(Kitco News) - Although gold faces some near-term headwinds as elevated oil prices continue to drive inflation and interest rate expectations higher, one investment firm says it still sees a path for prices to push above $5,000 an ounce by year-end.

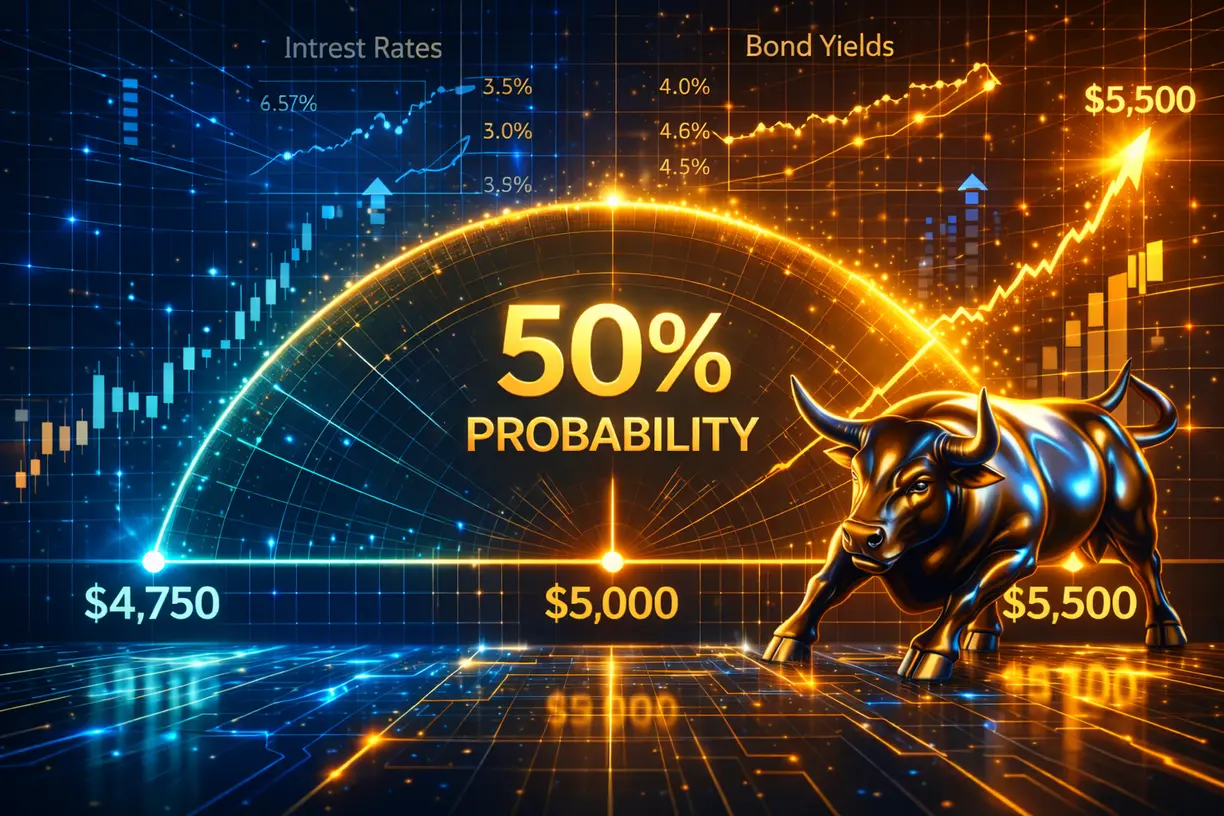

Commodity analysts at State Street Investment Management, led by Aakash Doshi, said they remain bullish on gold and continue to see a 50% chance that prices trade between $4,750 and $5,500 through the rest of the year.

At the same time, the investment firm has pared back its bullish expectations and now sees a firm level of support.

“We reduce odds of the US$5,500-6,250/oz bull case range from 35% to 30%, but think that US$4,000-4,100 will hold as a floor on the market and that ATHs could be re-tested into 2027. The bear case range of US$4,000-4,750, where trading ended March, is a 20% probability in our outlook,” the analysts said in their monthly report.

While State Street remains bullish on gold, the analysts note that its selloff last month and current consolidation are not surprising, given how sentiment in global financial markets has shifted because of the joint U.S.-Israel war against Iran.

The analysts noted that at the start of the new year, markets were pricing in 58 basis points of easing this year from the Federal Reserve; however, the chaos in the Middle East, which is creating significant supply-chain issues in the energy market, has dramatically shifted those expectations.

“In mid-late March, expectations for a Fed hike this year were at one point above 60%!,” the analysts said.

Currently, the CME FedWatch Tool sees a 71% chance that rates remain unchanged at current levels through year-end. Despite this neutral monetary policy stance, gold prices remain relatively resilient below $4,800 an ounce. Spot gold last traded at $4,774.20 an ounce, up more than 1% on the day.

Despite the headwinds, State Street said investors should continue to focus on broader long-term market trends rather than short-term interest rate expectations.

“The March correction in gold was largely a function of Fed re-pricing and higher real yields, which supported a stronger US$. It was probably not a breakdown of the global gold demand thesis driven by debasement concerns and allocations for alt-fiat. Investors should thus be cautious about cyclical pressures (opportunity cost of holding gold has temporarily increased with real yields) against structural dynamics (that, in our view, remain largely positive for gold),” the analysis said.

While higher oil prices will continue to drive inflation pressures higher, Doshi’s team warned that this environment is also a double-edged sword.

“While a prolonged conflict that sends ICE Brent prices north of US$150/bbl would likely weigh on gold through the Fed and dollar channel, it would also increase the odds of recession or stagflation. Meanwhile, oil prices normalizing to US$80-85/bbl could quickly send gold prices back above US$5,000/oz, in our view.”

Looking beyond U.S. monetary policy, State Street sees another long-term bullish factor for gold: the unsustainable rise in government debt. Highlighting estimates from the Congressional Budget Office, net interest payments on U.S. federal debt are forecast to exceed $1T this year for the first time on record. However, the U.S. is not alone in its growing debt problems.

“Rising deficits (war spending, higher interest expense, reduced revenue) reinforce a backdrop of elevated debt and long-term currency debasement risk, which historically boosts gold demand. Total global debt has grown to a record ~$348T, or 3-4x world GDP, rising most acutely across government, rather than private-sector, debt. This may foreshadow embedded fiscal pressures,” the analysts said.