(Kitco News) – Mentions of ‘recession’ have been increasing across social media and in financial headlines in recent weeks, but the signals have been mixed, leading to increased volatility across markets as investors struggle to make sense of the data and plan accordingly.

For economists at Goldman Sachs, recent improvements in retail sales and unemployment data suggest that the economy is gaining strength, prompting them to cut their probability of a recession in the U.S. within the next year from 25% to 20%.

“We have now shaved our probability from 25% to 20%, mainly because the data for July and early August released since August 2 shows no sign of recession," Goldman Sachs chief U.S. economist Jan Hatzius said in a note on Saturday, as reported by Reuters. “Continued expansion would make the U.S. look more similar to other G10 economies, where the Sahm rule has held less than 70% of the time.”

Hatzius added that if the August jobs report set for release on Sept. 6 “looks reasonably good, we would probably cut our recession probability back to 15%, where it stood for almost a year” before a revision on Aug. 2.

The economists also said they have become “more confident” that the Federal Reserve will cut interest rates by 25 basis points at their September policy meeting, “although another downside jobs surprise on September 6 could still trigger a 50bp move.”

While Goldman sees less chance of a recession, JPMorgan Chief Global Economist Bruce Kasman wrote that “the probability of a U.S. and global recession starting before end-2024” is now at 35%, which increases the likelihood of interest rate cuts, which will lead to a rise in M2. He also noted that the probability of a recession by the end of 2025 now stands at 45%.

“Important elements of our growth forecast are being challenged. U.S. news hints at a sharper-than-expected weakening in labor demand and early signs of labor shedding,” Kasman said. “The latest business surveys also suggest a loss of momentum in global manufacturing. On the other hand, these forces are being tempered by solid continued gains in overall activity, led by the service sector.”

“The modest increase in our assessment of recession risk contrasts with a more substantial reassessment we are making to the interest rate outlook. This is driven by the correlated shifts in growth and inflation risk that are shaking the gradualism narrative in current central bank rate guidance,” he explained. “Specifically, there has been a material positive shift in the risk profile on U.S. inflation as strong supply-side performance combines with moderating labor demand to ease labor market pressure.”

“Taken together, these developments warrant a break from gradualism and we expect the Fed to make a level adjustment in its policy stance that lowers rates by at least 100 basis points through year-end,” Kasman concluded.

While Kasman sees multiple rate cuts, Ed Yardeni, the Founder and President of Yardeni Research, told CNBC that he expects the Federal Reserve to implement a 25 basis points rate cut in September, but said that the cut would be “one and done.”

“The markets are very dovish; expectations are 25 to 50 basis points for the September meeting. I think there are expectations we’ll have 100 basis points between now and year's end. I think it's going to be 25 bps and I think it’s going to be one and done,” Yardeni said. “The economy is doing too well. I know people got freaked out by the last employment report, but I think a lot of that was weather, and some of the other indicators that came out confirmed that. Like single-family housing starts took a dive in the south.”

“So If I’m correct about that, they’re going to get indicators before the September FOMC meeting that suggest the economy is alive and well, the labor market is doing well, and that inflation is continuing to moderate,” he added. “So I think 25 basis points is enough, and I think that’s what Powell will probably communicate. It will be dovish, but not as dovish as the market is discounting.”

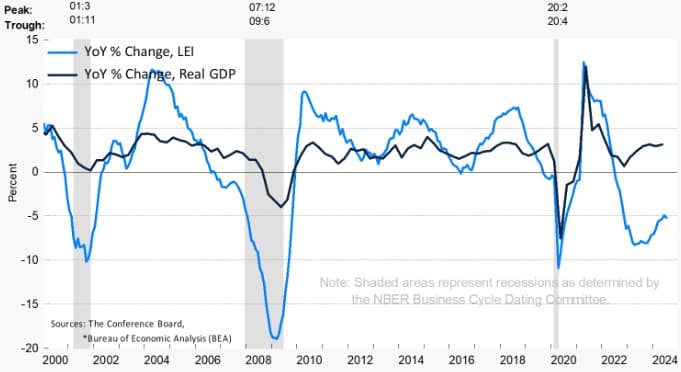

According to data provided by The Conference Board, the Leading Economic Index (LEI) for the U.S. “fell by 0.6 percent in July 2024 to 100.4 (2016=100), following a decline of 0.2 percent in June. Over the six-month period ending in July 2024, the LEI fell by 2.1 percent, a smaller rate of decline than its −3.1 percent over the six-month period between July 2023 and January 2024.”

“The LEI continues to fall on a month-over-month basis, but the six-month annual growth rate no longer signals recession ahead,” said Justyna Zabinska-La Monica, Senior Manager of Business Cycle Indicators at The Conference Board. “In July, weakness was widespread among non-financial components. A sharp deterioration in new orders, persistently weak consumer expectations of business conditions, and softer building permits and hours worked in manufacturing drove the decline, together with the still-negative yield spread.”

As noted by ZeroHedge, aside from the great financial crisis, “this is the worst decline in LEI since the mid-'70s.”

“These data continue to suggest headwinds in economic growth going forward,” Zabinska-La Monica said. “The Conference Board expects US real GDP growth to slow over the next few quarters as consumers and businesses continue cutting spending and investments. US real GDP is expected to expand at a pace of 0.6 percent annualized in Q3 2024 and 1 percent annualized in Q4.”

According to the report, “The LEI’s annual growth rate has stabilized but remains negative, suggesting downward pressures on economic activity ahead.”

However, despite the expected downward pressure, overall, the Conference Board said, “For the fourth consecutive month, the US LEI has not signaled a recession ahead.”

“And what is behind the 'no recession' call... US equity strength!!,” said ZeroHedge. “So, to summarize – almost all the macro data signals weakening growth for years... but because stocks are up (and credit spreads down), there's no recession anywhere on the horizon!!??”

Amid the mixed messaging on the possibility of a recession, a poll conducted by Reuters found that economists expect the Fed to cut interest rates by 25 basis points at each of the remaining three meetings of 2024 to avoid such a result, leading the economists to say that a recession is unlikely.

Most economists who participated in the poll said they do not expect a rapid series of rate cuts as recent data, including last week's strong retail sales report, suggests the economy is performing relatively well even as inflation recedes.

“The U.S. central bank will cut the federal funds rate by 25 basis points in September, November and December taking the range to 4.50%-4.75% by end-2024, according to 54% of those polled, 55 of 101,” Reuters journalist Indradip Ghosh wrote. “Markets, which were earlier betting on a half-percentage-point cut in September, are currently pricing around 70% probability of a quarter percentage point cut next month.”

“The basis for the cuts that we have is mostly because inflation is coming down,” Jonathan Millar, senior U.S. economist at Barclays, told Reuters. “It's not so much that activity is slowing ... We see a pretty resilient economy that's growing near trend and with that, we think inflation only ebbs gradually.”

“The labor market is hanging in there just fine. It's gradually cooling, but we don't expect it to have really material weakening,” he added. “The unemployment rate is maybe going to add another 10th or so from where it is. There's not really any reason for them (the Fed) to panic.”

The economists polled forecast that the unemployment rate will hover around the current 4.3% rate through 2026, and they said inflation will ease “only lightly over the coming two years.”

“All measures of inflation polled - the Consumer Price Index, core CPI, personal consumption expenditures price index and core PCE - are expected to stay above 2% until at least 2026,” Ghosh wrote. “Despite recent easing, wage growth has remained above the 3.0%-3.5% range seen as consistent with the Fed's 2% inflation target.”

With the U.S. economy growing at an annualized rate of 2.8% in the second quarter, faster than the 2.0% expected by economists, the poll found that economists see a recession as unlikely.

“Growth is seen in the poll as averaging 2.5% this year, faster than what Fed officials currently see as the non-inflationary growth rate of 1.8%,” the report said. “Two-thirds of common contributors upgraded their 2024 growth outlook from last month. The economy was predicted to grow 1.8% next year.”

“Economists in the poll broadly expect the economy to expand at around its trend growth rate at least until 2027,” Gosh said. “The median forecast from a smaller sample who provided a view showed the probability of a recession at just 30% - an outlook which has not changed much since the start of this year.”

"We're not convinced there's a downdraft in activity around the corner that's going to prompt large rate cuts from the Fed," Michael Gapen, chief U.S. economist at Bank of America, told Reuters. “There's reason to believe the July employment report was adversely affected by weather and therefore was a false signal about the health of labor markets and the economy. We're counting on subsequent data validating that story."

According to Carsten Fritsch, a precious metals analyst at Commerzbank, while base metals and industrial precious metals may struggle in the coming months, Commerzbank expects to see a recovery in 2025 as economic conditions improve, and the bank doesn’t see the U.S. economy slipping into a recession this year.

“There are signs of significant interest rate cuts by the most important central banks,” Fritsch said. “This should favor an economic recovery next year. Furthermore, we do not expect the US economy to slide into recession this year. Concerns about this had put commodity prices under significant pressure at the beginning of August. We, therefore, assume that commodity prices will rise again in the coming quarters from their current low level. However, the difficult economic situation in China suggests that the losses will not be recovered quickly.”

For now, market watchers are focused on this week’s annual economic symposium in Jackson Hole, Wyoming, and any hints from Fed Chair Jerome Powell regarding the outlook for the economy and the future of interest rates.