(Kitco News) – Investors attempting to discern whether gold and silver prices have set their cyclical lows, and whether bond yields have already seen their medium-term highs, should look to monetary policy in the near term while watching fiscal policies over the longer term, according to Erik Norland, Managing Director and Chief Economist at CME Group.

In a recent analysis, Norland wrote that 2026 began with two very different narratives around inflation.

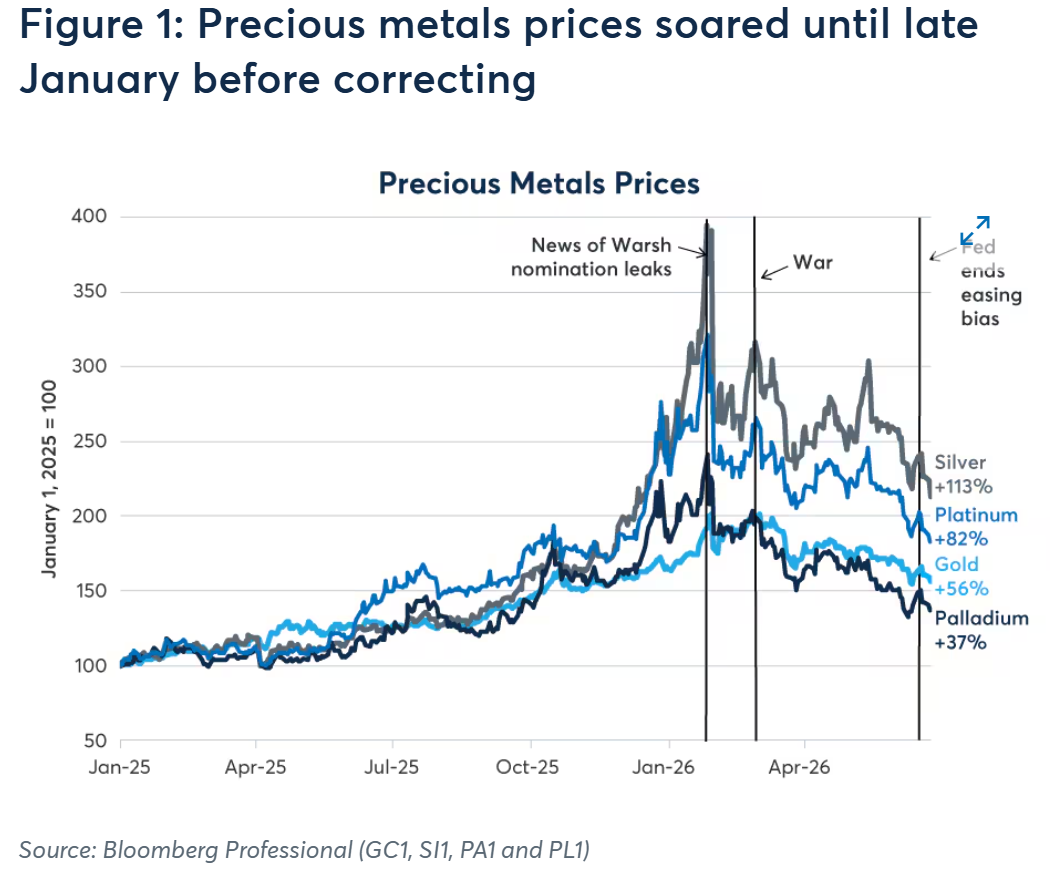

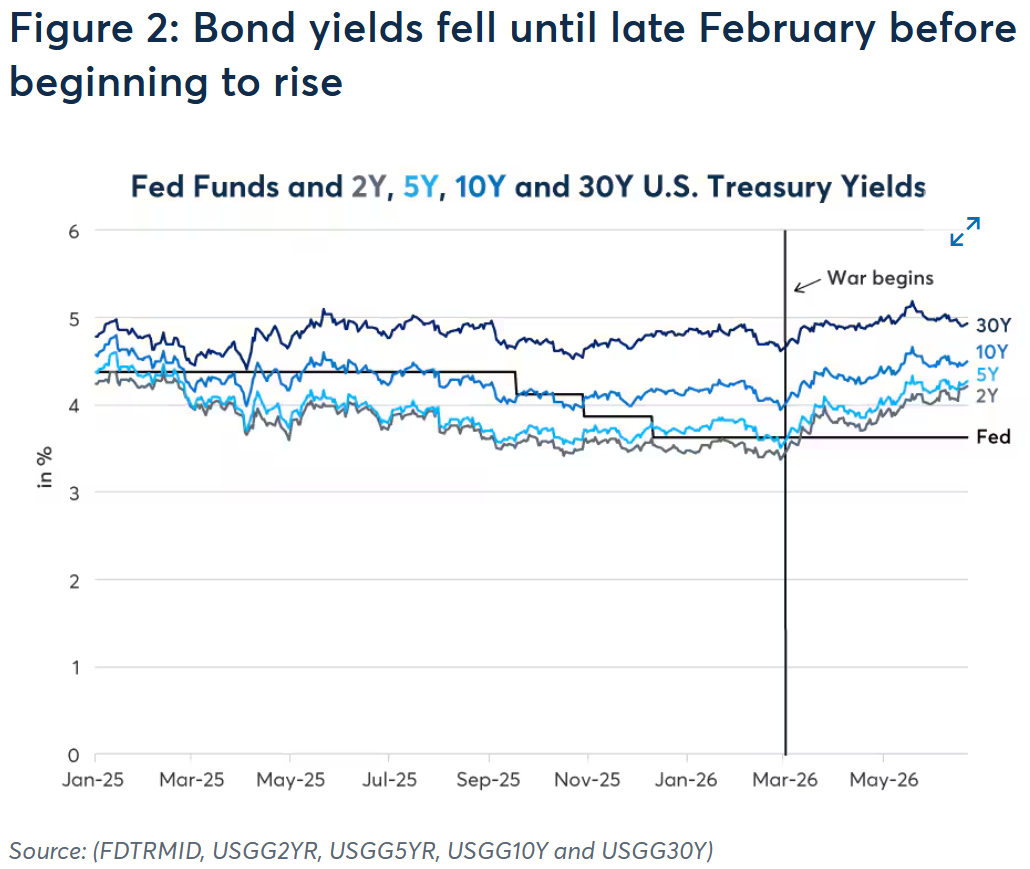

“On one hand, precious metals prices soared in 2025 through late January this year as investors braced for higher inflation, concerns over central bank independence and fiat-currency debasement,” he said. “Conversely, U.S. Treasury yields generally declined in 2025 and continued to drift lower into February 2026 as the market appeared to shrug off prospects of accelerating inflation.”

“The disconnect, however, came to an end in late January this year as a convergence of sentiment over sticky inflation led to a sharp decline in precious metals while U.S. Treasury yields began rising, especially at the shorter end of the yield curve.”

Norland then looked at what caused sentiment in these two markets to converge, and where they might be headed.

He said the run-up in precious metals prices appeared to have been based on three market narratives: Central bank independence might be eroding; Central banks cutting rates in 2024 and 2025 despite above-target inflation in most countries/currencies; and Expansionary fiscal policy and large budget deficits in the U.S. and elsewhere.

“In late January, the news of Kevin Warsh’s nomination to head the Federal Reserve (Fed) seemed to raise concerns that the Fed was at risk of losing its independence,” he said. “In 2011, Warsh resigned from the Federal Open Market Committee (FOMC) and began voicing his opposition to Quantitative Easing and holding rates near zero for extended periods. He didn’t seem like a policy maker intent on keeping the money printing press running. Indeed, in chairing his inaugural FOMC meeting in mid-June, Warsh’s Fed officially removed its easing bias.”

Norland noted that over the past five months, precious metals prices have declined sharply while remaining well above early 2025 levels, which suggests that while inflation concerns have eased, they remain present.

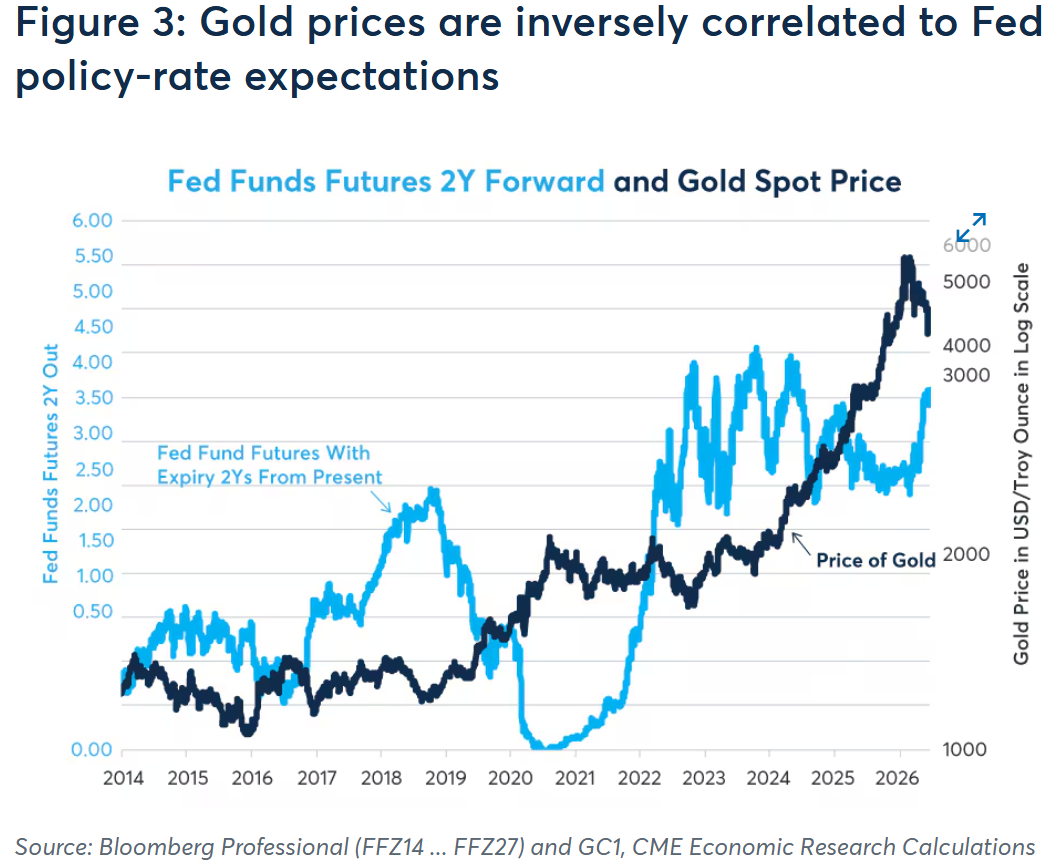

“Over the past few months, investors in Fed funds futures and SOFR futures have gone from pricing 50 basis points (bps) of rate cuts over the next two years to 50 bps of rate hikes,” he wrote. “Gold prices usually move inversely with rate expectations, rising in 2019 to mid-2020, and 2023 to early 2026 when rate expectations fell, and trading sideways when sentiment shifted to higher rates.”

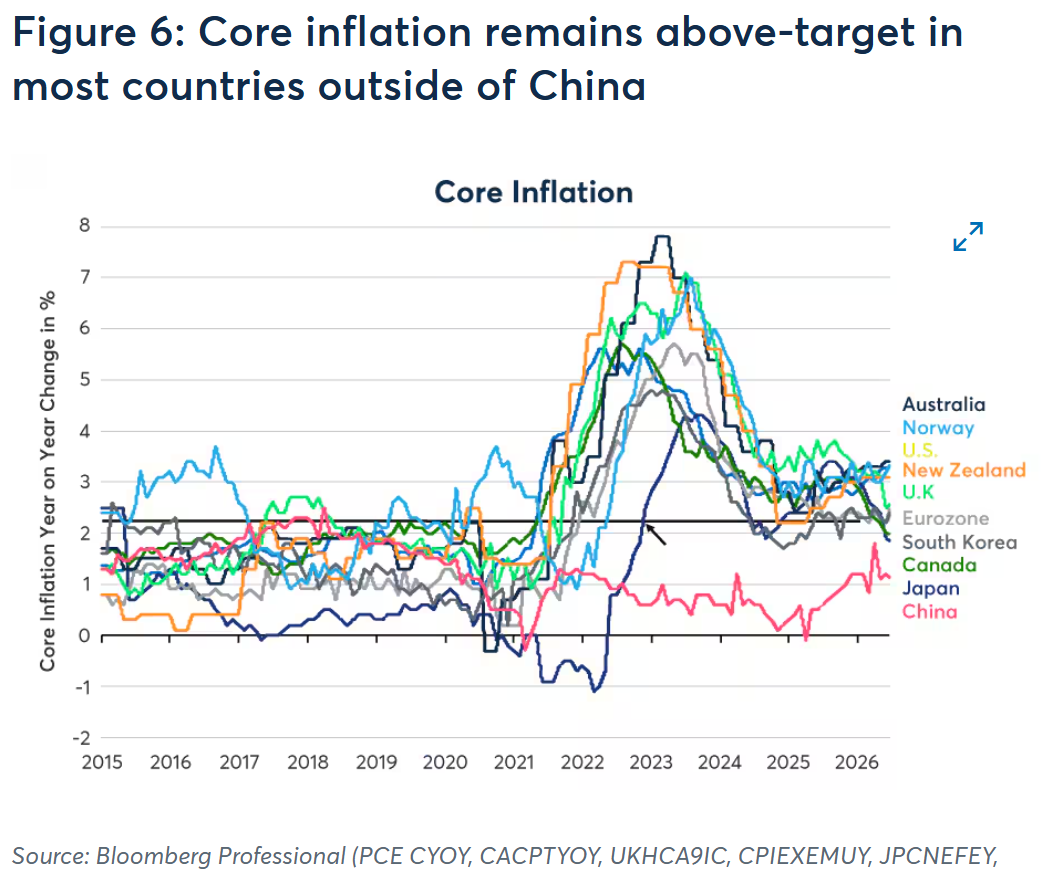

Norland said that, rising core inflation paradoxically contributed to pulling precious metals prices lower. “While precious metals are traditionally viewed as inflation hedges, accelerating inflation is sometimes unwelcome news because it tends to push up short-term interest rate expectations,” he said. “Indeed, rising rate expectations in the U.S. correlated with rising core inflation. Over the past few months, core PCE has risen from 2.8% YoY to 3.3%.”

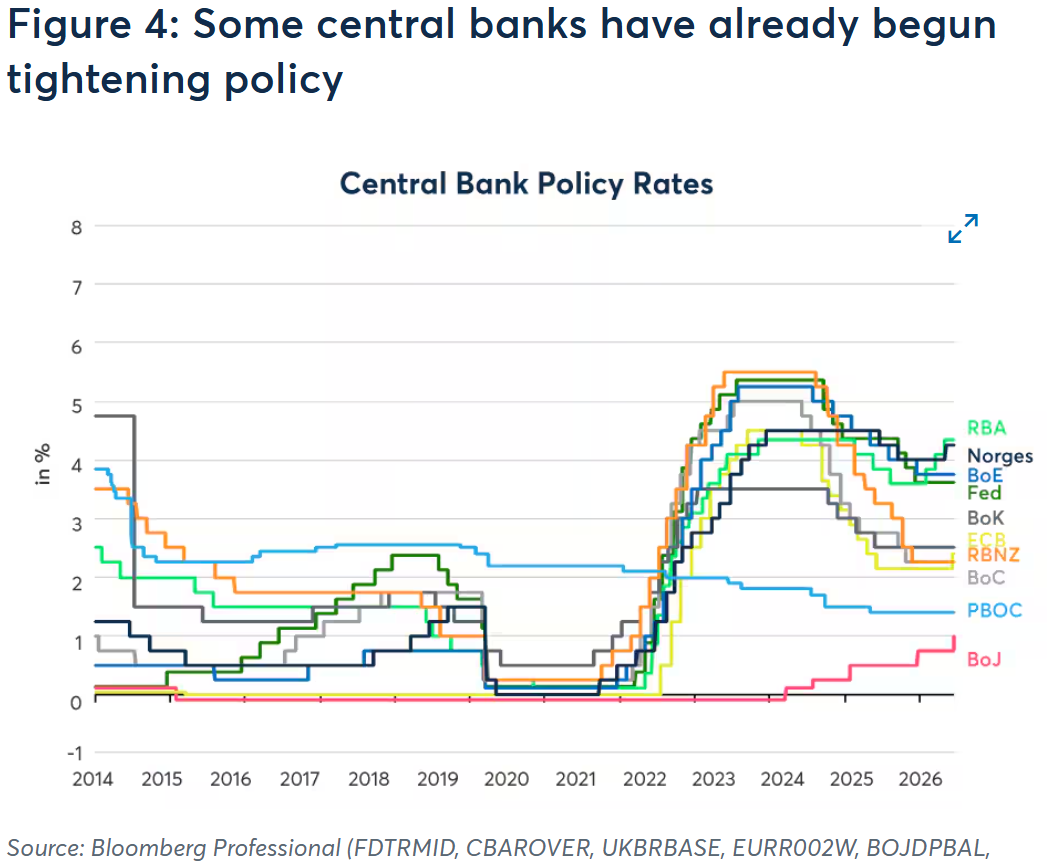

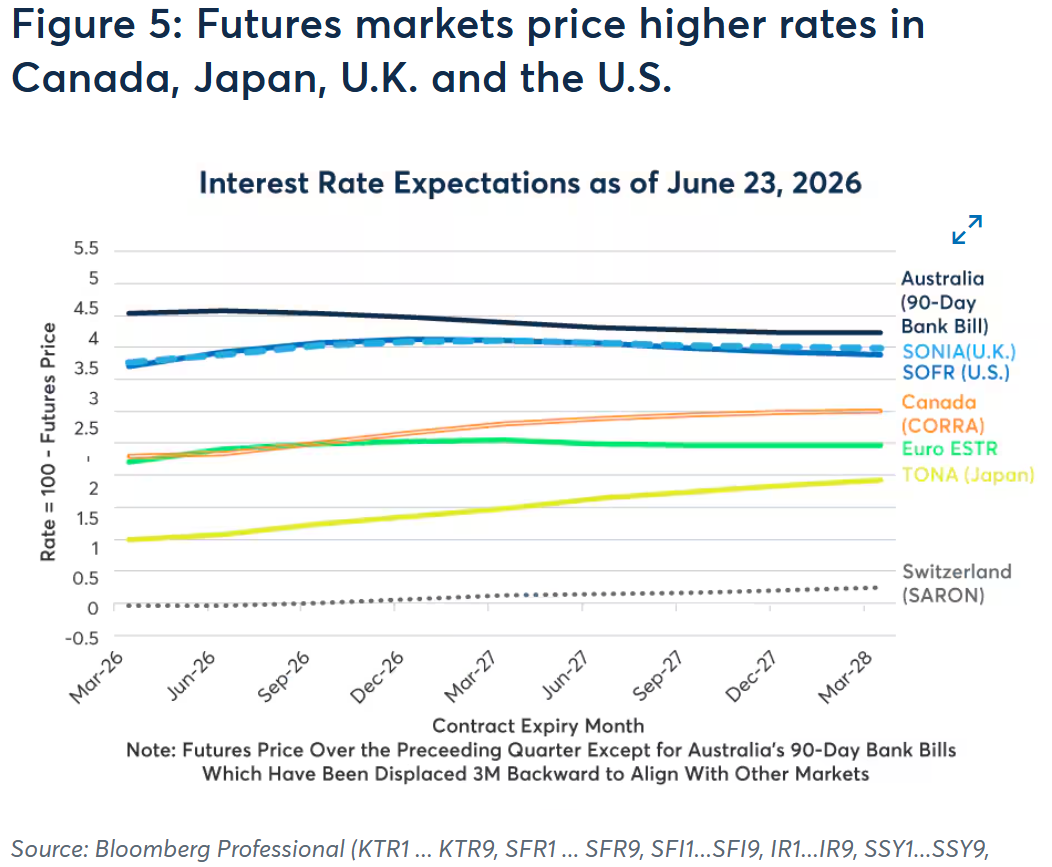

And while the Federal Reserve has abandoned its easing bias and Fed fund futures have priced in rate hikes, other central banks have already raised rates. “Thus far in 2026, the Bank of Japan, the European Central Bank, the Reserve Bank of Australia and Norges Bank of Norway have raised rates,” Norland noted. “And, the forward yield curves in many other nations are signaling the possibility of higher rates. The main driver appears to be that core inflation has been persistently running above target for years in the majority of these countries.”

But even as central banks are beginning to tighten monetary policy, he pointed out that fiscal policy remains extremely loose.

“Up until 2017, the U.S. budget deficit averaged about two percentage points less than the unemployment rate as a share of the economy,” Norland said. “That is, if the U.S. had a 5% unemployment rate, the budget deficit was probably around 3% of GDP. Since 2017, however, this structural dynamic has flipped: the deficit has transitioned from being roughly unemployment minus two percentage points to unemployment plus two percentage points.”

“Despite a relatively low unemployment rate of 4.3% currently, the U.S. is running a budget deficit of between 5% to 6% of GDP.”

And the United States is by no means alone in this degree of deficit spending. “Nations as diverse as Brazil, China, France, Germany, Japan, and the U.K. are also running large fiscal deficits,” he noted. “In Brazil and China, deficits are at 7.7% and 8.2% of GDP, respectively—surpassing the 5.8% for the U.S. as projected by the Congressional Budget Office in the current fiscal year ending September 30. France and the U.K. have deficits of 4.9% and 3.9% of GDP, respectively. Deficits are currently smaller in Germany and Japan (3.8% and 2.0% of GDP, respectively), but both nations plan to ramp up public spending later this decade on infrastructure and defense. Japan's public debt is close to 200% of GDP, roughly double that of its major peers. A similar deficit expansion holds true for the nations within the Gulf Cooperation Council in the Middle East.”

And while budget deficits do not drive the day-to-day performance of precious metals and bond markets, they are very impactful from year to year. “The persistence of these structurally large deficits risks producing two outcomes,” Norland said. “A massive volume of debt issuance that could drive sovereign bond yields significantly higher,” or “Structural concerns over the long-term sustainability of public finances could drive investors into precious metals.”

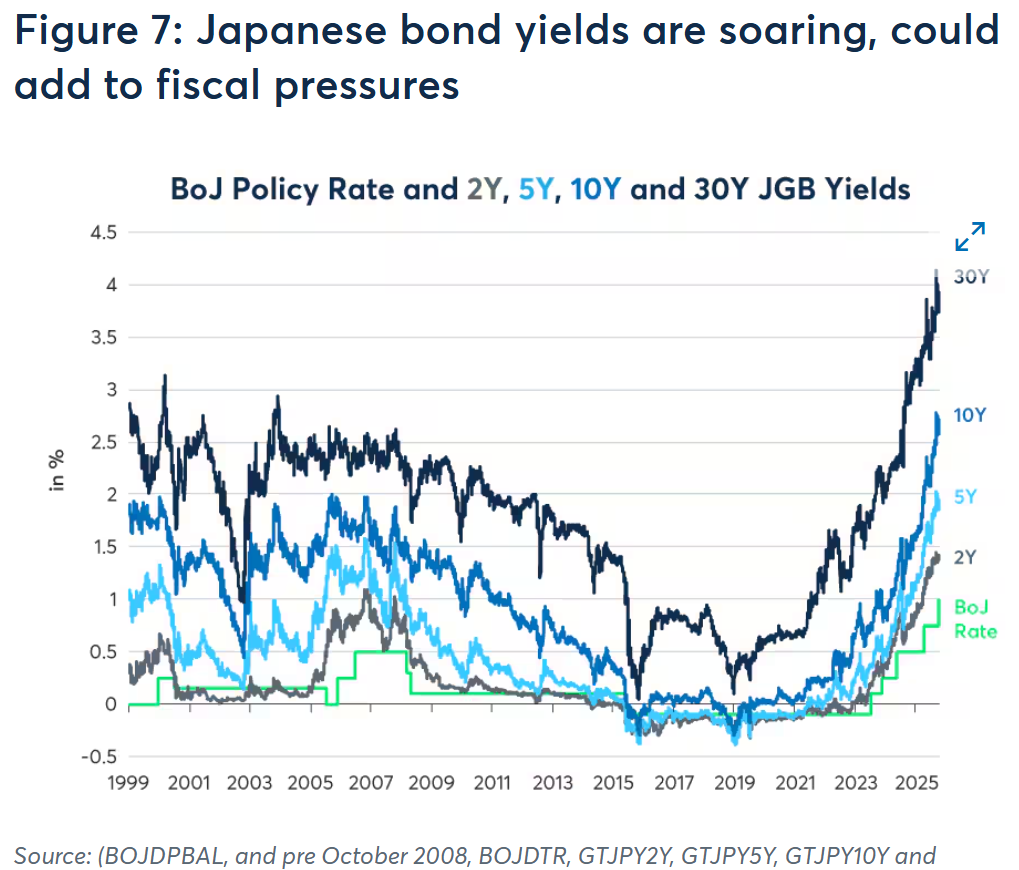

He noted that U.S. bond yields have not risen significantly in response to these concerns, but sovereign yields have spiked elsewhere. “Japanese government bond yields have been soaring,” he said. “Bond yields in France, Germany, the U.K., Australia and Canada have also been rising sharply, especially for longer maturities.”

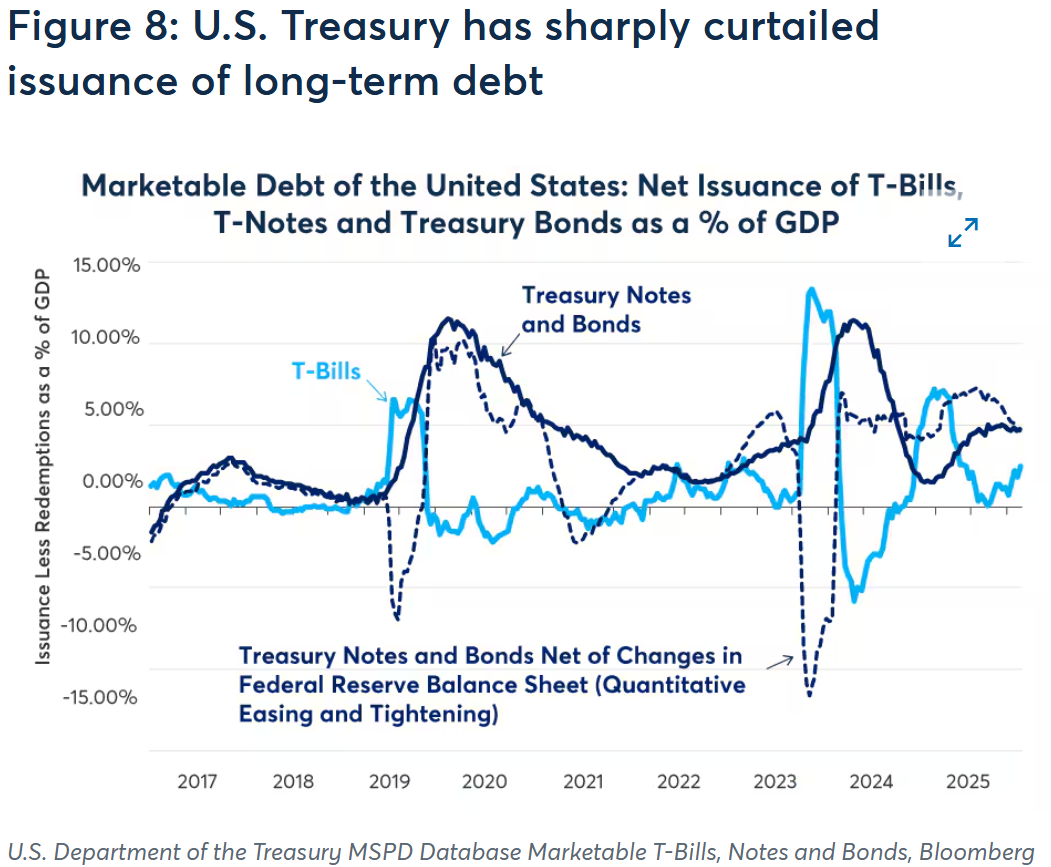

“U.S. Treasury yields have not been rising as much as their foreign peers so far in recent months as the U.S. Treasury has increased its issuance of T-Bills while the Federal Reserve has curtailed its quantitative tightening, reducing the amount of long-term debt coming into the market,” he pointed out.

“While favoring T-bills over long-term bonds suppresses long-term yields in the short term, an increased supply of T-bills heightens the concentration of highly liquid assets of the private sector,” Norland warned. “Because these instruments function quite similarly as cash, this supply shift could act as a backdoor means of monetary easing.”

Looking ahead, Norland questioned whether precious metals and bonds had hit their cyclical limits.

“Are precious metals at bargain prices after their recent decline, or will they continue to sell off? Will bond yields continue to rise or are they near a cyclical top?” he asked. “In the short-to-intermediate term, any increase in central bank rates is likely to push short-term rates higher and precious metals prices lower. As such, any continued rise in core inflation might be bad news for investors in bonds and precious metals.”

Over the longer term, Norland said budget deficits could be the deciding factor in the direction of precious metals prices and bond yields. “Any coordinated political effort to rein in deficits could lower long-term yields and reduce the structural lure of precious metals,” he said. “Conversely, the persistence or further expansion of these deficits could likely push long-term yields higher. At present, there appears to be very little political impetus anywhere in the world to implement tighter fiscal policy.”

Finally, Norland said the equity market remains a wild card.

“So long as equities continue to go higher, economic growth is likely to be sustained, increasing the likelihood of resource shortages that keep core inflation rates above central bank targets,” he wrote. “Consequently, a prolonged equity bull market may remain fundamentally bearish for both government bonds and precious metals.”

But if stocks suffer a severe correction, economic growth could slow sharply. “This could oblige central banks to reverse course and lower rates, potentially setting the stage for a renewed bull market in precious metals.”