(Kitco News)—The global financial system is facing its biggest challenge since the Great Financial Crisis (GFC), as inflation weighs heavily on global consumers and central banks continue to print money at a feverish pace.

While recent data in the U.S. has given some cause for hope that things are improving and inflation may soon be brought to heel, according to the Bank of International Settlements, moving forward, “monetary policy may well face an environment no less challenging than the one that has prevailed in the past decades,” with two factors that are “especially worrisome: fiscal trajectories and deep-seated adverse supply-side forces.”

That was the key takeaway provided in the “Challenges Ahead” section of the BIS Annual Economic Report 2024, released on Monday.

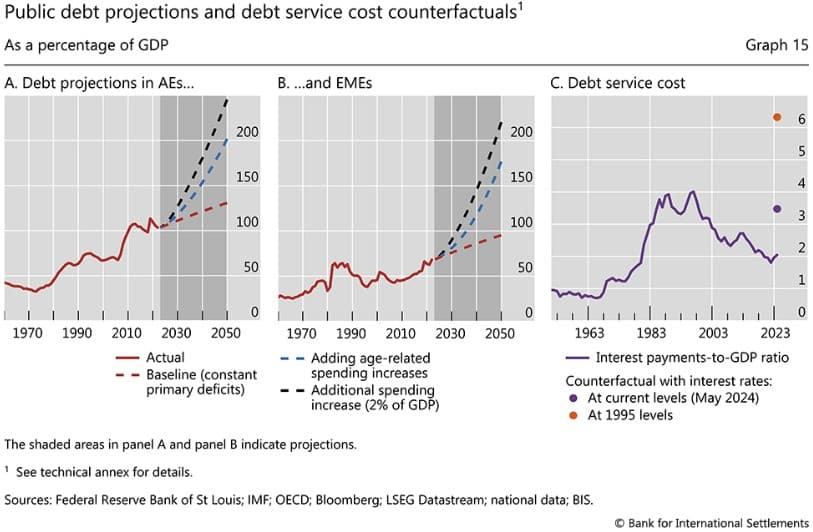

“As argued in detail in last year's Annual Economic Report (AER), longer-term government debt trajectories pose the biggest threat to macroeconomic and financial stability,” the BIS said. “Even if interest rates return to levels below growth rates, absent consolidation, ratios of debt to gross domestic product (GDP) will continue to climb in the long term from their current historical peaks.”

“The increase would be substantially larger if one factored in the spending pressures arising from population aging, the green transition, and higher defence spending linked to possible geopolitical tensions,” the report said. “The picture would be bleaker should interest rates settle above growth rates – something that has happened quite often in the past and would be more likely should the sovereign's creditworthiness come into doubt at some point. The trend decline in credit ratings in AEs and EMEs highlights this risk.”

The BIS noted that if interest rates remain at the current levels, “as governments refinance maturing bonds, the debt service burden will rise close to the record levels of the 1980s and 1990s. Should rates climb further, say, reaching the levels prevailing in the mid-1990s, debt service burdens would soar to new historical peaks, above 6% of GDP.”

The bank warned that higher public sector debt would “constrain the room for monetary policy maneuver by worsening trade-offs” and make it harder to achieve price stability.

“Higher debt raises the sensitivity of fiscal positions to policy rates. This increases the costs of a tightening and partly offsets its effects by boosting the interest income of the private sector,” they said. “In the extreme, if high debt cripples the credibility of fiscal policy or the creditworthiness of the sovereign, it can hamstring monetary policy: a tightening would simply heighten those concerns and fuel inflation, typically through an uncontrolled exchange rate depreciation.”

“Losses on public sector debt, whether caused by credit or interest rate risk, can generate financial stress; in turn, a weak sovereign cannot provide adequate backing for the financial system, regardless of the origin of the stress,” the BIS warned.

Signs of stress on the banking system have been evident since early 2023 when several banking failures prompted quick action by central banks, who scrambled to limit any possible contagion.

“The historical record has driven this message home repeatedly. Quite apart from inflationary pressures induced by expansionary fiscal policy, in evidence post-pandemic, there are many instances in which unsustainable fiscal policies have derailed inflation, especially in EMEs,” the report said. “Similarly, the past decade has shown the potential for the sovereign sector to cause financial instability, first as a result of credit risk (the euro area sovereign crisis) and more recently because of interest rate risk (eg the strains in the US banking sector in March 2023 or those in the UK NBFI sector in September 2022).”

The BIS also warned that “A slower-growing and less elastic supply could make the world more inflation-prone,” adding that the growing impact of artificial intelligence is also putting pressure on the system as it currently exists.

“In such a world, central banks would likely face similar challenges to those they tackled pre-pandemic, with persistent inflation shortfalls from target,” the report said. “If the events of the 21st century have highlighted one thing, it is the genuine uncertainty and unpredictability of the challenges central banks face.”

“They suggest that it would be desirable for monetary policy frameworks to pay particular attention to four aspects: robustness, realism in ambition, safety margins and nimbleness,” the BIS added. “They also point to the importance of complementary policies.”

“The unsustainability of fiscal trajectories poses the biggest threat to monetary and financial stability,” the BIS reiterated. “And supply may not be as elastic as in the decades preceding the pandemic due to changes in the degree of global integration, demographics and climate change. The world could become more inflation-prone.”

Due to the growing number of headwinds, the BIS warned, “In the years ahead monetary policy may well face an equally challenging environment” as was seen after the GFC.

“At the same time, a return to a world of more persistent disinflationary pressures cannot be ruled out, especially if the wave of technological advances underway bears fruit,” they warned.

“In the end, though, the trade-offs that monetary policy faces can become unmanageable absent more holistic and coherent policy frameworks in which other policies – prudential, fiscal or structural – play their part,” the report concluded. “Indeed, the growth illusion cannot be finally dispelled without a keener recognition that only structural policies can deliver higher sustainable growth.”

While the BIS is calling for more fiscal prudence, that is easier said than done, and according to macro guru Raoul Pal, founder and CEO of Real Vision, debt printing is not likely to end anytime soon. Pal sees a new wave of liquidity about to hit financial markets due to a variety of catalysts, which could be a boon for risk assets.

“We think that the Treasury runs down the Treasury General Account,” Pal said during a video update with Real Vision analyst Julien Bittel. “We think the Fed stops QT (quantitative tightening). We think that the end of the reverse repo gets drained. We think that Fannie Mae probably gets Congressional approval to offer equity release mortgages, which could add trillions of dollars. We think there’s either tax stimulus or fiscal spending stimulus to come.”

“We also think that globally, the Japanese might intervene in their currency selling dollars which adds dollars into the global system,” he added. “We also think that most countries will be adding liquidity as well. We think China needs to increase its liquidity.”

Other sources of increased liquidity highlighted by Pal include the implementation of Basel IV, a new banking regulation that requires banks to keep higher levels of liquidity on hand, and the weakness of commercial real estate.

“We also think Basel IV is coming next year, which means the banks are buying more bonds, so we think there are a lot of sources of liquidity,” he said. “Another one is commercial real estate. Eventually, if it remains ugly enough, the Fed could create a special-purpose vehicle to put all these loans in.”

“We’ve seen that historically in the past, particularly in the savings and loan crisis in the early 90s,” Pal noted. “That’s another method of liquidity. So there’s lots and lots of different avenues, and ones that we haven’t even covered.”

Due to these possible sources of liquidity, along with the upcoming Presidential election in the U.S., Pal has recently been calling for risk assets like Bitcoin to enter a “banana zone” during which they see their prices surge higher in dramatic rallies.

“Look, the backend quarter of an election year is true banana zone for all assets,” he said during an interview with Scott Melker. “It always is. So you know that you’ve got a very, very, very high probability that by autumn things are utterly ripping.”