(Kitco News) – Bitcoin (BTC) bulls looked to bounce back from an overnight dip below $58,000 in early trading on Thursday as the latest data out of the U.S. showed that consumers remain resilient, with July’s retail sales climbing 1%, above estimates for a 0.4% rise, while another decline in jobless claims showed the labor market remains strong.

The upbeat data helped boost stocks and gold, and while Bitcoin is showing signs that it will continue to climb, it has been hampered by concerns that the U.S. government is about to start selling portions of its BTC stash again.

"The U.S. government transferred 10,000 Bitcoin (BTC) related to the Silk Road to Coinbase Prime early Thursday morning,” said Ryan Lee, Chief Analyst at Bitget Research. “This does not mean that 10,000 Bitcoin have already been sold.”

“Last month, the U.S. Marshals Service, an agency under the U.S. Department of Justice, announced a partnership with Coinbase Prime to ‘safeguard and trade’ large digital assets,” he noted. “Therefore, in addition to the purpose of ‘trading,’ it is also possible that the Bitcoin was merely handed over to Coinbase for custody. After all, Coinbase is the primary custodian for U.S. ETFs, and it is a possibility that the U.S. government entrusted the BTC to Coinbase for safekeeping.”

“Furthermore, such a large-scale Bitcoin transaction could significantly impact the market given the current liquidity situation,” he added. “Based on the current price performance, while there is a possibility of it being sold in the market, it is not very likely.”

While most analysts agree with Lee and have called for calm, the barrage of headlines warning that another major dump was imminent served to spook crypto traders, leading to the weakness seen on Wednesday.

“The cryptocurrency market retreated 2.9% over the past 24 hours to $2.08 trillion from levels near $2.15 trillion, which had been resistance for the past ten days,” said Alex Kuptsikevich, senior market analyst at FxPro. “Despite moderate optimism in equities following the inflation data, cryptocurrencies failed to find sufficient demand.”

“The negative performance of cryptocurrencies could herald another round of outflows from risk assets, especially ahead of the weekend,” he warned.

“Bitcoin fell to $58K, a loss of 4.5% in 24 hours,” Kuptsikevich noted. “The sell-off started with the crossing of the 50- and 200-day moving averages. According to statistics, when a ‘death cross’ is formed, it takes an average of one month to recover to the starting point.”

BTC/USD 1-day chart by TradingView

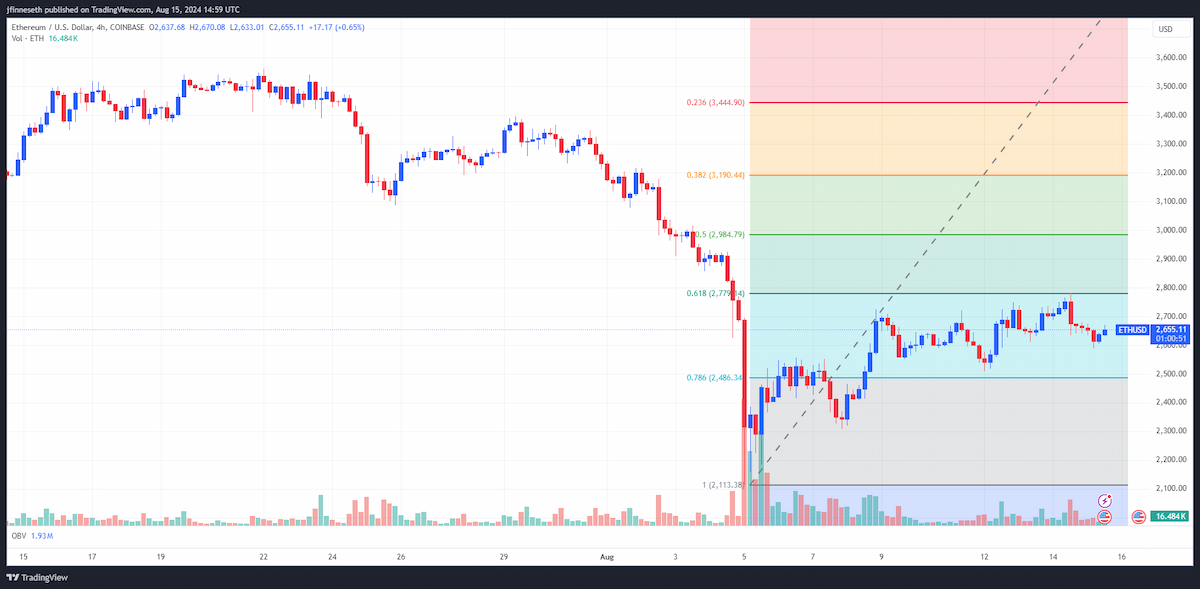

“Ethereum (ETH), which rolled back to $2620, experienced a similar drop,” he added. “The rally lost momentum near the 61.8% level of the initial decline, creating the risk of another $500 pullback.”

ETH/USD 1-day chart by TradingView

Data provided by TradingView shows that after hitting a high of $61,863 on Wednesday, Bitcoin’s price entered a sharp downtrend and fell to a low of $57,746 in the early hours of Thursday as concerns about government sales peaked.

BTC/USD 4-hour chart by TradingView

King Crypto has since seen a 3% bounce-back, and at the time of writing, trades at $59,720, an increase of 0.67% on the 24-hour chart.