(Kitco News) – Republican presidential candidate Donald Trump’s potential victory is only part of the strong bull case for gold heading into 2025, while lower silver prices are helping attract renewed interest from ETF investors even as Indian demand falters, according to precious metals analysts at Heraeus.

In their latest precious metals report, the analysts shared a four-part case for why they remain bullish on gold despite the metal’s already dramatic price gains.

First, “A Trump presidency is viewed as broadly positive for the outlook for gold,” they said. “Heightened political uncertainty could be a positive driver for gold as a general hedge against geopolitical risk.”

The analysts noted that the likelihood of a second Trump presidency has increased in recent weeks, and that the former president favors weakening the dollar and increasing tariffs on imports.

The second factor is the likely path of the USD itself under Trump’s proposed policies. “A weaker dollar is expected under a Republican US administration,” they wrote. “Reinflationary policy and tariffs are part of Trump’s goal to support US exports, but could also support the price of risk assets, such as gold. The strength of both the gold and dollar prices has been poorly correlated year-to-date, but fundamentally should be supportive of gold.”

Third, while net speculative positions are already bullish, they still have room to improve. “Net longs have grown to 25.8 moz in July,” Heraeus noted. “This is still below the high of 35.4 moz during the Covid pandemic, highlighting scope for further accumulation of longs in H2’24. Continued long building could help the gold price rise higher. However, the risk of a price reversal does increase as positioning becomes more stretched.”

Lastly, the analysts believe that overall gold investment remains undersaturated. “Despite a turn in global gold ETF holdings, volumes of allocated metal are still 30 moz lower than the peak in 2020,” they wrote. “The prospect of US interest rate cuts in September is likely to be driving inflows, and momentum switching from the East to West could be a strong swing factor for the gold price in H2’24.”

One factor that has become less supportive of gold prices over the last few months is Chinese demand. Heraeus sees China’s jewelry demand falling due to high prices.

“Elevated gold prices, particularly in yuan terms, persistently low levels of consumer confidence and uncertainty over the economic outlook are crimping gold jewellery demand in China,” they said. “Cautious consumers are less likely to spend on precious metals. Growth in retail sales of gold and silver jewellery fell to just 0.2% year-on-year in June, the lowest level since December 2022, when the country was still recovering from Covid-related lockdowns earlier in the year.”

“After having declined by 5% year-on-year in Q1’24 to 195 tonnes (source: World Gold Council), weak gold withdrawal data from the Shanghai Gold Exchange suggests that jewellery demand may have also declined in Q2,” they warned. “The outlook for Chinese gold jewellery demand for H2’24 is therefore cautious and may not match the 672 tonnes seen last year, particularly as the outlook for the gold price in the next quarter remains structurally bullish.”

After last week’s selloff, Heraeus said, “The short-term bearish price level to look out for is ~$2,300-2,330/oz, the area of strong support that provided the base for the previous rally.”

After multiple attempts to break above resistance near $2,395 per ounce shortly after the North American market opened, the spot gold price slid sharply to a fresh daily low of $2,369.65 per ounce. It last traded at $2,375.99, losing 0.47% on the session.

Turning to silver, the analysts see a risk that Indian demand for the gray metal could decline for the second straight year due to higher prices.

“Generally speaking, high silver prices tend to encourage inventory destocking and a reduction of imports in India,” Heraeus said. “Indian silver imports totalled 130 moz in Q1’24, but fell to just 17 moz in Q2 as the silver price rose above $25/oz. If silver manages to resist downward pressure from relatively weak economic data in a number of key consumption regions (EU, China) and maintains a price level of >$25/oz for the rest of the year, it is unlikely that Indian imports will meaningfully pick up again – aside from surges on dips as seen in the past. This could result in a contraction in Indian jewellery and silverware fabrication demand for a second year in a row.”

Conversely, higher prices are making silver more attractive to ETF investors than it has been in years, as they poured in to buy on the recent dips.

“The drop below $29/oz prompted more than 28 moz of ETF purchases in the last fortnight, taking silver ETF holdings to a three-month high of 714.8 moz as of 25 July,” they noted. “Although this is still significantly lower than the peak level of silver holdings in 2021, it has been the largest single-week inflow in holdings since then."

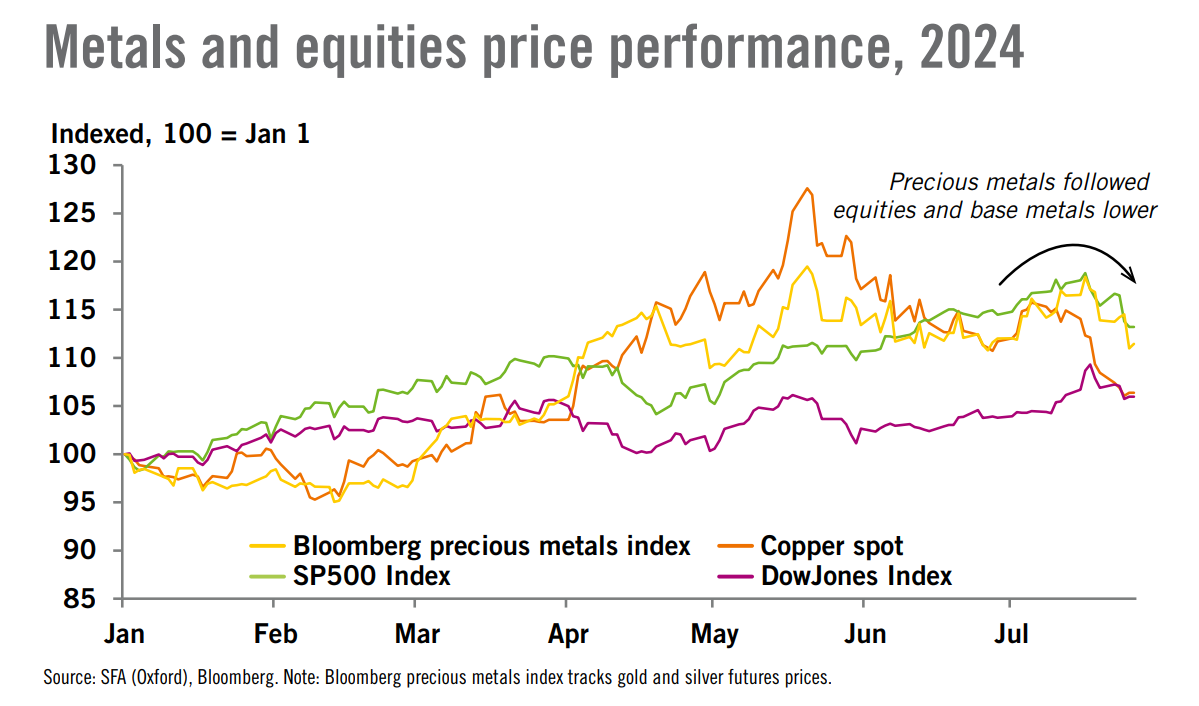

The analysts pointed out silver price saw heavy selling pressure last week as the spot price fell below $28 per ounce for the first time since May. “The decline in US stocks and base metals continued to spill over into the precious metals markets,” they said, adding that “additional pressure is being applied as the EU economic sentiment survey recorded its first drop in a year.”

Silver is seeing continued downward pressure on Monday, with spot silver last trading at $27.548 per ounce for a loss of 1.37% on the daily chart.