(Kitco News) – After a standout 12-month performance that has seen gold prices rise by nearly 42%, investors would do well to revisit the gold investment thesis, according to Columbia Business School professor and QuantStreet Capital partner Harry Mamaysky.

In a recent analysis for VettaFi, Mamaysky noted that since the Fed began its monetary easing cycle, cutting its interest rate target by 1%, gold has done what it typically does: post gains.

“[G]old (as represented by the iShares Gold Trust (IAU)) has been one of the best-performing asset classes, with gains outstripping those of the S&P 500 index (SPX), Treasuries (represented by the Vanguard Intermediate-Term Treasury ETF (VGIT)), the Nasdaq-100 Index (represented by the Invesco QQQ Trust (QQQ)), bitcoin, and global stocks ex-U.S. (represented by the Vanguard Total International Stock ETF (VXUS)),” he wrote.

Mamaysky said that much of gold’s recent strength is due to the uncertainty caused by the Trump administration’s trade policy. “Since President Trump’s April 2 'Liberation Day' tariff announcement, gold is up 6.2%, while U.S. stocks are down close to 7%, and international stocks and bitcoin are down around 2%,” he said.

Mamaysky then lists a number of factors that have helped drive gold prices higher, and that support the investment case for holding gold going forward.

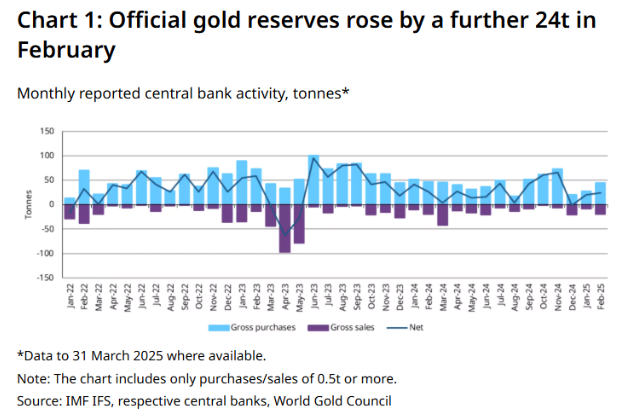

The first of these is persistent buying by central banks around the globe. “[C]entral banks have been net buyers of gold for the last several years, a trend that might accelerate given recent market turmoil caused by trade uncertainty,” he said.

Gold’s effectiveness as a hedge against market and economic uncertainty is shown through two statistical measures.

“Gold’s daily price changes have very low correlations with price changes of other asset classes,” Mamaysky wrote. “For example, over the last year, the correlation of daily gold and S&P 500 returns has been 21%, whereas the correlation of bitcoin and S&P 500 returns has been 46%. This low correlation means gold is a diversifying influence in investor portfolios.”

Gold also tends to do well in 12-month periods where the overall market performs poorly. “In 1-in-20 bad 12-month return periods for the S&P 500 — when the S&P 500 is down 25% on average — gold’s average return has been a positive 2%,” he noted

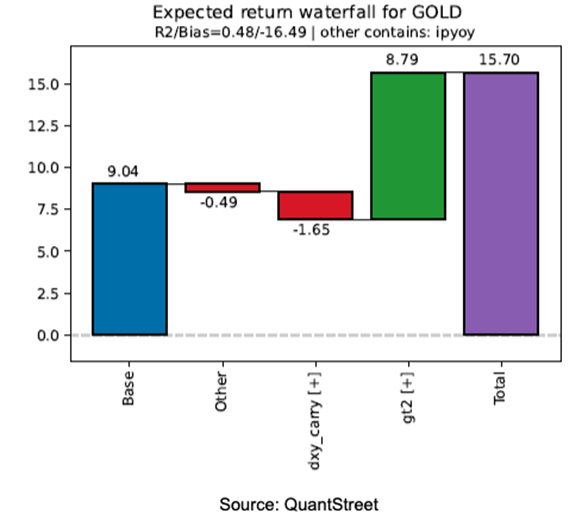

Mamaysky said that QuantStreet’s machine learning forecasting model is bullish on gold. “The model identifies several forecasting variables for each tracked asset class,” he said. “For gold, the model identifies the U.S.’ versus Germany’s interest rate differential (dxy_carry) and the level of two-year Treasury yields (gt2) in the U.S. as important forecasting variables. The currently elevated — relative to its history in the model training window — level of two-year yields generates a high one-year ahead return forecast.”

Another element that supports the gold investment thesis is QuantStreet’s gold forecasting model, “which has good out-of-sample forecasting properties, as seen by its out-of-sample R-squared (a measure of the goodness of fit of future one-year return forecasts versus actual one-year ahead return outcomes) of 48%,” he said.

Mamaysky then outlines the elements that argue against gold investment in the current environment.

The first of these is its high rate of return over the past year. Mamaysky shared a chart that shows the price of front-month gold futures relative to CPI. “The gold-to-price-level ratio is at 9.77, which is an all-time high dating back to the mid-1970s,” he noted. “Last year, we also mentioned this elevated level as a concern for the gold thesis, though at that time the ratio was only at 6.77.”

“Another factor in favor of gold as a portfolio hedge is the gold-to-bitcoin ratio, which now stands at 0.039, quite a bit higher than last year’s ratio, but still well off recent highs established in late 2022,” he added.

“Several factors argue in favor of gold’s inclusion in investor portfolios, but the elevated valuation level of gold (relative to the inflation price index) argues for some caution,” Mamaysky concluded, adding that while QuantStreet continues to hold gold in their portfolios, “we regularly evaluate the investment thesis and other relative opportunities, and our holdings of gold may decrease or increase in the coming weeks and months.”