendum in 2016, around the ‘stealth QE’ narrative in 2019, around the same levels that it was during the peak of the Covid crisis in March of 2020.”

“In our view, so many of these bullish narratives that are being discounted by investors have already been baked into the cake,” he added.

“And at the same time, physical markets are completely different than they were a few months ago,” Ghali said. “There is a buyer’s strike in Asia. Mind you, most of that buying activity was actually probably related to a currency depreciation hedge, to retail investors in part looking to diversify their wealth at a moment in time when property markets were crashing in China, stock markets were crashing, bond markets weren't necessarily seen as a good investment, so there really wasn't any other alternative than to move your capital into gold.”

Ghali said that the outlook that markets are pricing in today is totally different. “We are talking about a soft landing that's underscored by a pretty aggressive rate-cutting cycle,” he noted. “Capital should move from areas where it's least productive to most productive, so if the market is right about this global macro expectation, then you would actually expect capital to move to more productive uses, and that's just inconsistent with what is currently priced into gold.”

Asked if Chinese real estate prices are still pushing investors into gold today, Ghali said that no longer appears to be the case.

“In a very large way it did, earlier this year,” he said. “That being said, when we track Chinese flows in particular, whether it be into Chinese gold ETFs or even in physical markets, there really isn't any sign of buying activity from that region. And it's not only a China story, it’s also a Japan story. The currency depreciation pressure that Japan was facing earlier this year, was also a catalyst for retail investors to look for safe havens for their wealth.”

The sharp appreciation of the Yen and the concurrent unwinding of the carry trade have removed this support from the gold market as well.

Asked what price he would be looking to buy back into gold, Ghali said he’d be targeting a significant drop from current levels.

“We think a price closer to $2,300 is reasonable relative to the historic analogies that we spoke about,” he said. “Moments in time where positioning is as stretched as it is today have historically resulted in a 7% to 10% drawdown, so that seems reasonable to us.”

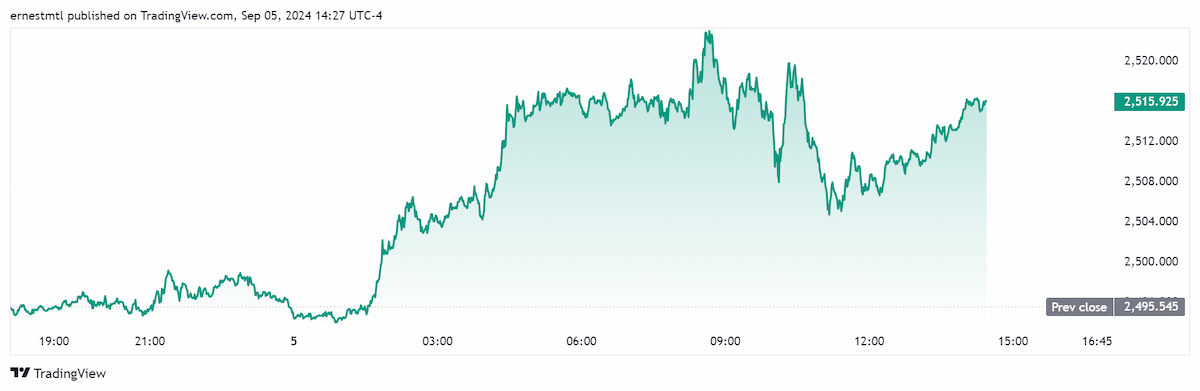

Spot gold once again climbed above the $2,500 level during the Asian session before going on a tear in European and North American trading, topping out at a session high of $2,523.52 per ounce just after 8:30 am Eastern. It last traded at $2515.92 per ounce, and is up 0.82% on the day.

Turning to the platinum market, Ghali said that algorithmic traders have come to dominate there, and he sees evidence that prices are carving out a bottom.

“We think that we could be in the process of forming a local low,” he said. “What we think is really the main driver behind platinum prices over the last few months has been the ebbs and flows in algorithmic trader positioning.”

“This is a market that is very useful when it comes to autocatalyst fabrication, it's very tied to the auto industry for example,” Ghali added. “In recent years, the chemical industry was a big consumer as well. But more recently, jewelry has actually been a trend, particularly in Asia. The variations in those components of demand that we spoke about, which is really where platinum metal is utilized, are substantially smaller than the variations in speculative flows, so algorithmic traders have actually now become the dominant speculative cohort in platinum markets, and other commodity markets as well.”

“We think that we're seeing signs of selling exhaustion from that cohort,” he said. “Even more so, we think that in most scenarios for prices, they would be set to buy over the near term, so this is a setup that could be suggesting that prices are starting to find a base.”

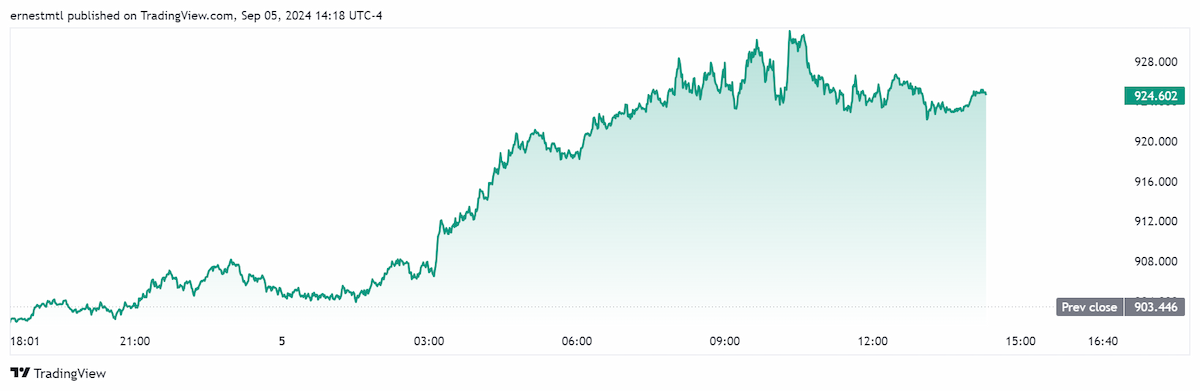

Platinum does appear to have found support, and it saw a nice rally on Wednesday, with spot platinum last trading at $924.602 per ounce for a gain of up 2.34% on the daily chart.

Asked if he would be interested in buying copper at current price levels, Ghali said no.

“Copper is a very interesting one, it's a market that is actually giving some signs of global recession,” he said. “The demand side is really what's concerning there. What most of the market expected earlier this year was that supply-side scarcities would finally be met. We're not seeing any sign of that. In fact, we're seeing larger surpluses over the next few years, so there's very few reasons to be long copper based on that view.”

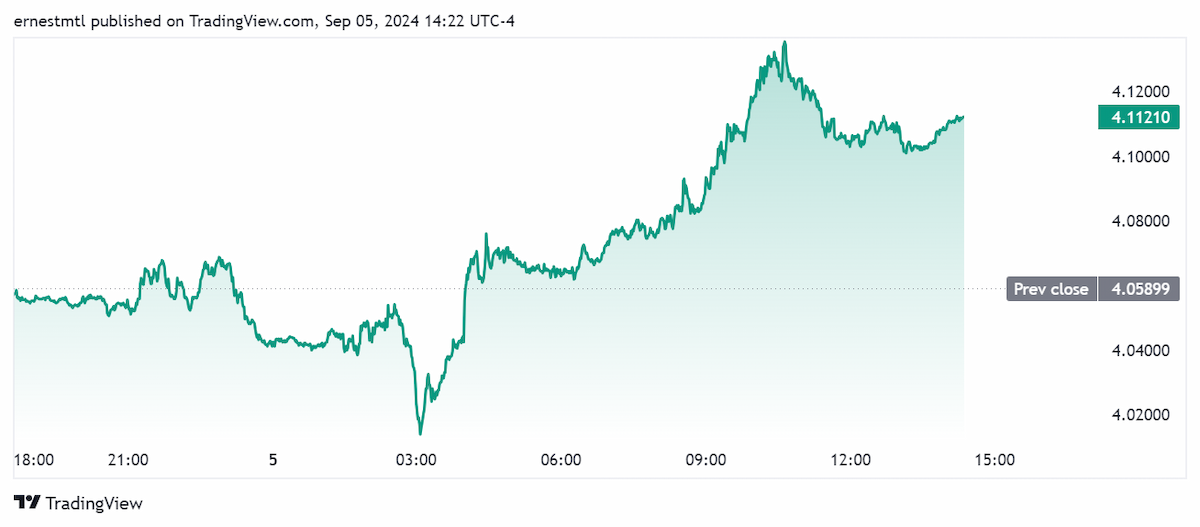

Copper prices have also received a bit of a boost, with CFDs on Copper last trading at $4.112 per pound for a 1.31% gain at the time of writing.